BONDS: NZGBS: Richer With US Tsys As Risk-Off Buoys

NZGBs are 2-3bps richer after US tsys finished 4-5bps lower in yield.

- Latest headlines quoted Omani mediators that there were significant progress in US-Iran talks. Progress and continued talks signaling that a breakthrough deal to limit Iran’s nuclear programme and avert a US strike are possible.

- This saw risk sentiment improve slightly, with US tsys & US$ paring gains, stocks paring losses.

- Initial claims for the week of Feb 21 came in at 212k - still within recent ranges but below consensus expectations of a 216k reading.

- The ANZ consumer confidence index fell 6.6%m/m in Feb to 100.1, this unwinds the Jan bounce (the Dec reading for the index was 101.5). Sentiment is still above lows from 2025 around 92.0, but the uptrend has stalled.

- At the most recent RBNZ decision, the central bank emphasised the need for consumer spending to support the economic recovery and that spending was more likely to be reliant on labour income rather than housing wealth (generated by rising prices), which was a departure from previous cycles.

- Swap rates are 1-4bps lower, with a flatter curve.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for April, while December 2026 assigns 29bps.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NEW ZEALAND: Jobs Filled Flat In Dec, After Strong Nov Rise, Y/Y Close To Flat

New Zealand filled jobs for Dec were flat after a revised 0.5%m/m gain for Nov (originally reported as a 0.3% rise). The Nov rise was the strongest outcome since April 2023. This leaves the y/y pace at -0.1%. The data show the improvement in the labour market slowed somewhat in Dec, but this came after a strong Nov outcome. We would expect further general improvements in these trends, given expectations NZ growth improved late 2025 and into early 2026. The outcome is unlikely to shift near term RBNZ thinking.

- Stats NZ notes, in y/y terms, that jobs filled were down 3.1% in construction, and -1.6% in manufacturing. Services related jobs filled was positive in y/y terms.

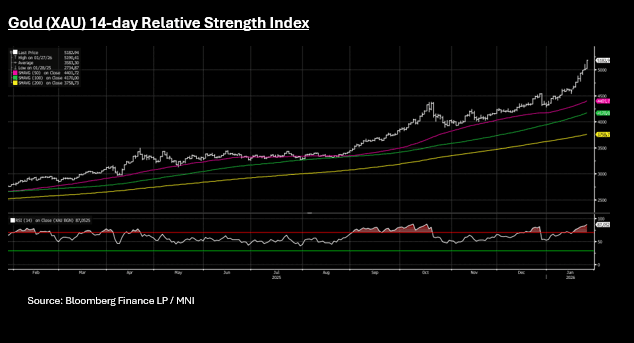

GOLD: Valuations Sidelined as the Bias to Rally Continues

- Gold's relentless rally continued overnight pushing higher, with momentum indicators suggesting extreme valuations.

- Since the beginning of the trading year, gold has rallied 14 out of the 18 trading days pushing bullion deeply into overbought on the 14-day relative strength index.

- Gold rose +3.4% by the close in the US overnight pushing to new all time highs of US$5,186.08 and the biggest one day gain in eight months.

- Early last year, the drivers for gold's ascent seemed clear - the US were ratcheting up their trade rhetoric through the threat of tariffs and gold's safe haven status underpinned demand.

- Successive Central Banks globally have upped their allocation to gold in what some market observers suggest is a 'debasement trade' where investors begin to shy away from treasuries or JGBs and even USD assets in general. Going further, some assess this as equal parts concerns as to the fiscal position in the US and Japan or a re-allocation away from USD assets in a global rebalance.

- Either way, gold's ascent has been astonishing. Gains of 66% in 2025 are being backed up with a year to date tally of almost 20%.

- Finding reasons for gold to fall in the current environment is difficult. Markets can ignore valuations for a long time, until they don't.

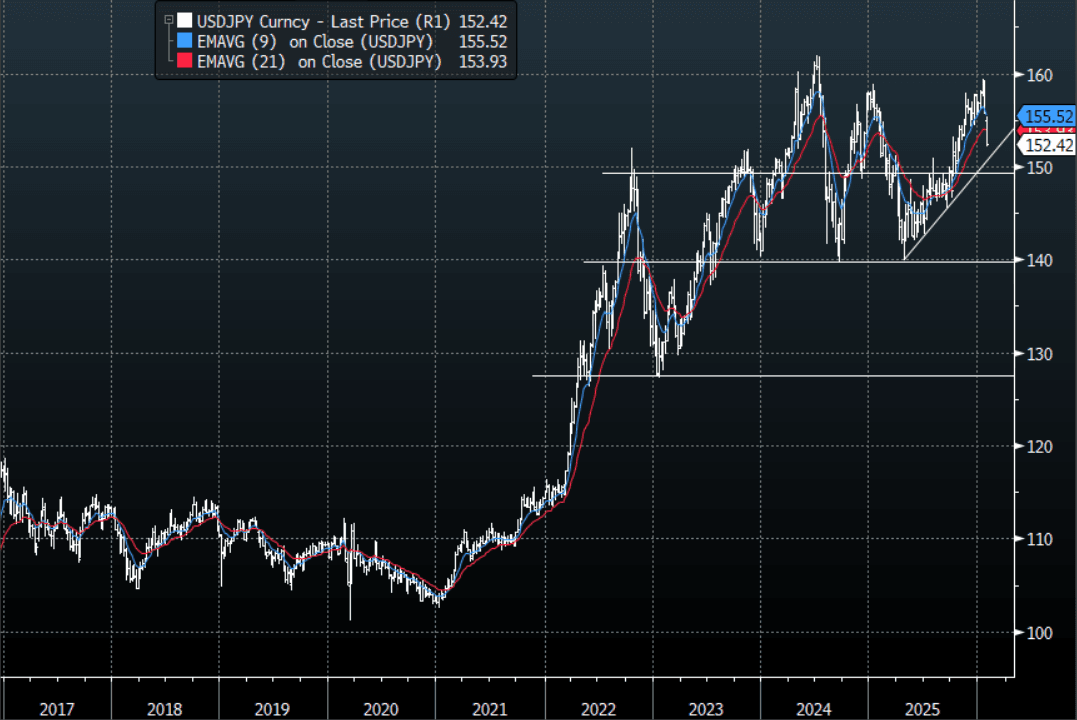

JPY: USD/JPY-Leveraged Funds & CTA Yen Shorts Being Purged, 149-152 Support

The USD/JPY overnight range was 152.10 - 154.88, Asia is currently trading around {USDJPY Curncy}. USD/JPY continues to slide as a leveraged market is forced to pare back large Yen shorts. If the market's take is correct this could be a big deal but as of yet it looks to have been little more than words to me, I feel there will need to be real and active intervention and the participation of the FED would need to be key to give it any real probability of success. For the moment the collapse lower has released a pressure valve causing leveraged funds and CTA’s to have to pare back large JPY shorts, but I suspect unless we get something more significant and clarity around FED involvement dips could remain supported once those shorts have been purged. In today's Asian session, we could continue to see shorter term players and CTA’s continue to reduce, first sell-zone is 153.75-154.25 and then 155.50-1.5600. The price has moved quickly lower and is now approaching its longer-term support, the area between 149.00-152.00 is wide but nothing has really changed and this area should start to offer good risk/reward again for Yen bears again.

- MNI INTERVIEW: Ex-BOJ's Sakurai Sees April Hike, 1.5% Rate. Sakurai expects three rate hikes over the next two fiscal years – either one in 2026 and two in 2027, or two in 2026 and one in 2027 – as the BOJ faces the challenge of breaking the vicious cycle of high inflation, fiscal expansion, and a weak yen. {NSN T9IEQV6QRTHD <GO>}

- “BofA Sees Yen in 150-158 Range Until BOJ Meeting in April. In the longer term, BofA anticipates that structural outflows may continue to weigh on the yen, which would leave the currency vulnerable if the acceleration of US growth and inflation prompts the Fed to begin the next rate-hike cycle.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 154.00($727m). Upcoming Close Strikes : 153.75($1.26b Jan 29), 156.00($1.33b Jan 30) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 177 Points

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P