NZD: NZD/USD - Remains Within Its 0.5915-0.6015 Range, Albeit With A Heavy Tone

The NZD/USD had a range today of 0.5947-0.5995 in the Asia-Pac session, it is currently trading around 0.5985, -0.22%. The NZD like the AUD had an impressive bounce from its lows filling in its early morning gap from the Asian open. The pivotal resistance toward 0.6100-0.6150 continues to cap for now and the dovish read of the RBNZ has delayed its challenge in the short-term and this global turmoil will just add to its headwinds. On the day, price still remains in its 0.5885-0.6015 range, I suspect rallies back toward 0.6000 could now be sold into as the market looks to see if the USD gets bought as a safe haven into the London open.

- MNI AU - NZ Jan Jobs Filled Up, But Stop/Start Nature Of Job Rises Continues: The stop/start nature of the NZ jobs recovery continued in Jan. Filled jobs rose 0.2%m/m, after a revised 0.3% fall in Dec (which was originally reported as a flat outcome). In y/y terms filled jobs were down 0.2%. The m/m profile was -0.2% in Oct last year, +0.5% in Nov, -0.3% in Dec and now +0.2% in Jan. Hence there isn't clear signs of a consistent pick up in labour demand. This will feed into RBNZ thinking around holding rates lower as it waits for firmer evidence of economic recovery feeding into the labour market (before it tightens rates). The central bank did state at its last meeting that a rate hike was possible by year end but this wasn't set in stone in terms of its OCR outlook.

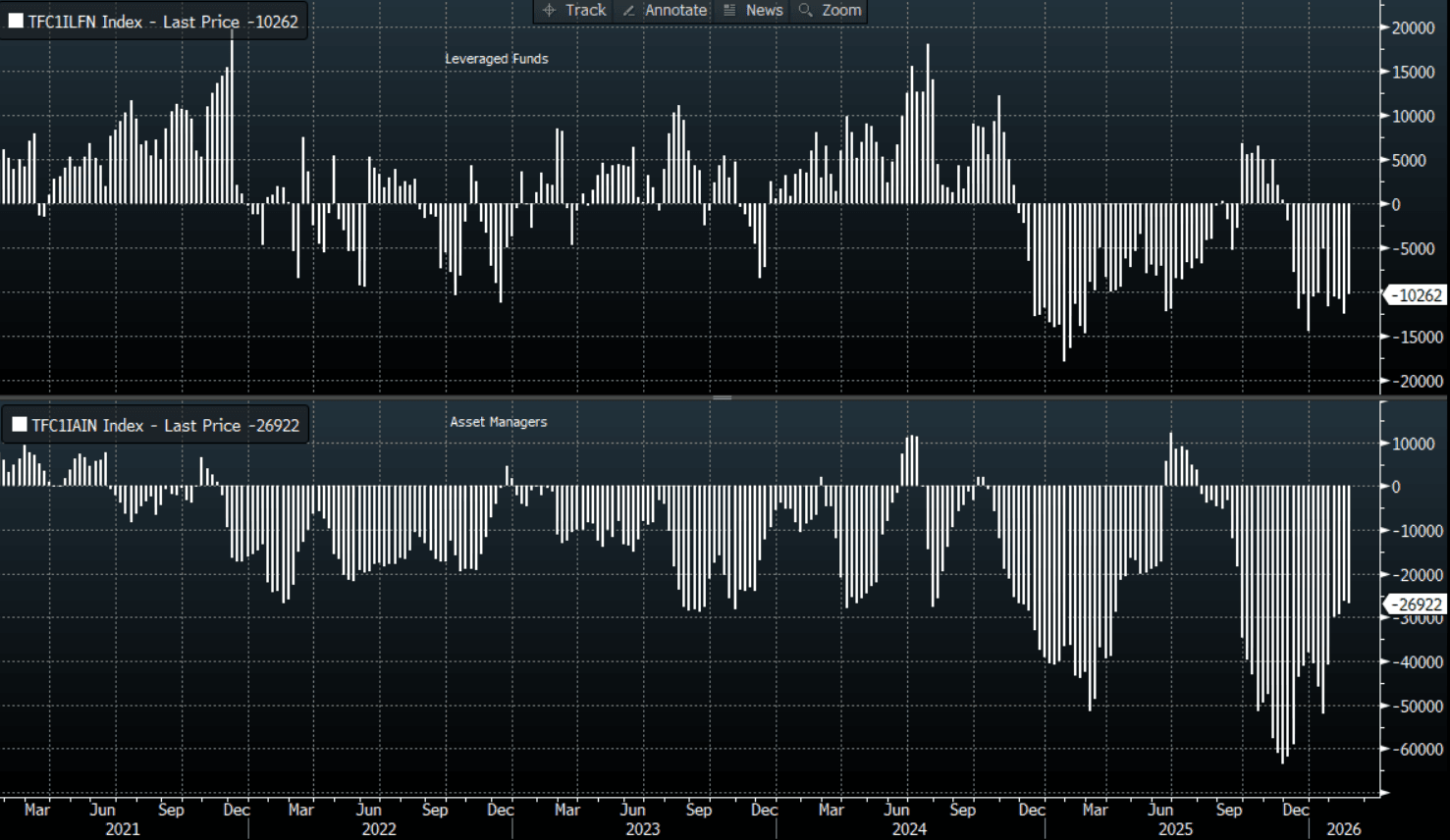

- CFTC Data up to 24/02/2026 shows Asset Managers maintaining their slightly reduced short positions in the NZD, -26922(Last -26152). The Leveraged community slightly pulled back their own shorts, -10262(Last -12465).

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5950(NZD894m March 5) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 47 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Gov Bowman: We Should Be Ready To Adjust Rates Toward Neutral

Fed Vice Chair for Supervision Miki Bowman said Friday that while she didn't elect to cut rates in January, she could be ready to cut in March. She made clear that she saw 3 cuts this year in the December Dot Plot (as MNI had assumed), making her one of the biggest doves on the Committee. (speech text here)

- "I continue to see policy as moderately restrictive, and, looking ahead to 2026, my Summary of Economic Projections includes three cuts for this year."

- The key is that "downside risks to the labor market have not diminished, and we should not overemphasize the latest reading on the unemployment rate...My view is that we should continue to focus on downside risks to our employment mandate, and the description of the labor market is helpful to communicate that we are not overly confident. History tells us that the labor market can appear to be stable right up until it isn't."

- "Absent a clear and sustained improvement in labor market conditions, we should be ready to adjust policy to bring it closer to neutral...we should also not imply that we expect to maintain the current stance of policy for an extended period of time because it would signal that we are not attentive to the risk that labor market conditions could deteriorate."

- "In my mind, the question at this meeting was about the timeline for implementing these cuts, essentially choosing between continuing to remove policy restraint and arriving at my estimate of neutral by the April meeting, or moving policy to neutral at a more measured pace throughout this year."

- "I am also reluctant to take meaningful signal from the latest data releases given the statistical noise introduced by the government shutdown" but "Given that by the time of our March meeting we will have received two additional inflation and employment reports, I saw merit in waiting to take action."

MACRO ANALYSIS: MNI US Macro Weekly: The Fog Of Warsh

We've just published our US Macro Weekly - Download Full Report Here

- The largest rate moves of the week surrounded President Trump’s selection of former Fed Governor Kevin Warsh as the next Fed chair when Powell’s term in the position ends in May.

- A next Fed cut is close to being fully priced for the June meeting again (22bp, the first meeting under the new Fed chair) whilst there are two 25bp cuts fully priced by year-end.

- While historically more hawkish than most of the other contenders but also favoring economic productivity arguments for expecting inflation to remain in check amid solid growth, there remains high uncertainty on what the Fed might look like under Warsh’s leadership. (More from our Policy Team on page 18.)

- That includes policy on the balance sheet (preferring a smaller one) and communications, the Fed’s reach outside of core monetary policy channels, and even personnel, having previously said "I think what we need is regime change at the Fed, and that's not just about the Chairman, it's about a range of people...it's about breaking some heads, because the way they've been doing business is not working."

- Warsh or not, one impetus for consensus on a resumption of Fed easing would be a clear deterioration in the labor market, but here the data evidence remained mixed. Jobless claims remain at a healthy level despite initial claims surprising higher for the first time since Dec 11 after a particularly impressive run but with residual seasonality concerns. Continuing claims pushed lower still however but also with some questions over the role of unemployment insurance eligibility roll-off.

- A further acceleration of strong core PPI inflation trends had little impact on Friday against a backdrop of precious metal prices tumbling, whilst details confirmed strong core PCE estimates at ~0.4% M/M for Dec.

- Real GDP growth tracking for Q4 has been trimmed from 5.4% to a still very strong 4.2% after latest volatility in monthly trade reports. Capital goods imports are up strongly in tech-led strength but consumer and industrial imports are down heavily in a hangover from tariff front-running in Q1.

- Manufacturing firms’ sentiment firmed in January but consumer confidence slumped, with the lowest Conference Board metric since 2014 as consumer labor market perceptions softened further.

- The FOMC treaded a largely neutral path with its January decision, maintaining its easing bias but sounding slightly more patient in making its next move than it did last month. Markets took a very mildly hawkish interpretation with implied rates rising under 1bp for meetings to July but even less of a move further out, and the dollar remaining largely unmoved.

- Looking ahead, another government shutdown looms, starting Saturday, but with questions over its potential duration and breadth. In the event the BLS isn’t impacted, the nonfarm payrolls report for January will highlight the week’s economic data on Friday. The report will include benchmark revisions and will continue to see attention on the unemployment rate after its recent stalling around the 4.4% mark.

- We also get Treasury’s quarterly financing and borrowing updates, with attention on any revisions to its guidance on future increases in auction sizes.

US DATA: BLS Economist Matsumoto To Be Nominated As Commissioner: WSJ

The Wall Street Journal reports that President Trump will nominate Brett Matsumoto as the next Commissioner of the Bureau of Labor Statistics. The role has not been filled since Trump fired Commissioner McEntarfer in September shortly after weaker-than-expected nonfarm payrolls report, accusing her of manipulating the data for political reasons.

- Importantly what little we know about Matsumoto suggests that he shouldn't have too much difficulty receiving Senate confirmation, as he has relevant experience and educational background, with little in the way of political entanglements. From the WSJ report: "Matsumoto has worked as an economist at the BLS since 2015. Before spending much of the past year on assignment with the White House Council of Economic Advisers, he had no experience working in a political capacity. He earned a Ph.D. in economics from the University of North Carolina at Chapel Hill in 2015. Matsumoto didn't respond to requests for comment."

- Trump's previous nominee, E.J. Antoni, had his nomination withdrawn in October due to key Senators on the relevant Committee having reservations over his appointment. NPR reported at the time "Antoni's selection was praised by Trump loyalists like Stephen Moore and Steve Bannon. But it was roundly criticized by even conservative economists. Opponents said Antoni — who has spent most of his career at right-wing think tanks — lacked the expertise in statistical number crunching that's typical of previous BLS commissioners. A group of BLS supporters issued a statement Tuesday urging the president to choose a new nominee with a technical and non-partisan background."