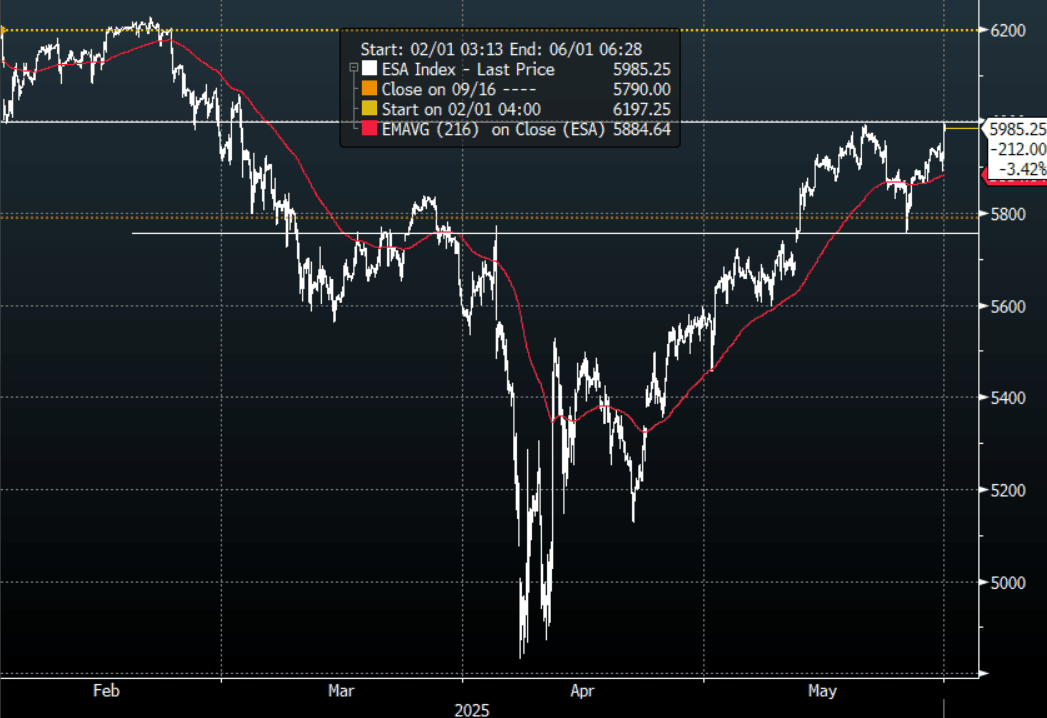

US STOCKS: Nvidia Results And A US Court Ruling Challenge An Underweight Market

The ESM5 Overnight range was 5890.00 - 5952.50, Asia is currently trading around 5985. US stocks traded with a heavy tone overnight but a combination of a very strong quarterly update from Nvidia after the close and reports a U.S. federal court on Wednesday blocked President Donald Trump's "Liberation Day" tariffs from going into effect have seen a surge in early Asian trading currently up around 1.5%.

- (Bloomberg) - “Nvidia continues to generate huge amounts of cash. It had cash flow from activities of $27.4 billion and returned $14.3 billion in cash to shareholders in the quarter.”

- “The company reported $44 billion of revenue for the three months through April 27, up 69% from a year earlier despite the Trump administration blocking sales of its H20 chips to China.”

- FT reports - “ The Trump administration blocking sales to China of software used for designing chips is more of a risk to companies than the broader market. The FT reported that the administration told Cadence, Siemens EDA and Synopsys to stop selling their tech to China.”

- (Bloomberg) - “Nvidia CFO Colette Kress said on the earnings call that the company believes the Chinese AI accelerator market will grow to $50 billion and that losing access will “have a material adverse impact” on its business in the future, while benefiting competitors in China and elsewhere.”

- Stocks trade like a beachball being held under water, the move looks overdone but momentum type funds and share buybacks have kept the market well supported.

- The price action continues to point to a market that is begrudgingly underweight, this move in price will force PM’s back into the market.

In the short-term stocks continue to look overbought but it's very hard to ignore this price action. Dips should be expected to be met with demand, the first buy-zone is back towards the 5600/5700 area.

Fig 1: SPX Hourly Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Flat, RBA Kent Speech Later, Q1 CPI Tomorrow

ACGBs (YM +1.0 & XM +0.5) are little changed after US tsys finished near session bests Monday, 2-5bps richer.

- Underlying bid as Dallas Fed's Texas Manufacturing Survey for April -- the weakest since the start of the Covid pandemic in 2020, as tariff uncertainty weighed heavily on manufacturers in the district, while price pressures remained elevated.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at -4bps.

- Swap rates are little changed as well.

- The bills strip is +2 across contracts beyond the 1st (flat).

- RBA Assistant Governor Kent will speak later today, 12:05pm local time (0305BST). His speech per the RBA website is as follows: "Keynote speech by Christopher Kent, Assistant Governor (Financial Markets) - Australia's External Position and the Evolution of the FX Markets - at Bloomberg, Sydney." Monetary policy is therefore unlikely to be covered. Note the next central bank meeting for the RBA is on 19-20 of May.

- RBA-dated OIS pricing is 1-3bps softer across meetings today. A 50bp rate cut in May is given a 13% probability, with a cumulative 119bps of easing priced by year-end.

- Today, the local data calendar will be empty ahead of tomorrow’s Q1 CPI.

- The AOFM plans to sell A$1200mn of the 2.75% 21 June 2035 bond on Friday.

NEW ZEALAND: Nascent Signs Labour Market Recovering

Filled jobs rose 0.2% m/m in March but are still down 1.5% y/y after being flat and down 1.6% y/y in February. However, the 3-month annualised rate at 0.4% turned positive for the first time since April 2024, signalling that Q1 employment may be flat to slightly higher on the quarter when labour market data is released on May 7.

NZ employment q/q%

- Labour demand remains weak but is showing some tentative signs that it has begun to gradually recover. 3-month momentum is improving for filled jobs and also SEEK job ads which rose 8.7% annualised in March. While vacancies are still down 15.4% y/y, they are off the low of -34.8% in June.

- SEEK applicants/job index shows that labour supply remains robust. It rose in the 3 months to February and was up 31.3% y/y with 3-month momentum annualised at almost 19%.

- The increase in March filled jobs was broad based across sectors with primary rising 0.4% m/m, goods-producing +0.1% and services +0.2%. Construction has taken the brunt of labour shedding over the last year down 6.1% y/y followed by admin & support services -5.7% and manufacturing -2.2%, while health care is up 1.7% y/y.

- Young people have seen the largest losses with filled jobs of 15-19 year olds down 10% y/y, while for 35-39 years they’re up 2.2% y/y.

NZ filled jobs vs SEEK job ads

US: Trump To Ease Auto Tariff Burden - Per WSJ

Headlines have crossed from the WSJ that US President Trump will soften tariffs on the automotive sector. The WSJ notes that: "President Trump is expected to soften the impact of his automotive tariffs, preventing duties on foreign-made cars from stacking on top of other tariffs he has imposed and easing some levies on foreign parts used to manufacture cars in the U.S., according to people familiar with the matter." (see this link).

- Reuters added that these actions are expected to take place tomorrow, per comments from the Whitehouse(which should be Tuesday US time).

- At this stage the market reaction hasn't been large in the US equity futures space, which still sit modestly down in the red (but up from session lows).

- We did see late last week hints that tariff reprieve could be coming for the autos sector.