US-CHINA: NVIDIA Scrambling To Meet H200 Demand From China: RTRS Sources

Latest from Reuters sources on NVIDIA chip demand from China:

- "Nvidia NVDA.O is scrambling to meet strong demand for its H200 artificial intelligence chips from Chinese technology companies and has approached contract manufacturer Taiwan Semiconductor Manufacturing Co 2330.TW to ramp up production, sources said."

- "Chinese technology companies have placed orders for more than 2 million H200 chips for 2026, while Nvidia currently holds just 700,000 units in stock, two of the people said."

- "The exact additional volume Nvidia intends to order from TSMC remains unclear, they said. A third source said Nvidia has asked TSMC to begin production of the additional chips, and work is expected to start in the second quarter of 2026."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: Eurex Roll Pace (update)

EUREX Roll pace (as of Thursday): The roll will be at the forefront this Week (Expiry 8th Dec).

- Buxl: 6%.

- Bund: 20%.

- Bobl: 10%.

- Schatz: 10%.

- BTP: 6%.

- BTS: 6%.

- OAT: 11%.

US 10YR FUTURE TECHS: (H6) Corrective Pullback

- RES 4: 114-00 Round number resistance

- RES 3: 113-29+ High Oct 17 and a key resistance

- RES 2: 113-23 High Oct 23

- RES 1: 113-22+ High Nov 25

- PRICE: 113-08 @ 07:30 GMT Dec 1

- SUP 1: 113-01 20-day EMA

- SUP 2: 112-37 50-day EMA

- SUP 3: 112-10+ Low Nov 20

- SUP 4: 112-07 Low Nov 5 and a key support

A bullish theme in Treasuries remains intact despite the latest pullback. The recent breach of the 112-31 level, an area of congestion since Nov 5, marks an important short-term bullish development. Note that the contract is also trading above the 20- and 50- EMAs. A resumption of gains would open 113-29+, the Oct 17 high and a key resistance. On the downside, initial support to watch is at 113.01, the 20-day EMA.

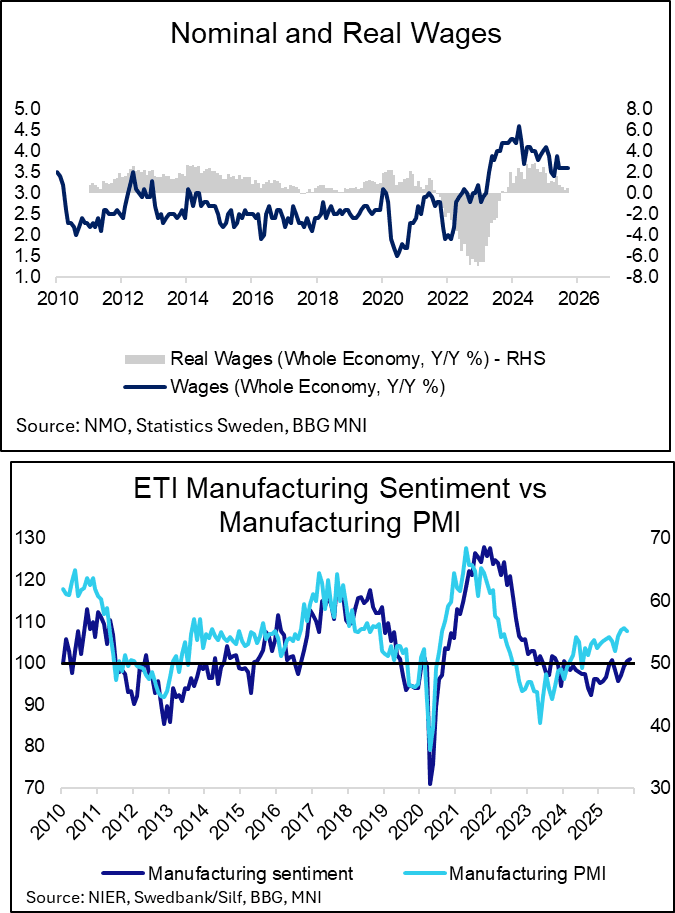

SWEDEN: Wage and Manufacturing PMI Data Consistent With A Cyclical Recovery

This morning’s Swedish data were consistent with the ongoing narrative around an economic recovery. The Riksbank is firmly expected to be on hold at 1.75% for "some time", but today's readings add to the stock of data suggesting medium-term risks to rates are tilted towards hikes.

Real wage growth remains positive, which is expected to support household consumption through the end of 2025 and into 2026.

- Whole-economy nominal wage growth was estimated at 3.2% Y/Y in September, while the National Mediation Office’s (NMO) adjustment to account for retroactive payments predicted growth of 3.6% Y/Y.

- This implied whole-economy real wage growth of 0.5% Y/Y (vs 0.4% prior).

- Private sector wages were estimated at 3.3% Y/Y (vs 3.3% prior), with the NMO’s adjustment predicting growth of 3.5% Y/Y (vs 3.6% prior).

- In the public sector, the NMO’s adjustment played a larger role, with wage growth predicted at 3.9% Y/Y based on an original estimate of 3.2% Y/Y.

The November manufacturing PMI remained comfortably in expansionary territory at 54.6 (vs 55.0 prior). The three analyst estimates submitted to Bloomberg were 55.0, 55.1 and 55.5.

- New orders rose back to 56.7 (vs 55.8 in Oct, 57.7 in Sept), while production eased to 57.6 (vs 60.5 prior). Employment rose to 51.6 (vs 50.9 prior), while future production remained elevated at 66.7 (vs 70.1 prior).