CHINA: News Reports on Potential Property Stimulus

- BBG is reporting that new measures are being considered to bolster the property sector, where prices are in their fourth year of deflation.

- The report suggests that the housing ministry is considering measures such as mortgage subsidies for new home buyers, an increase in income tax rebates for mortgage borrowers and lowering home transaction costs.

- The new 5-Year plan is focused particular on the consumer and domestic demand. Given the importance of real estate to families, the downturn has fed sharply into decreased consumption patterns (retail sales trending around +3% versus 5-Year average of +4.9%).

- FITCH Ratings last month warned about bank's profitability given their exposure to property as bad loan books continue to expand.

- Whilst no announcements as yet have been forthcoming, it is believed it has been consistently one of the cornerstone discussions at recent party meetings.

- This comes at a time when moderate policy adjustments seem aimed at driving bond yields down. The PBOC has resumed modest purchases of government bonds, having been sidelined for 2025.

- The potential policies indicated could translate to further issuance by the government, ultimately requiring more intervention to keep bond yields in check. The size of the problem is significant yet the response is likely to be gradual.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: 10Y Climate Transition Note Greeted With Lacklustre Demand

Japan sold ¥300bn of 10-year climate transition notes at a cut-off yield that was lower than expectations, signalling lacklustre investor demand.

- The cut-off yield was 1.680%, compared with 1.695% estimated by traders in a Bloomberg survey.

- The bid-to-cover ratio was 3.56x, compared with 3.31x in October 2024, the last time the government sold the bonds.

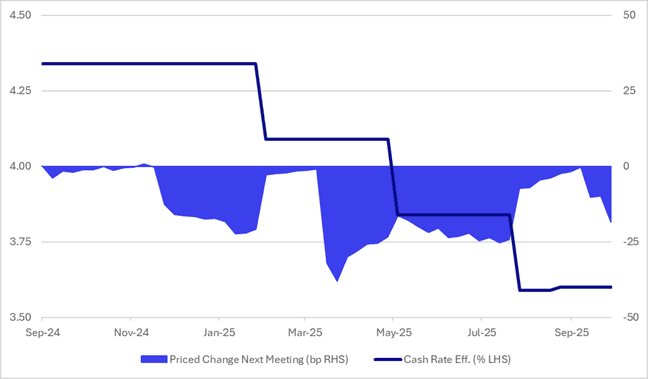

AUSSIE BONDS: Richer But Market Losing Its Conviction About Nov 4 Cut

ACGBs (YM +2.5 & XM +4.0) are stronger and at session highs on another data-light day. The local data calendar remains fairly quiet throughout the week.

- Cash US tsys are slightly mixed, with a flattening bias, in today’s Asia-Pac session.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at +13bps.

- Today’s ACGB auction of the Jun-54 bond showed strong demand, with the weighted average yield printing 0.92bps through prevailing mids and the cover ratio jumping to 4.0533x from 3.3500x from the previous auction. The strong demand came despite the bond’s outright yield being 20-25bps lower than the previous auction and around 30bps below the peak reached in May.

- The bills strip bull-flattened, with pricing flat to +2.

- Despite firming slightly in recent days, RBA-dated OIS pricing remains 7–13bps softer across meetings compared with pre-jobs data levels last week.

- A 25bp rate cut in November is now assigned a 68% probability (peak 80%, pre-data 38%), with a cumulative 23bps of easing (peak 25bps, pre-data 13bps) priced by year-end.

- Compared with the lead-up to previous cuts in this easing cycle, the market appears less certain than usual about a November 4 move.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI

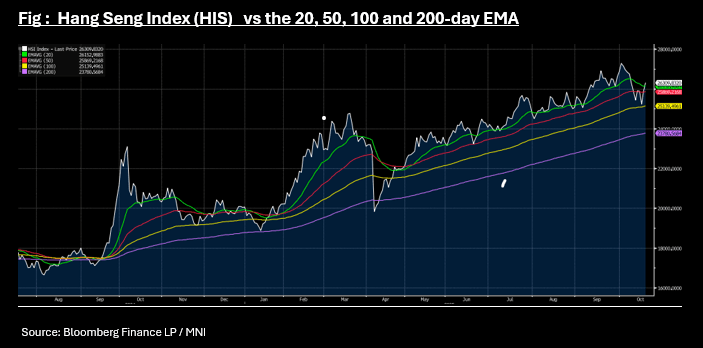

ASIA STOCKS: Trump Comments Drives HSI Above Key Technical

Japanese stocks reached another new high as Sanae Takaichi appears likely to become the next PM and deliver what is expected to be an expansionary fiscal policy and low rates. China's key markets latched onto President Trump's comments that he expects the US and China will have a “really fair and really great trade deal together” with major bourses delivering solid gains. The KOSPI hit yet another new high as the Korea Economic Daily reported that President Lee is considering cutting the top rate on dividends (as per BBG).

- The NIKKEI is up over 700pts today reaching a new high of 49,929 and almost 5% higher in the first two days of the trading week.

- Having trended below the 20-day and 50-day EMA earlier this month, today's gains of +1.8% takes the Hang Seng back above the 20-day EMA of 26,154. The CSI 300 is up +1.5% today for its largest daily gain since before the October National Day holidays. The Shanghai Composite is up +1.20% and the Shenzhen Composite up +1.6% as it nears its 20-day EMA, the second time this month it will try to hold above the key technical.

- The KOSPI is up on the dividend news, trending well above all moving averages and better by +0.6% today, and +2.5% already this week.

- The Jakarta Composite is strong ahead of tomorrow's Central Bank +1.3% as it consolidates above the 20-day EMA.