EU REAL ESTATE: New Immo: 5yr

Nov-06 09:31

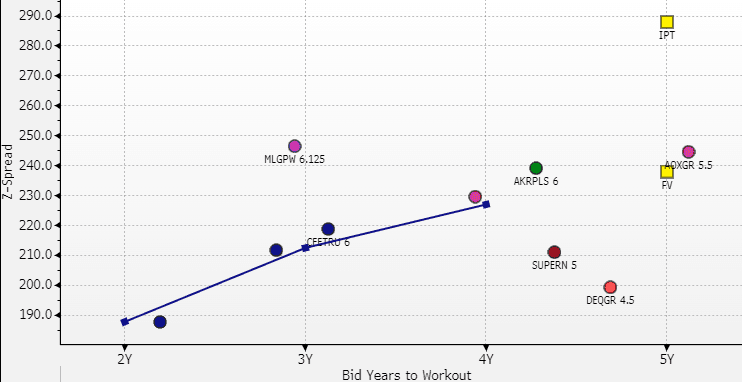

(CEETRU; Ba1/NR/NR)

• IPT: EUR Exp 500m 5yr 5.25-5.375%a (z+288/300)

• We see FV 4.75% z+238

• In terms of retail focus property - should come inside akropolis and outside SuperNova / Deutsche Euroshop. Vs other BB names, just inside Alstria Office.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: EURJPY Pressed Higher Despite Ongoing French Woes

Oct-07 09:26

- The initial fade in the JPY on Monday stalled as advisor Honda talked up governmental support for a December BoJ rate hike, however the currency is on the back foot again early Tuesday, helping usher in new weekly highs for USDJPY at 150.83. The move narrows the gap with key resistance and the bull trigger in the pair at 150.92, clearance above which puts prices at the best level since late March. Takaichi's victory in the LDP leadership race remains the primary driver here, with local press focusing on her negotiations with junior coalition partners - who oppose her more conservative political views.

- EURJPY's rally to new alltime highs this week is largely holding, with Tuesday seeing a 176.35 print, however ongoing fiscal and political concerns in France will be containing the strength. Implied EUR vols are steadying and appear to have halted their multi-month downtrend in the front-end. Calls for early Presidential and legislative elections in France to clear the political logjam have been rising - an unlikely occurrence in the very near-term, but a growing possibility given the government's inability to proceed with an acceptable budget.

- NZD is the poorest performing currency on the day, with AUD not far behind. Price action comes ahead of the RBNZ rate decision on Wednesday, at which markets are split between expecting a 25bps rate cut, or something more sizeable. Consumer confidence data in Australia also deteriorated, dragging AUDUSD toward the weekly lows of 0.6582.

- The ongoing US government shutdown keeps data further delayed, meaning today's trade balance data for August is unlikely to be released (and may have spillover impacts on the Canadian trade balance statistics, which are cross-referenced against the US numbers). As such, the speaker schedule is likely to be of more market importance: Fed's Bostic, Bowman, Miran & Kashkari are all set to appear and may shed some insight into the Fed's views on the shutdown ahead of the Minutes release tomorrow. ECB's Nagel & Lagarde are also on the calendar.

EGBS: German Curve Steepening Resumes; Supply and French Politics In Focus

Oct-07 09:24

The German curve has bear steepened this morning, with yields flat to 2.5bps higher. Although the 5s30s curve has traded in a broadly sideways direction since the September ECB decision, the Sep 12 low of 93.4bps has contained downside and allowed a longer-term steepening theme to remain intact. The curve is back above 100bps at typing (+1.2bps today).

- 10-year yields remain within the familiar 2.60-2.80% range, currently +1.5bps at 2.733%.

- Bund futures are -19 ticks at 128.37 on lighter-than-usual volumes, close to yesterday's 128.31 low. German factory orders were weaker-than-expected this morning, but there’s been more focus on today’s sovereign supply and French political headlines.

- After resigning as French PM yesterday, Lecornu has been invited by President Macron to hold 48 hours of emergency talks to try and gain support for the 2026 budget. Prospects appear bleak, keeping French political/fiscal risks top of mind.

- Germany will sell E4.5bln of the 2.20% Oct-30 Bobl at 1030BST, while today’s RAGB auction saw very strong demand across the two lines on offer. The EU is holding a dual tranche 7/15-year syndication today.

- 10-year EGB spreads to Bunds are mixed, with OATs and BTPs up to 1bp wider on the session.

- The US Government shutdown is ongoing, so no data is due this afternoon. ECB President Lagarde and Bundesbank President Nagel will speak this evening – no changes in stance are expected.

EQUITY OPTIONS: Commerzbank Put Spread

Oct-07 09:23

CBK (19th dec) 36/30ps, bought for 3.52 in 2.5k.