US DATA: No Sign Of Alarm In Claims But Govt-Sensitive Areas Drift Higher

Initial jobless claims were essentially as expected whilst continuing claims were better than expected in a payrolls reference period. There is no sign of unusually large government layoffs although continuing claims for most sensitive areas are drifting higher in a hint of re-hiring frictions.

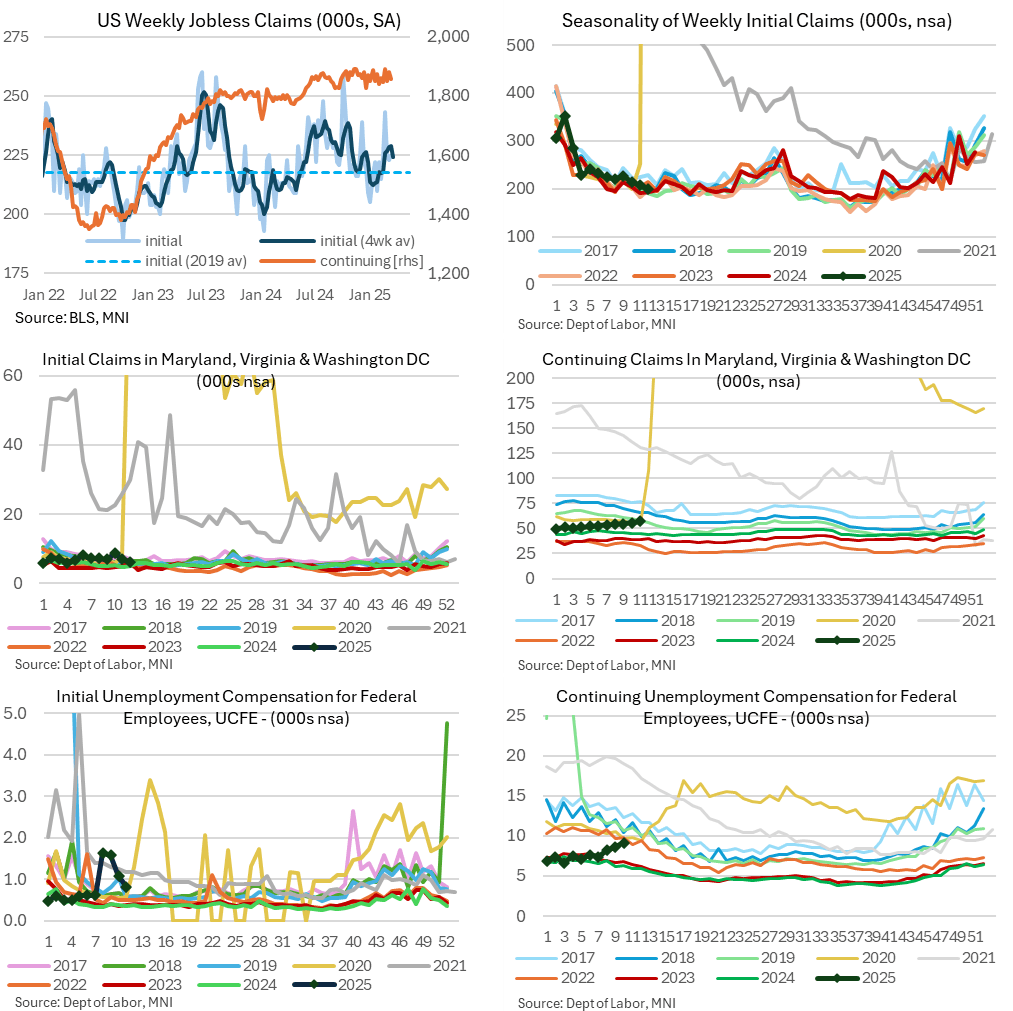

- Initial jobless claims: 224k (sa, cons 225k) in the week to Mar 22 after an upward revised 225k (initial 223k).

- The four-week moving average dropped 5k to 224k, the lowest since mid-Feb and closer to the 218k averaged in 2019 in a sign of a still relatively tight labor market.

- Government layoffs have continued to ramp up anecdotally (although the deferred resignation scheme, the single most impactful approach so far, won’t show in claims until Oct) but there doesn’t look to be any major sign of higher claims that show up on a macro level.

- Our crude proxy for capturing federal government layoffs is to look at Maryland, Virginia and Washington DC, initial claims for which fell modestly last week from 7k to 6k for their lowest since late January.

- Note that the lagged series for those seeking unemployment compensation for federal employees (UCFE) also fell from 1.1k to 0.8k in the week to Mar 15 for its lowest in a month. See the below charts for how these figures are back easily within typical values.

- Continuing claims: 1856k (sa, cons 1886k) in the week to Mar 15, covering a payrolls reference period, after a downward revised 1881k (initial 1892k).

- The decline sees continuing claims pullback from what had been close to three-year highs, and offers a relatively more favorable comparison of prior payrolls reference periods (following 1847k in the relative week for Feb and 1849k for Jan).

- Whilst initial claims in Maryland, Virginia and Washington are within typical levels, the continuing series is slowly drifting higher compared to past years which hints at difficulties in rehiring for a sector that typically has low churn rates.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CAD: FX Exchange traded Option

CADUSD 69p, sold at 12.00 in ~2.2k.

ECB: Schnabel Suggests Wider ASWs May Push Up r*

Schnabel's speech argues that declining convenience yields (which can be proxied by widening asset swap spreads) will put upward pressure on the Eurozone r* going forward, with market participants valuing the "liquidity and safety services of government bonds less than they did in the past". This can also be seen in the repo market, where "steady and measurable rise in overnight rates and a convergence across collateral classes" have been observed.

She highlights three familiar factors contributing to the rise in bond free float in the Eurozone and the US:

- "Most importantly, net borrowing by governments remains substantial".

- "Rising geopolitical fragmentation is likely to be contributing to a drop in demand for government bonds in some parts of the world"..."In the United States, for example, there has been a marked decline in the share of foreign official holdings of US Treasury securities since the global financial crisis".

- "Central banks are in the process of normalising their balance sheets"..."Unlike when central banks announced large-scale asset purchases, the effects of quantitative tightening (QT) on yields are likely to materialise only over time, as many central banks take a gradual approach when reducing the size of their balance sheets".

Note: Convenience yield is defined as the "yield that investors are willing to forgo in equilibrium" for "money-like convenience services that safe and liquid assets, such as government bonds, provide to market participants".

MNI: US FEB PHILADELPHIA FED NONMFG INDEX -13.1

- MNI: US FEB PHILADELPHIA FED NONMFG INDEX -13.1