SCANDIS: Near-term Risks In NOKSEK Remain To The Downside

Nov-21 16:10

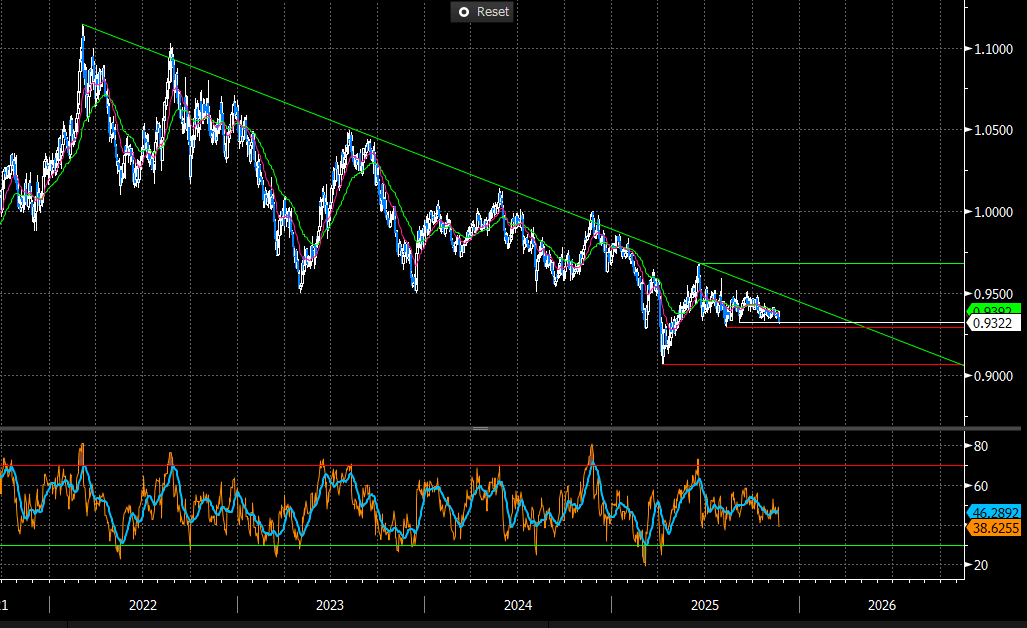

The aforementioned bounce in crude oil futures on the latest Trump comments provides light support to NOK, helping NOKSEK away from session lows of 0.9313. That said, this afternoon’s downside price action has affirmed that the near-term risks in the cross are skewed to the downside. Support at the Sep 5 low of 0.9324 has been pierced, clearance of which would quickly expose clustered support around 0.9295 (Aug 11 low) and 0.9300 (round-number). Beyond this zone, downside targets appear scant until ~0.9200.

- Volatility in NOKSEK has been limited since the middle of October. Early November Norges Bank/Riksbank decisions brought few surprises, with Scandi FX mostly dictated by swings in global risk sentiment.

- SEB have written that “despite a correction lower in NOK/SEK during Q4, there is still scope for the pair to move even lower, according to seasonal trends in Q4. Looking further ahead, the first quarter tends to support the NOK/SEK, hence Q4 presents a buying opportunity for the pair”.

- Next week’s Scandi calendar is headlined by Q3 GDP reports in both Norway and Sweden.

- Consensus sees Norwegian mainland GDP at 0.4% Q/Q (vs 0.6% prior), in line with Norges Bank’s latest projection. Alongside the GDP breakdown, there will be a lot of focus on national account wage metrics. Analyst expectations for Norges Bank’s terminal rate range from 4.00% (i.e. no more cuts) down to 3.25%, so incoming data remains very important to monitor.

- Swedish GDP is seen at 1.1% Q/Q, which would be in line with the flash release presented at the end of October, and well above the Riksbank’s 0.5% September MPR projection. We caution that the flash release can often be heavily revised, but acknowledge that growth data has been improving in recent months. The bar to a near-term Riksbank rate change is high, but we’ve highlighted that the risk of a hike back to 2% exceeds that of another cut on a 12-month horizon.

Figure 1: NOKSEK Since 2022 (Source: Bloomberg Finance L.P)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ITALY AUCTION RESULTS: Day 3 books for the Oct-32 BTP Valore Total E3.3bln

Oct-22 16:01

- Day 3 books for the Oct-32 BTP Valore (ISIN: IT0005672016) totalled E3.3bln. Total books now stand at E13.0bln.

- This will be the fifth BTP Valore issued (but the first of 2025) and have the longest maturity to date. Since launching in 2023, BTP Valore volumes have ranged from E11.2-18.3bln with maturities ranging from 4-6 years.

- The last BTP Valore issued in May 2024 (maturity May 2030) saw day 3 books total E2.1bln, and cumulative books after three days total E8.7bln. Cumulative books for the Feb 2024 Valore issue (maturity March 2030) were E14.7bln

- So far in 2025 there have been two Italian retail offerings: the 9-year BTP Piu in February for E14.9bln and the 7- year BTP Italian in May with a retail takeup of E8.8bln.

- Books for the Oct-32 Valore opened on Monday, and will close at 1300CET on Friday (October 24). The guaranteed minimum coupon rates will be 2.60% for years 1-3, 3.10% for years 4-5 and 4.00% for years 6-7.

SONIA OPTIONS: H6 Call Condor Seller

Oct-22 15:57

SFIH6 96.15/96.25/96.40/96.50 call condor, sold down to 3.25 in 18.5k

EURIBOR OPTIONS: Large Dovish Z6 Call Spread Buyer

Oct-22 15:49

ERZ6 98.875/99.00 call spread, paper pays 0.75 on 17k

Trending Top

Mar-27 20:13