US DATA: NFP Recap: Lower U/E Rate Counters Tepid Jobs, Quality Concerns Remain

Jan-09 19:58

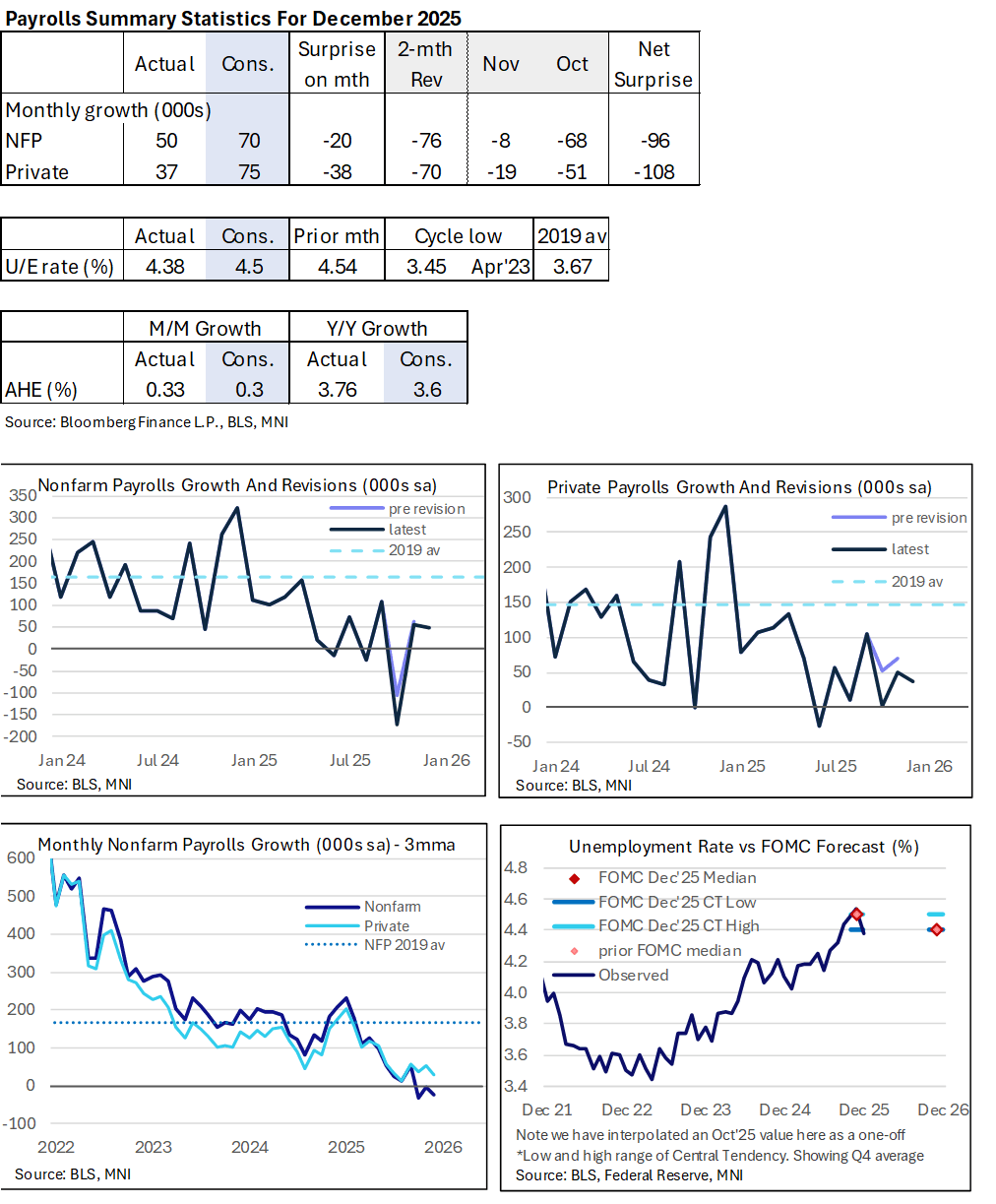

- Nonfarm payrolls growth was softer than expected in Dec at 50k (cons 70k) and with a larger downward surprise for private payrolls at 37k (cons 75k).

- The solid two-month downward revisions (-76k for NFP) were concentrated back in Oct (-68k) and driven by the private sector with -70k of which -51k was in Oct.

- Latest three-month trends: nonfarm -22k over three months and 15k over six months, private 29k over three months and 43k over six months.

- Private payrolls continued to see a large contribution from the cyclically insensitive health & social assistance sector: strip this out and private payrolls would have averaged -19k over the past three months, with only one of the past eight months seeing net job creation.

- Colder than usual early December weather likely weighed although we suspect the impact is modest.

- The household survey meanwhile showed several signs of improvement from November's, even if that largely just reversed some weakness seen on survey- and government-shutdown related distortions.

- The unemployment rate fell back to 4.375% in Dec after a downward revised 4.54% in Nov (initially 4.56%) and 4.49% in Oct (initially 4.50%). Seasonal adjustment factors were updated in annual revisions covering the past five years.

- The u/e rate averaged 4.47% in Q4 (using an interpolated value for Oct) to match the 4.5% the median FOMC participant forecast in both the Sept and Dec SEPs. However, seven FOMC members had looked for 4.6-4.7% across Q4 vs three in September as dovish momentum shifted.

- Some notable findings with the household survey include the biggest drop in unemployment since Mar 2022 (-278k after increasing a cumulative 176k over Sep-Nov) and temporary layoffs falling 73k after a 158k two-month increase.

- Average hourly earnings meanwhile were on the solid side as they increased at 0.325% M/M, considering perceived skew to downside risks to consensus of 0.3% and an upward revision. However, growth of 3.8% Y/Y and 4.0% annualized in Q4 won’t trouble the Fed from a unit labor cost angle with productivity still increasing rapidly.

- Data quality concerns are still elevated though, particularly with the household survey response rate barely increasing from November’s record low.

- Jobs growth may have disappointed but the drop in the u/e rate has seen near-term rate FOMC cut prospects trimmed further after hawkish shifts throughout the week on data and oil prices. It sees a cumulative 12.5bp of cuts priced for Apr vs 14.5bp pre NFP and 18.5bp prior to Wednesday’s strong ISM services report. A next cut is still fully priced for June, only just at 25.5bp, the first meeting under a new Fed Chair.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Powell Questioned on Why the FOMC Didn't Wait Until January

Dec-10 19:57

- Why did the Committee cut today instead of waiting until January? Powell says "in terms of inflation, it's coming in a touch lower" and the labor market cooling has continued, including that payrolls have been overstated and have been negative on an adjusted basis since April:

- "In October, I said that there was no certainty of moving. And that was indeed correct. I said it's possible you could think about it that way, but I was careful to say other people could look at it differently. So why do we move today? You know, I would say point to a couple things. First of all, gradual cooling in the labor market has continued. Unemployment is now up three tenths from June through September. Payroll jobs averaging 40,000 per month since April. We think there's an overstatement in these numbers by about 67,000 so that would be negative 20,000 per month. And also, just to point one other thing, surveys of households and businesses both show declining supply and demand for workers. So I think you can say that the labor market has continued to cool gradually, maybe just a touch more gradually than we thought."

FED: Powell Says Rate Hike Not Anybody's Base Case as Next Move

Dec-10 19:52

- Powell frets that the upcoming payrolls data could be distorted due to the impact of the government shutdown on data collection - particularly the Household Survey of employment. "We are going to get data, but we are going to have to look at it carefully and a somewhat skeptical eye by the January meeting. notwithstanding that, we will have a lot of the December data by January. So, I am saying what we get, for example, for CPI, or for the household survey, we are going to look at that really carefully, and understand that it may be distorted by very technical factors."

- Asked if risks to rates are two-sided from here: "I don't think that a rate hike is anybody's base case at this point - I'm not hearing that."

FED: Powell on the Divide Within Committee

Dec-10 19:49

- On the divide within the Committee and what it would need to see to cut rates in January, Powell:

- "Everyone around the table at the FOMC agrees that inflation is too high and we want it to come down, and agrees that the labor market has softened and that there's further risk. Everyone agrees on that where the difference is is, how do you weight those risks, and what does your forecast look like? ... The discussions we have are as good as any in my 14 years at the Fed. They are very thoughtful, respectful. We have people with strong views, but we come to a place to make a decision. We came to a decision today, 9 out of 12 supported it, so fairly broad support. But it is not like the normal situation where everyone agrees on the direction and what to do. It is more spread out."

- "In terms of what it would take, we all have an outlook in terms of what is going to come, but I think ultimately having cut 75 [basis points], the effects of the 75 basis points will only begin to be coming in. As I said before a couple times, we are well positioned to wait to see how the economy evolves. We will have to see. We will get quite a bit of data."