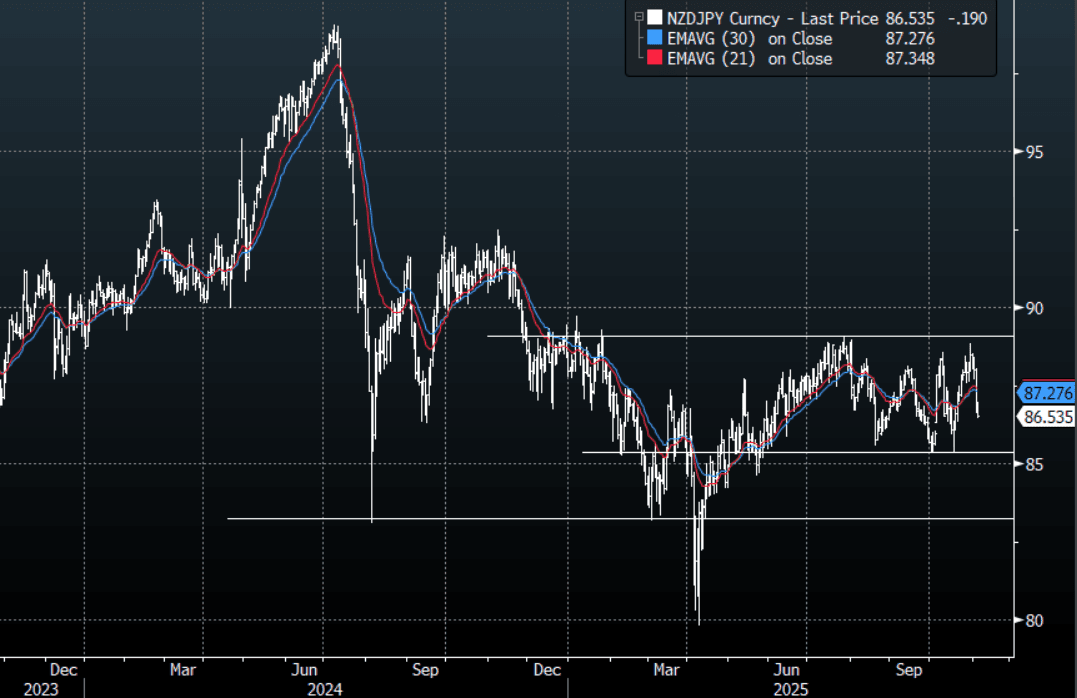

NZDJPY: NZD/JPY - Turns Lower With Risk, Targets 85.00 Initially

The overnight range was 86.60 - 87.36, Asia is currently dealing 86.45. This pair stood out as the outlier when cross-yen was accelerating higher and was the best vehicle to be short of if you wanted a hedge against those in your basket. This turnaround in risk has seen the pair very quickly gather pace lower again. A lot obviously depends on how long and how deep this correction in risk turns out to be, but NZD/JPY should now be a sell on rallies as the focus turns back toward the 85.00 area. A break back below 85.00 could potentially signal the start of a bigger move lower and the beginning of a new downtrend.

Fig 1 : NZD/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: 2/10s Steeper, 10yr Tracking Recent Ranges As Govt Shutdown Continues

US Tsys futures are maintaining a negative bias since the open, although fresh weakness after the gap lower at the open has been modest. Spillover to the cash Tsy space is evident from the steepening bias seen in cash JGBs. The US 2/10s was last +56bps, back around Oct highs (Sep highs were +62bps). More broadly for the outright 10yr, last at 4.14%, +2bps, we remain wedged within recent 4.10-4.20% ranges. Market sentiment is somewhat mixed, with limited official data out due to the government shutdown (thereby limiting assessment on economic trends) potentially impacting sentiment. 10yr futures (TY) were last 112-17, -04+, leaving the 50-day EMA support point at 112-12+ intact.

NEW ZEALAND: RBNZ Forecast To Cut But By How Much?

The focus of the week is firmly on Wednesday’s RBNZ decision. While it is widely expected to cut rates further, economists are split between a 25bp and 50bp move. 10 out of the 25 analysts surveyed by Bloomberg are forecasting the larger reduction. The announcement won’t be accompanied by updated forecasts or a press conference (they are scheduled for November), but post-meeting speaking events should be announced this week.

- In terms of data, the key Q3 Quarterly Survey of Business Opinion (QSBO) is released on Tuesday. It should give an indication of how weak the recovery is and as a result possibly impact the size of rate cut projections ahead of Wednesday’s RBNZ decision.

- In terms of surveys, there is also BusinessNZ’s PMI for September. It showed manufacturing stagnating in August with the PMI at 49.9 but the Q3 average was 51.3 up from Q2’s 50.0. While August output and employment were below the breakeven 50-level, forward-looking new orders rose to 55.2, the highest since March 2022.

FOREX: USD/JPY Marching Towards 150.00 Test, EUR/JPY To Record Highs

USD/JPY gains are the main focus point so far in Monday trade. We are close to late Sep highs near 150.00. A clean break higher would see attention shift to 150.92, the Aug 1 high. As we noted earlier, US-JP yield/swap rate differentials don't argue for a sustained move higher in USD/JPY beyond 150.00, but these spreads have moved in favor of the USD so far today. BoJ hike odds have fallen dramatically in the first part of trade, with a full hike not priced in until April next year. Oct hike odds are around 20%.

- The USD is ticking up against the rest of the G10, but moves are modest at his stage. EUR/USD is down 0.25%, but still above 1.1700. EUR/JPY is above 175.35 in latest dealings, fresh record highs.

- Focus for the EU session will be French President Macron's cabinet appointments, which largely saw continuity. French bond futures are weaker in the first part of trade.

- AUD/USD is under 0.6600, NZD, near 0.5825. Australian markets are largely out today due to a holiday.

- AUD/JPY is up to 98.75/80, fresh highs back to Jan of this year.

- The data calendar is very light today with only second tier Aust and NZ releases out a short while ago.