IRAN: NY Post Reporter Repeats Claims Of Iranians Arriving In Pakistan Tonight

Apr-24 11:44

Caitlin Doornbos at NY Post: "An Iranian delegation will land in Islamabad tonight as the world wait...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - USDJPY Bulls Still In The Driver's Seat

Mar-25 11:42

- In FX, short-term gains in EURUSD are - for now - considered corrective. Resistance to watch is at the 50-day EMA, at 1.1676. A clear breach of it would signal a stronger reversal. On the downside, the bear trigger is unchanged at 1.1411, the Mar 13 and 16 low. Clearance of this level would resume the downtrend.

- The trend set-up in GBPUSD remains bearish, and recent gains appear corrective. Note that resistance at the 50-day EMA, at 1.3446, has been pierced. A clear break of the EMA would undermine the bearish theme and signal scope for a stronger recovery. This would open 1.3575, the Feb 26 high. Key short-term support and the bear trigger lies at 1.3219, the Mar 13 low.

- The trend direction in USDJPY remains bullish and short-term pullbacks appear corrective. The breach of key short-term resistance at 159.45, the Jan 14 high, confirmed a resumption of the uptrend and has opened the 160.00 psychological barrier next. Initial firm support lies at 159.64, the 50-day EMA.

PIPELINE: Corporate Bond Roundup: Nippon Life, LG Energy Solution on Tap

Mar-25 11:37

- Date $MM Issuer (Priced *, Launch #)

- 03/25 $500M #JFM 5Y SOFR+58

- 03/25 $Benchmark Nippon Life 5Y +120a, 7Y +135a

- 03/25 $Benchmark LG Energy Solution 3Y +150a, 5Y +165a, 5Y SOFR, 10Y +200a

- $24.525B Priced Tuesday, $31.175B/wk

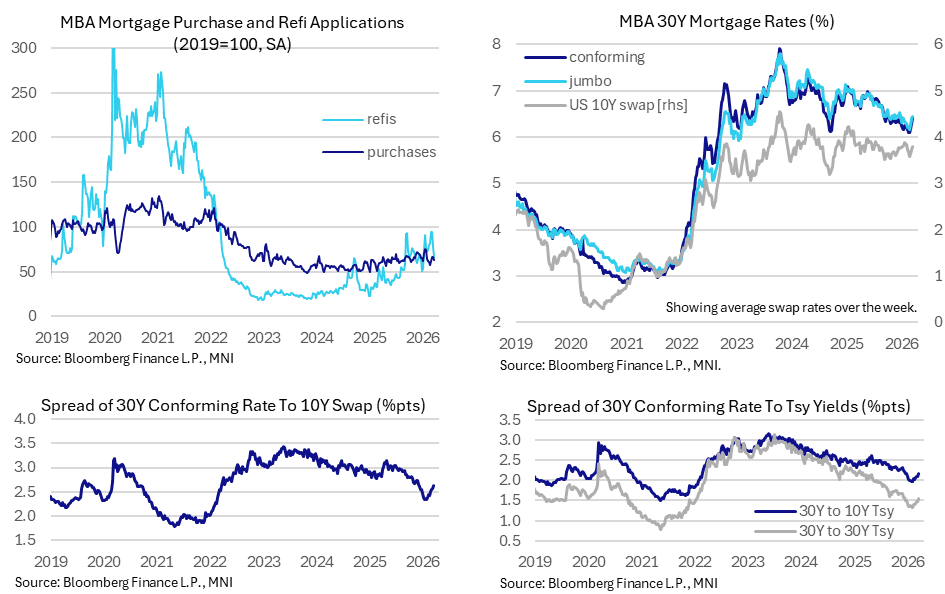

US DATA: Mortgage Applications Slip Further As Rates Climb Again, Spreads Wider

Mar-25 11:17

- MBA composite mortgage applications slipped another -10.5% (sa) last week after -10.9% the week prior, hitting their lowest level since the turn of the year.

- Refis again led this weakness (-14.6% after -18.5%) but new purchase applications also softened (-5.4% after 0.9%) with their largest weekly decline since end-Jan.

- The new purchase applications trend leaves at best flat momentum for housing market activity.

- Higher rates are clearly having an impact, with the 30Y conforming mortgage rate climbing another 13bp after 11bp and 10bp increases in the previous two weeks. It’s a 34bp increase from 6.09% in late Feb in what had been its lowest since Sep 2022.

- A widening in mortgage spreads has been fuelling this rate increase in recent weeks after a material tightening seen through 2H25 and into early 2026.

- The spread of 30Y mortgages to 10Y Tsy yields averaged 217bp last week (from 210bp the week prior) vs high 190s in mid-Jan to early Feb, whilst the spread to 10Y swap rates averaged 264bp (256bp the week prior) vs in the 230s in mid-Jan to early Feb.