US DATA: No Real Surprises For ADP As Confirms Return Of Declining Employment

Dec-03 13:36

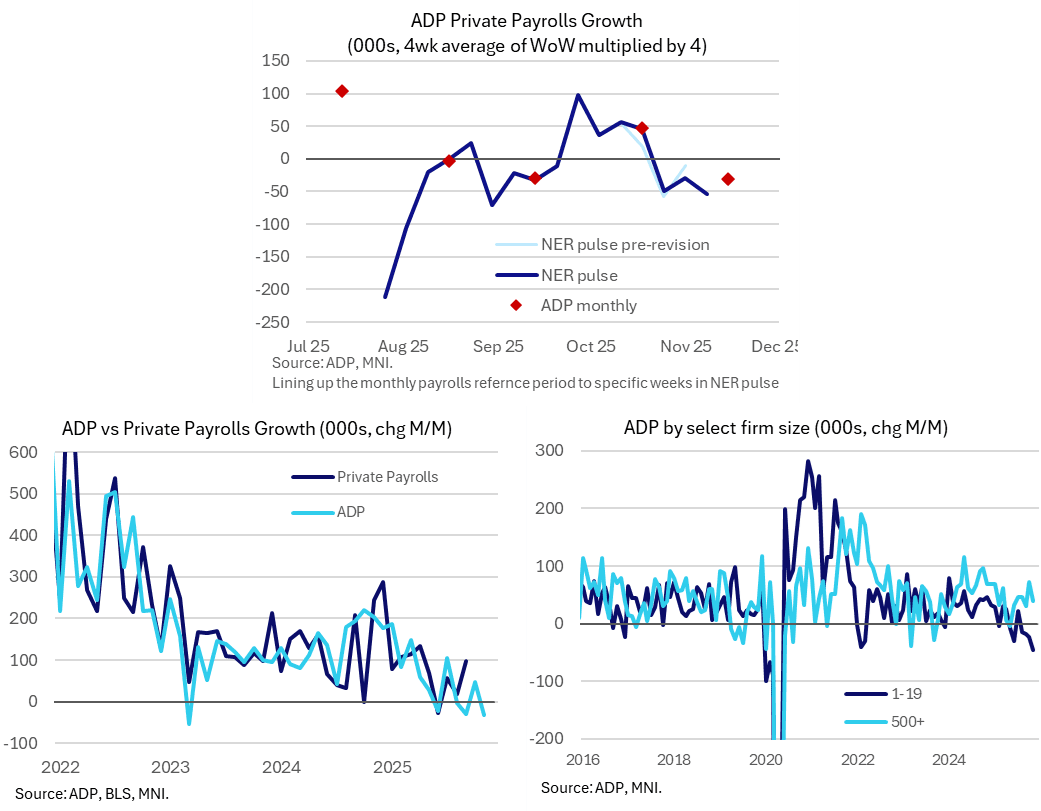

The monthly ADP report in November turned out closer to the weakness implied by its own weekly tracker than Bloomberg consensus which had surprisingly eyed a small increase on the month. It confirms a return to a monthly decline in private employment, with a third decline in the past four months.

- ADP employment growth “surprised” lower at -32k (Bloomberg cons 10k) in November whilst the October increase was revised up from 42k to 47k.

- However, as noted in our preview this morning, this had looked an odd consensus figure considering last week’s ADP NER Pulse update saw an average weekly change of -13.5k in the four weeks up to Nov 8, i.e. closer to a -55k decline on a rolling monthly basis.

- In theory, this monthly report should have offered limited new information from that in the weekly series as, broadly mimicking the BLS payrolls report, its reference period is the week including the 12th of the month.

- As we wrote: “The weekly series is prone to revisions although we’d be surprised if they were strong enough to materially alter a weak trend that has seen three weeks averaging -11k (on the same four-week rolling basis, i.e. closer to -45k in monthly terms). “

- Further, the previous current vintage for the weekly tracker had pointed to a ~46k increase back in October so today’s modest upward revision also chimes there.

- Back to today’s monthly report, smaller firms clearly felt pressure in November, with -46k for those with 1-19 employees and -74k for those with 20-49. The offsetting 90k increase elsewhere was led by a 39k increase for those with 500+ employees after a strong 73k increase for the latter in October.

- From today's press release (link): "Job creation has been flat during the second half of 2025 and pay growth has been on a downward trend. November hiring was particularly weak in manufacturing, professional and business services, information, and construction.

- * Hiring has been choppy of late as employers weather cautious consumers and an uncertain macroeconomic environment. And while November's slowdown was broad-based, it was led by a pullback among small businesses."

- The broader momentum in the series should be viewed as an important indicator for jobs growth, with the three-month average slowing through the year to date (200k in Dec 2024, 139k in Mar, 22k in Jun, 24k in Sep and -4k most recently in Oct).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PIPELINE: Corporate Bond Update: Novartis Capital 7Pt Adding Pressure to Tsys

Nov-03 13:34

Adding Novartis 7Pt issuance with prior for comparison:

- Date $MM Issuer (Priced *, Launch #)

- 11/03 $Benchmark Alphabet 8-pt jumbo**: 3Y +60a, 3Y SOFR, +5Y +70a, 7Y +80a, 10Y +90a, 20Y +100a, 30Y +110a, 50Y +135a (massive debt issuance includes $6.5B over 6 tranches: 3Y, 6Y, 7Y, 13Y, 19Y and 39Y).

11/03 $1B Neptune Bidco 5.5NC2 - 11/03 $Benchmark Novartis Capital 7Pt**: 3Y +55a, 3Y SOFR, 5Y +70a, 7Y +75a, 10Y +80a, 20Y +80a, 30Y +90a

- 11/03 $Benchmark UBS 8NC7 +120a, 21.5NC20.5 +115a

- 11/03 $Benchmark Peoples Republic of China 3Y, 5Y

- 11/03 $Benchmark Qatar 3Y +45a, 10Y Sukuk +55a

- 11/03 $Benchmark Kingdom of Jordan 7Y investor calls

- **Piror Alphabet issuance for comparison: $5B on April 28 of this year ($750M 5Y +32, $1.25B 10Y +47, $1.5B 30Y +62, $1.5B 40Y +70) a long stretch since issuing $10B on Aug 3 2020 ($1B 5Y +25, $1B 7Y +45, $2.25B 10Y +58, $1.25B 20Y +73, $2.5B 30Y +88 and $2B 40Y +108)

- **Prior Novartis issuance for comparison: $3.7B on September 16, 2024 ($1B 5Y +45, $850M 7Y +57, $1.1B 10Y +67, $750M 30Y +77)

EURIBOR OPTIONS: Put Condor buyer

Nov-03 13:29

0RH6 97.87/97.75/97.68/97.56p condor, bought for 2.5 in 4k.

GLOBAL POLITICAL RISK: Week Ahead 3-9 November

Nov-03 13:27

Download Full Report Here

Monday 3 November:

- France: Debate in the National Assembly resumes on the 2026 state budget and social security budget. With thousands of amendments needing to be discussed and voted on, the Tuesday deadline for voting on the revenue part of the state budget is at risk of being missed. If this is the case, the debate on the revenue section will be paused until 13 November, raising the prospect of the entire budget failing to be passed before Christmas (the final deadline that would allow the Constitutional Court to review the legislation before being sent to President Emmanuel Macron’s desk for final sign-off).