CANADA: Near-Term OIS Steady Whilst BAX Inversion Builds Slightly

Aug-02 18:12

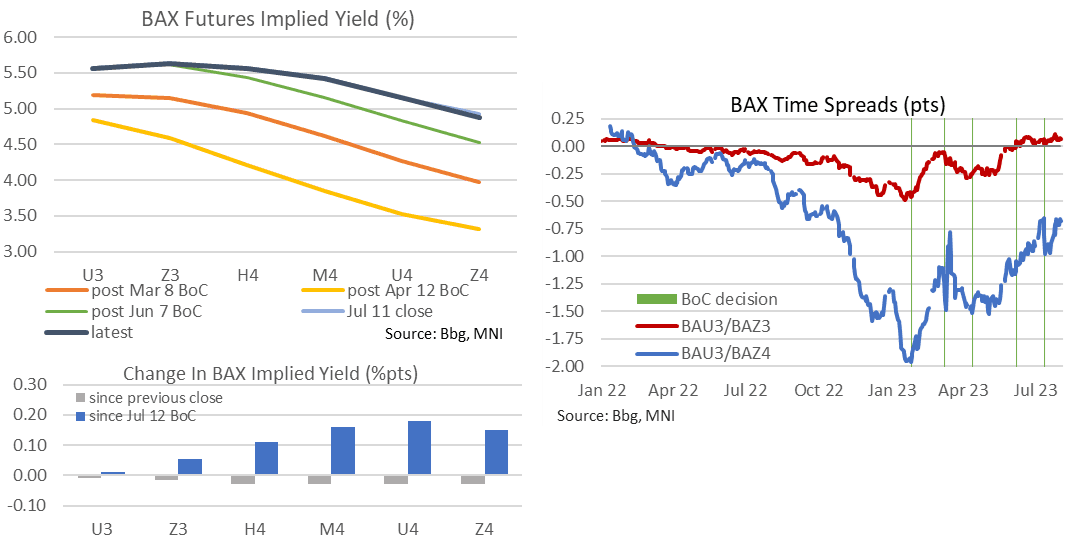

- BAX futures have seen a mixed session but currently hold a push richer on the day as they eat into yesterday’s sell-off.

- The front Sep’23 trades +0.015, building to +0.03 for Mar’24 and +0.04 from Sep’24 onwards, pushing the BAU3/Z4 spread back -68.5bps after yesterday closing at -66bps for its joint lowest since Jul 11 (the day before the BoC decision to hike 25bps to 5%) and before that Oct’22.

- Near-term BoC implied rates hold most of yesterday’s increase meanwhile and in fact push higher for Dec’23, with CORRA OIS showing +9.5bp for Sep building to a cumulative +22bp to year-end.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: Primary Trend Direction Remains Down

Jul-03 18:00

- RES 4: 0.8786 Trendline resistance drawn from the Feb 3 high

- RES 3: 0.8749 50.0% retracement of the Feb 3 - Jun 19 downleg

- RES 2: 0.8719 High May 23

- RES 1: 0.8658 High Jun 28 and a short-term bull trigger

- PRICE: 0.8597 @ 16:06 BST Jul 3

- SUP 1: 0.8576/36 Low Jun 30 / Low Jun 23

- SUP 2: 0.8518 Low Jun 19 and the bear trigger

- SUP 3: 0.8502 1.0% 10-dma envelope

- SUP 4: 0.8454 76.4% retracement of the Mar - Sep 2022 bull cycle

The primary trend direction in EURGBP is down and recent short-term gains are considered corrective. Key near-term resistance has been defined at 0.8658, the Jun 28 high. A break of this level would resume the recent uptrend and signal scope for a climb towards 0.8719, the May 23 high. On the downside, a deeper pullback would instead expose the bear trigger at 0.8518, where a break would confirm a resumption of the downtrend.

US TSY FUTURES: BLOCK, Late Sep'23 2Y Buy

Jul-03 17:45

- +5,000 TUU3 101-18.25, buy through 101-18 post-time offer at 1327:29ET

US TSYS: Rates Back Near Lows Despite Weaker ISMs

Jul-03 17:43

- Treasury futures finishing the shortened pre-holiday session at/near lows, accounts scaling back support despite early session data showed disinflationary signs.

- Treasury futures extend highs slightly after S&P Global US Manufacturing PMI comes out as expected at 46.3, not a large reaction.

- Treasury futures extended highs after June ISM Manufacturing falls to 46.0 vs. 46.9 est (47.2 prior) the lowest since May 2020. Prices paid at 41.8 lower than exp 44.2, ISM Employment at 48.1 lower than expected 51.4. Meanwhile, Construction Spending MoM lower than expected at +0.9% vs. 1.2% est.

- Front month 10Y futures marked 112-17.5 high (+9) before falling back to111-29.5 after the early close. Initial technical resistance at 112-21 Jun 22 low, 113-18 June 15 High key resistance.

- Later in the week, FOMC minutes for the June meeting are released at 1400ET Wednesday, while the latest employment data is released this Friday at 0830ET, current mean est at 225k vs. 339k prior.