BONDS: NZGBS: Little Changed, US Tsys Rally Slightly After Flurry Of Data

Dec-03 22:12

NZGBs are little changed after a modest rally by US tsys on Wednesday following a flurry of economic data.

- The ISM services index was stronger than expected in November as it inched higher to 52.6 (cons 52.0) after 52.4 in October, marking its highest since February.

- The S&P Global US services PMI continues to offer a more optimistic assessment of current activity despite being revised down in its final November release to 54.1.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November, whilst the October increase was revised up from 42k to 47k.

- Construction work rose 1.5% q/q (estimate +0.2%) in Q3 versus a revised -2.4% in Q2.

- NZ Treasury published financial statements for the four months ended Oct. 31, with the OBEGALx deficit at NZ$4.94bn, NZ$705mn wider than the gap projected in the May budget.

- NZ house prices stagnated in November, leaving them barely changed from a two-year low recorded in September.

- RBNZ-dated OIS pricing is little changed across meetings. 2bps of easing is priced for February, while November 2026 assigns 28bps of tightening.

- The NZ Treasury plans to sell NZ$150mn of the 4.50% May-30 bond, NZ$225mn of the 4.50% May-35 bond and NZ$75mn of the 2.75% May-51 bond.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Little Changed, Holding Yield Bounce, Q3 Jobs & Wages Tomorrow

Nov-03 22:01

NZGBs are unchanged despite a heavy close for US tsys, with yields ~3bps higher.

- US tsys extended early weakness after unexpectedly large corporate bond issuance announced ($40.5B with Alphabet making up $17.5B over 8 tranches) - only to gap back to pre-open level after lower-than-expected ISM Mfg & Prices paid data.

- The key event in NZ this week is the release of Q3 labour market and wages data tomorrow. Filled jobs for the quarter signal a stabilisation, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ's August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

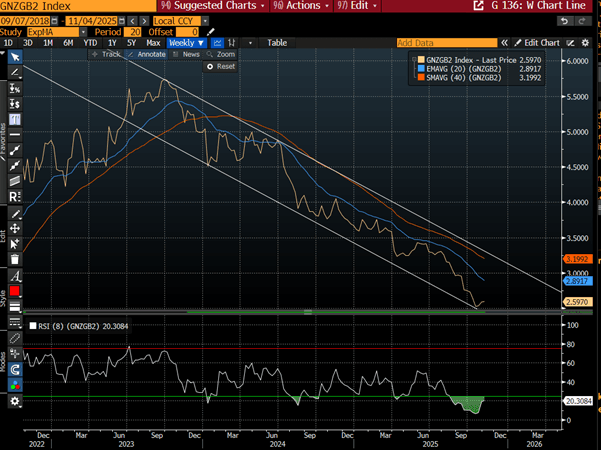

- Swap rates are little changed. The 2-year rate is holding its recent rise, bouncing off channel support, after reaching extreme overbought conditions. (see chart)

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for November, with a cumulative 30bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

OIL: Crude Relieved OPEC Will Pause But ISM Raised Growth Fears

Nov-03 21:55

There was a relief rally in the APAC and early European sessions on Monday following OPEC’s December output increase in line with November but specifically because it said it would keep quotas unchanged in Q1, a time of soft demand. Oil then trended lower reaching a trough following the disappointing US manufacturing ISM, which may suggest slower growth and thus also energy demand.

- WTI is flat at $61.00/bbl off the low of $60.51 reached when the ISM printed at 48.7 down from 49.1, a small rise had been expected. It made a high of $61.50 earlier, below resistance at $62.59. The bear trigger is at $55.96.

- Brent rose 0.1% to $64.86/bbl off the intraday trough of $64.33. It reached a peak of $65.32, just below initial resistance at $65.98, 9 October high. Initial support is at $63.37, 24 October low.

- The market has been range trading as uncertainty remains elevated. There are currently significant seaborne flows in line with increased production. However, Ukraine’s attacks on Russian facilities may impact supply. It struck a tanker in the Black Sea and damaged port infrastructure at Tuapse.

- The outlook for 2026 is unclear with OPEC pausing the unwinding of output cuts in Q1 and most members facing capacity constraints. Lower prices are discouraging US shale producers. The IEA expects a record oil surplus next year which could also drive production cuts.

- On the demand side, there is a structural decline but the impact of increased protectionism on the global economy remains unclear. However, sanctions on Russian majors Lukoil and Rosneft appear to be reducing demand for Russian crude as buyers look to other suppliers.

ASIA: Government Bond Issuance Today

Nov-03 21:28

- South Korea to Sell KRW4.1tn 30-Year Bonds

- Hong Kong to Sell HK$63.73 Billion 91-Day Bills

- Hong Kong to Sell HK$17 Billion 182-Day Bills

- Bank of Thailand to Sell 50 Billion Thb of 364-Days Bills

- Bank of Thailand to Sell 65 Billion Thb of 91-Days Bills

- Bank Indonesia to Sell 181D SVBI Bills

- Bank Indonesia to Sell 92D SVBI Bills

- Bank Indonesia to Sell 32D SVBI Bills

- Bank Indonesia to Sell 365D SVBI Bills

- Bank Indonesia to Sell 273D SVBI Bills

- Philippines to Sell Agg PHP35.0 Bln 5-Year Bonds

- Philippines to Sell Agg PHP35.0 Bln 10-Year Bonds