ASIA STOCKS: NKY and KOSPI Up Cautiously Whilst SE Asia Losses Mount

With China out, Asia looked to South Korea and Japan as the main markets opened Monday. The AXIOS report ended a weak start with the NIKKEI touching 53,200 early before rebounding back above 54,000, before settling around 53,500 and gains of +0.85%. AI stocks continued to perform from the positive spillover from Microsoft's AI partnership in Japan. Banks continue to deliver modest returns as the higher yield environment bodes well for their balance sheets.

In Korea, Samsung led the charge with gains of over +3.6% Monday driving the KOSPI higher by +1.3%. Early trading was bolstered by reports that the South Korean government is considering a new supplementary budget for the second half of the year to cushion the economy against high oil prices and supply chain disruptions. Banks are performing also given the higher yield environment perceived to have a positive impact. Gains were tempered in the afternoon with investors wary of the April 6 deadline

Malaysia, Thailand and Indonesia have all had a weak start to the trading week with losses of around -0.40% to -0.80% on the ongoing Middle East concern. The woes for the JCI started with concerns over the fiscal spend due to the government's growth objectives, was further pressured by concerns raised by the index provider MSCI (and hence rating agencies) and now the price of oil. This sees the JCI floundering with year to date losses of -19% whilst projecting a full year growth rate of around 5%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE 3-YEAR TECHS: (H6) Near-Term Weakness Extends

- RES 3: 96.700 - High Sep 12

- RES 2: 96.260 - Congestion High Nov 19 -24 ‘25

- RES 1: 96.925 - High Jan 9 and a key short-term resistance

- PRICE: 95.545 @ 15:51 GMT Mar 06

- SUP 1: 95.504 - 3.0% Lower Bollinger Band

- SUP 2: 95.470 - Low Mar 03

- SUP 3: 94.731 - 1.0% 10-dma envelope

The bearish primary trend structure in Aussie 3-yr futures firmed after a poor week for prices. The bear mode set-up in MA studies is highlighting a dominant downtrend. Resistance to watch remains 95.925, the Jan 9 high. A clear break of it would signal a short-term reversal. For bears, weakness through year-to-date lows at 95.560 has prompted further downside, opening vol-band support into 94.731.

MACRO ANALYSIS: MNI US Macro Weekly: War Shock Meets Weak Jobs Data

We've just published our US Macro Weekly - Download Full Report Here

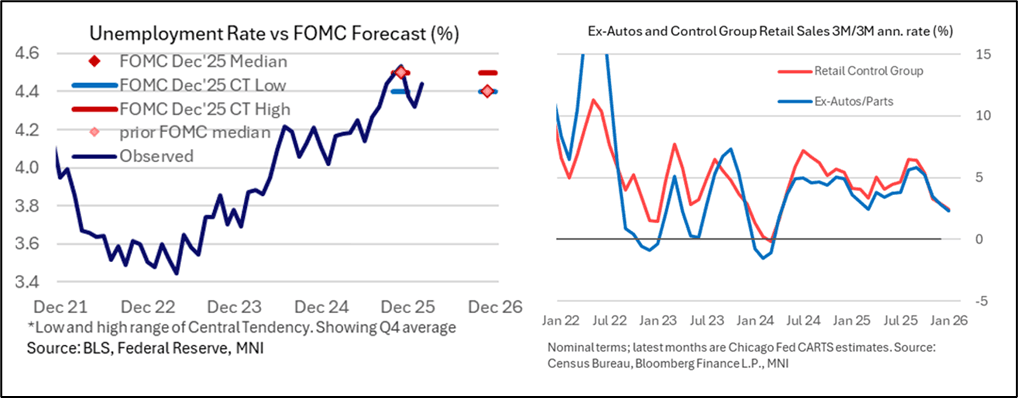

- In the key release of a tumultuous week that was overshadowed by geopolitical developments, both the establishment and household surveys disappointed in the February Employment report with a 92k NFP drop, an unemployment rate rise to 4.44%, and large lower revisions.

- But survey quirks and one‑offs complicate interpretation and it comes after a relatively solid January report. As such it doesn't appear to have greatly impacted FOMC participants' overall views on the rate outlook as we head into the pre-March FOMC blackout period.

- Indeed it sounds as though all of the FOMC participants will have to weigh the surprisingly soft report alongside the potential macro implications of the conflict in the Middle East before coming up with a synthesis and forming March SEP projection updates.

- Soaring energy prices and broader market uncertainty over the war in the Middle East started over the weekend saw rate cut pricing evaporate. Cumulative pricing at one point suggested that a rate cut would have to wait until after the September FOMC, having last Friday pointed to about a 50/50 chance of a second 25bp cut by that point (after July).

- End-2026 pricing briefly touched ~32.5bp of cuts in the hour prior to the release of the February employment report, a 28bp repricing vs prior to the US-Iran conflict. The unexpected drop in payrolls and uptick in the unemployment rate was enough to bring a September rate cut to fully priced (29bp), even if a cut as soon as July remained slightly elusive.

- Otherwise, data were mixed. Import prices remained firm, with ex‑petroleum import prices posting their strongest four‑month stretch since 2024 amid tariff effects and fading China concessions.

- Growth indicators softened, with GDPNow falling to 2.1% on weaker expected consumption. Business surveys diverged: ISM Manufacturing held gains but saw a sharp jump in Prices Paid, while ISM Services surprised strongly with broad‑based strength and cooling prices; S&P PMIs pointed to ~1.5% Q/Q growth.

- Retail sales and consumption signals were mixed, with headline and category breadth softening despite a modest Control Group gain.

- The week ahead features key inflation releases, with February CPI (Wed) and January PCE (Fri) central to shaping expectations before the March 17–18 FOMC meeting and new SEP; additional data in the week to come include GDP revisions, JOLTS, durable goods, and housing indicators.

US PREVIEW: US Week Ahead: Inflation Releases Feature Ahead Of FOMC Meeting

The coming week brings key US inflation and spending data ahead of the Fed's mid-March meeting.

- February headline CPI (Wednesday, 0830ET) is seen accelerating slightly to 0.3% M/M from January's 0.2%, with core ticking down to 0.2% from 0.3%. Recall that January's report saw strong supercore (0.6%) inflation in excess of overall core services (0.4%), and offset by a milder than anticipated (0.0%) core goods reading on the back of a large fall in used vehicle prices. Some of those dynamics were expected to have reversed in February, not least including a pickup in housing inflation though volatile categories such as airfares (6.5% in January) reverting, though there will be attention on whether ex-autos core goods inflation continues to accelerate given tariff passthrough concerns.

- Friday's PCE report (0830ET) is a little stale being for January, but the price index will be in focus as the Fed's preferred inflation gauge. Core PCE prices are seen registering a 0.4% M/M rise for a second consecutive month, keeping the Y/Y rate at 3.0%. The just-released January retail sales report suggested a continued deceleration in goods consumption momentum (fell 0.5% in real terms in December's PCE report), putting continued pressure on services consumption (rose 0.3% in real terms in December) to underpin the "solid consumer" narrative. Going into the PCE report, overall real personal spending is seen flat in January, vs December's 0.1% gain.

- Other key releases include revised Q4 GDP figures, and January JOLTS and durable goods orders data.

- There are no FOMC speaking appearances in the coming week as it's the pre-meeting blackout period (though Gov Bowman appears, she will be speaking on banking supervision and not on monetary policy.)

Date | ET | Impact | Event |

9 Mar | 1100 | ** | NY Fed Survey of Consumer Expectations |

10 Mar | 600 | ** | NFIB Small Business Optimism Index |

10 Mar | 855 | ** | Redbook Retail Sales Index |

10 Mar | 1000 | *** | NAR existing home sales |

10 Mar | 1200 | *** | USDA Crop Estimates - WASDE |

11 Mar | 700 | ** | MBA Weekly Applications Index |

11 Mar | 830 | *** | CPI |

11 Mar | 830 | Fed Vice Chair Michelle Bowman | |

11 Mar | 1400 | ** | Treasury Budget |

12 Mar | 830 | *** | Jobless Claims |

12 Mar | 830 | *** | Housing Starts |

12 Mar | 830 | ** | Trade Balance |

12 Mar | 1100 | Fed Vice Chair Michelle Bowman | |

13 Mar | 830 | *** | GDP / PCE Quarterly |

13 Mar | 830 | *** | Personal Income and Consumption |

13 Mar | 830 | ** | Durable Goods New Orders |

13 Mar | 1000 | *** | JOLTS jobs opening level |

13 Mar | 1000 | *** | U. Mich. Survey of Consumers |