NORWAY: Norges Bank FX Purchases Set To Increase From Next Year

Oct-15 14:01

Based on the details of Norway’s 2026 budget proposal, analysts expect Norges Bank daily NOK purchases to increase from next year. Early estimates we have seen range from NOK600-800mln/day, up from NOK276mln at present. These figures will be refined once budget negotiations conclude, likely in December.

JP Morgan:

- “The deficit is [presumably] larger than Norges Bank’s assumption, suggesting a marginal hawkish impact.”....“The fiscal impulse is estimated at 0.4%, while a separate estimate of fiscal thrust is just 0.1%”…“The latter estimate tends, however, to under-estimate the actual impact. We expect 2026 fiscal thrust at 0.5%”

- “We estimate that the Budget, in isolation, indicates net NOK purchases of 0.67bn/day, on average, in 2026. On top of the projections from the Budget, Norges Bank’s profit transfer to the oil fund needs to be taken into account ….Assuming profits amount to roughly the same as in 2025, this gives total NOK buying of ~0.8bn/day….For the remainder of 2025, we see upside risk to the current pace of 0.276bn/day NOK buying.”

- “Bear in mind that increased NOK purchases by Norges Bank does not imply that total net NOK demand increases in the market. The reason is that prior to Norges Bank’s NOK purchases the private petroleum companies convert taxes—which are in foreign currencies —to NOK. These taxes, which are much larger in size, are now expected to decline compared to 2025”

SEB:

- “The budget underscores the general notion that fiscal demand impulses will ease, but overall spending is broadly in line with Norges Bank’s estimate and should thus not impact the monetary policy outlook.”

- “The need for daily NOK purchases will increase in 2026. On the one hand, the non-oil budget deficit will decrease by NOK 35bn to 452bn, but on the other hand the fall in NOK-denominated petroleum income will be larger. Our first take given the budget translates into NOK purchases of around 600-650mn per day on average.”

- “The budget implies an underlying borrowing need of NOK 96bn, which is broadly stable from 2025. We believe Norges Bank wants to keep supply broadly stable while building up the cash reserve if possible. Hence, we expect a stable borrowing interval of NOK 95-105bn, or possibly NOK 100-100bn. “

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: Call Spread vs Put Spread

Sep-15 14:01

SFRV5 96.43/96.62cs vs 96.25/96.12ps, bought the cs for 1 in 4k.

EUROZONE DATA: Soft Imports Take Some Of The Edge Off A Solid June [2/2]

Sep-15 13:52

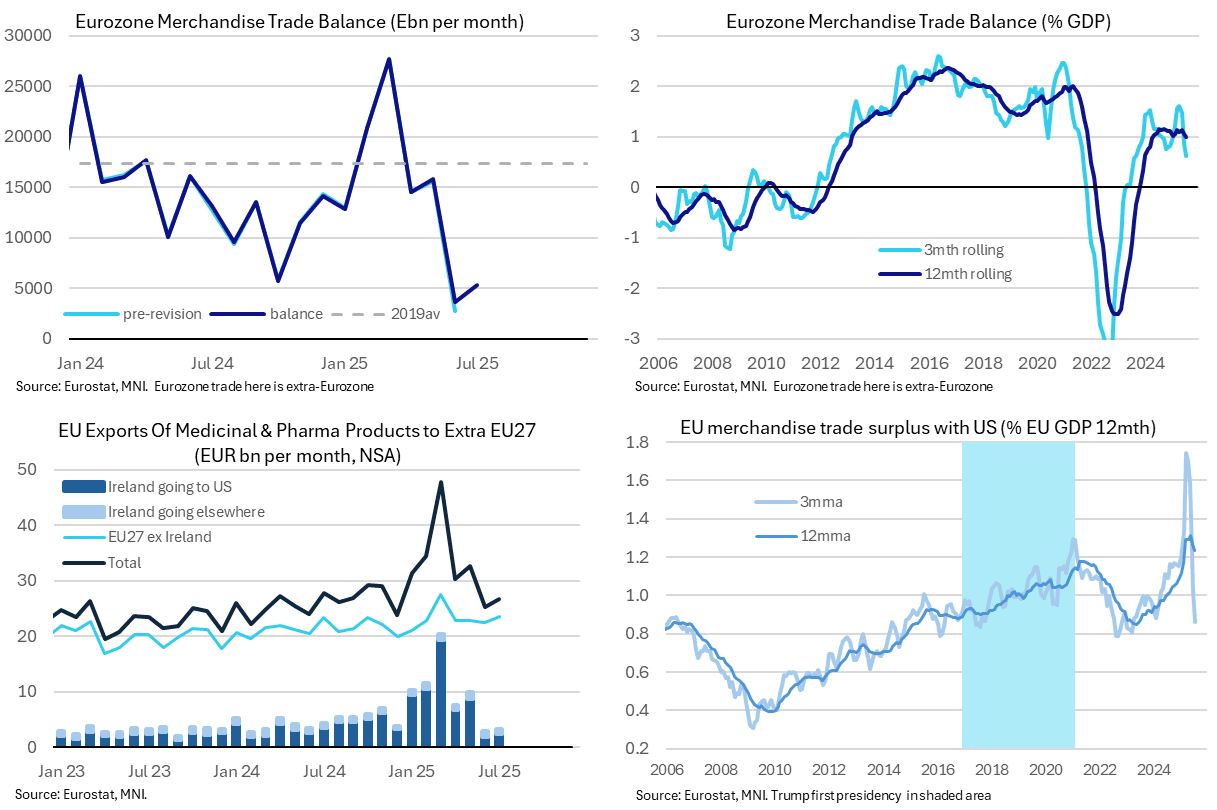

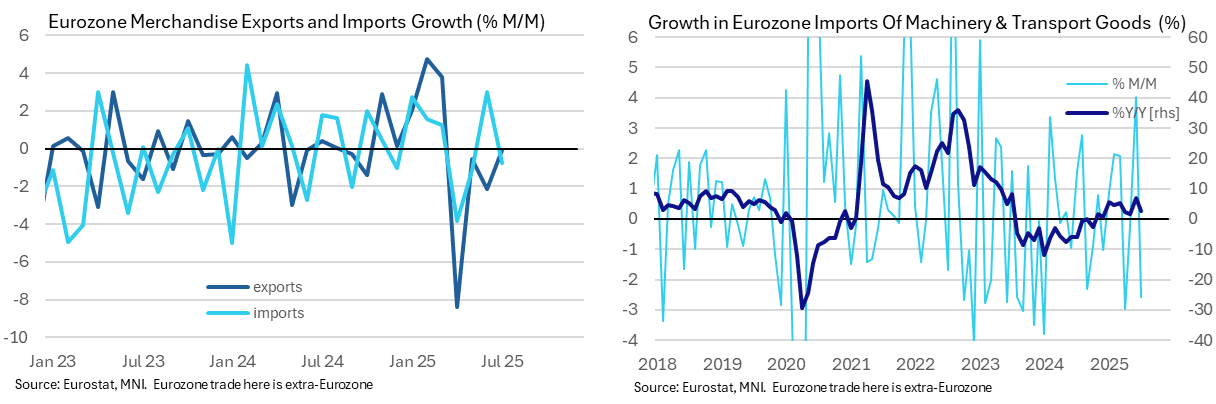

- The modest widening in the surplus came as imports (-0.8% M/M) fell by more than exports (-0.1% M/M).

- It sees imports unwind part of the 3.0% M/M increase in June in what was a rare solid reading compared to recent months.

- An important caveat when it comes to digging into import details for domestic demand implications -- the miscellaneous category again shows a surge but this was revised away last month as these unclassified items are eventually correctly allocated.

- Specifically, the miscellaneous category surged 172% from to E6.8bn in Aug from a typical E2.5bn in July, with the latter initially reported at E7.1bn.

- With that in mind, monthly declines are currently seen as being led by the typically volatile raw materials category (-7.5% M/M) along with manufactured goods (-2.8%) and food, drinks & tobacco (-1.8%).

- We tend to focus on machinery & transport within manufactured goods, and this currently shows a disappointing -2.6% M/M to undo a sizeable part of June’s 4.0% increase. In doing so, it crimped annual growth in this nominal category to just 2.5% Y/Y.

EUROZONE DATA: Trade Data See Further Post Tariff Front-Running Adjustment [1/2]

Sep-15 13:51

- The Euro area goods trade surplus surprised lower for the third time in four months, with a seasonally adjusted E5.3bn in July (cons E12.0bn expected) after an upward revised but still low E3.7bn (initial E2.8bn) in June.

- The Bloomberg consensus figure again consisted of only three responses, so we wouldn’t put too much weight on the surprise and instead focus on the direction.

- The trend is one of clear narrowing in surpluses, with an average E4.5bn in Jun/Jul, E15.2bn in Apr/May and E24.3bn in Feb/Mar on peak tariff front-running. For a sense of a more ‘typical’ surplus, it averaged E14.1bn per month through 2024.

- Alternatively, it leaves the latest three-month goods surplus worth approximately 0.6% GDP vs a peak of 1.6% GDP in the spring after an average surplus of 1.1% GDP through 2024.

- The more detailed NSA data show that Irish pharmaceutical exports to the US registered a second small month of E2.4bn after just E1.8bn in June. It's continued payback from a surge in Q1 when exports summed to E39bln vs the E44bln through 2024 as a whole. As such, it may not necessarily be surprising but it's still notable and could see similarly small readings ahead with Jan-Jul exports already worth a cumulative E58.7bn.