FED: NatWest Now Sees Cuts In 2025, Starting In September

As with Deutsche earlier, NatWest has changed its Fed call after the Powell Jackson Hole speech to reflect a 25bp September cut. Previously, the call was for no cuts in 2025. The new baseline outlook includes further 25bp cuts in December and March, bringing rates closer to neutral ("however, the changing composition of the committee becomes far less clear once Powell term expires in May").

- "While the August jobs and CPI reports will be watched carefully, it is clear to us that Powell has already seen enough to decide renewed action to counter downside economic risks is likely warranted, and so we now look for a 25 basis point rate cut on September 17th.

- "We expect officials will very much downplay the likelihood of a 50bp rate cut leading up to the jobs data, but we have to admit if the report is "weak enough" (e.g., the unemployment rate increases by 0.3pct to 4.5% (where officials had it at year end) anything can happen and wouldn't rule anything out. However, given the latest pivot and with financial markets pricing (86% of a 25bp rate cut) a lot has to happen (unemployment rate 3-handle and core CPI +0.5%) for the FOMC to undeliver and hold off from a rate cut in September. "

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

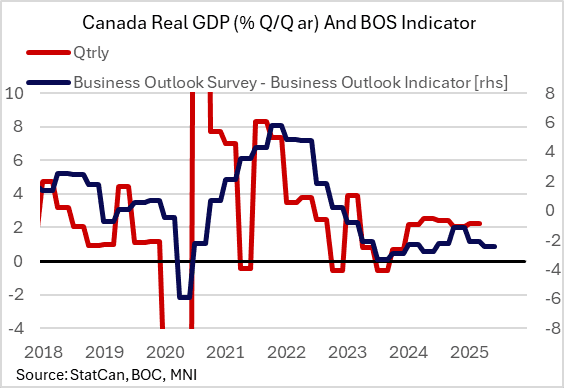

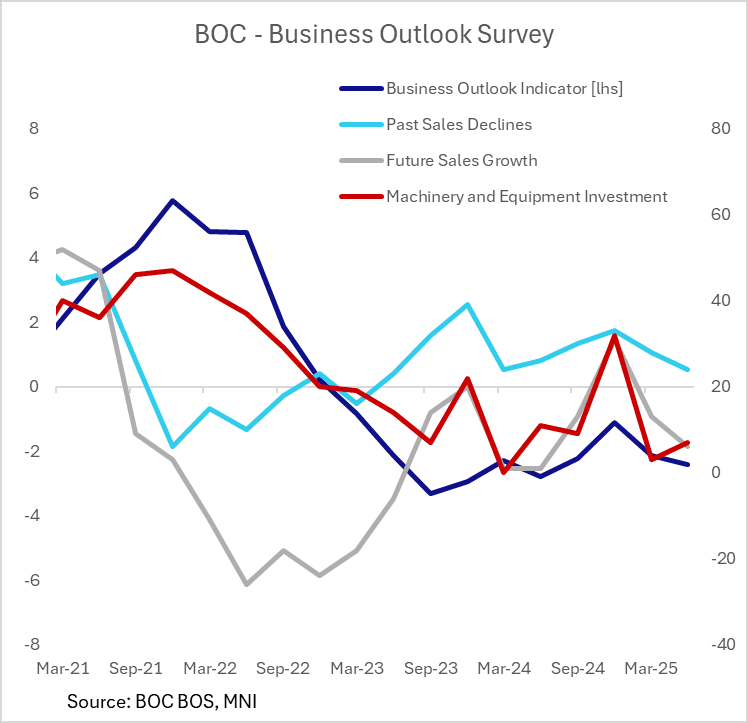

CANADA: BOC Business Outlook Survey Roughly Neutral For Rate Path (1/3)

The Bank of Canada's quarterly Business Outlook Survey (BOS) and Canadian Survey of Consumer Expectations (CSCE) showed broadly that the economy and inflation expectations stabilized between February (the Q1 survey) and May (the Q2 report released this month).

- Neither survey's findings are an obstacle for further BOC rate cuts, but nor do they make a compelling case for further easing (although the consumer survey was clearly the weaker of the two).

- Additionally, there is something of a staleness about the Q2 survey, whose responses were collected before US Pres Trump raised his tariff threat to 35% while pushing back his deadline to Aug. 1. As such there was only limited market reaction to the Q2 release on July 21.

- In the BOS, the 0.3 point drop in the Business Outlook Indicator (-2.42) in Q2 brought the level to the lowest since Q4 2023 but was a stabilization of sorts compare to the 1 point drop between Q4 2024 and Q1 2025 (which was the largest since early 2023 albeit that was from a much higher starting level). Past and future sales dropped to the lowest level since Q1 2024, with indicators of future sales at -6, the lowest since Q4 2023.

- 28% of business owners expect a recession in the next 12 months.

- Even so, machinery investment intentions and future employment actually picked up slightly.

- From the report: "Tariffs and related uncertainty, along with spillover effects on the Canadian and global economies, continue to have major impacts on businesses’ outlooks. However, the worst-case scenarios that firms envisioned last quarter are now seen as less likely to occur. Sales outlooks remain pessimistic overall due to widespread concerns about the broader effects of a slowing economy. But recent monthly survey results suggest some improvement in firms’ outlooks—particularly among exporters—because few have been directly affected by the current tariffs. Uncertainty continues to drive cautiousness in outlooks for hiring and investment. Most firms expect to maintain current staffing levels and limit investment to regular maintenance over the next 12 months."

USDCAD TECHS: Bears Remain In The Driver's Seat

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3738/74 50-day EMA / High Jul 17

- PRICE: 1.3617 @ 16:13 BST Jul 23

- SUP 1: 1.3557 Low Jul 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

The trend needle in USDCAD continues to point south and this week’s move down reinforces current bearish conditions. Resistance at 1.3738, the 50-day EMA, remains intact for now. A clear break of it is required to highlight a possible stronger short-term reversal. For bears, a continuation lower open key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the downtrend.

FED: Inter-Meeting FedSpeak: Uncertainty Equals Patience For Most (2/2)

While a majority of participants appear open-minded to the argument that tariff inflation will prove transitory and that the labor market is “on the edge” (in Waller’s words), almost all participants require more certainty in the data and broader developments before supporting a cut.

- “Uncertainty” was cited by many as a key reason to maintain a patient stance. For example, SF’s Daly is concerned that the Fed could fall behind the easing curve but still only eyes two cuts this year, and not before the fall.

- The most hawkish Board member – Gov Kugler (who is very likely to be replaced in January at the end of her term) – saw the June inflation reports pointing to tariff pressures beginning to show up in prices. Another 2025 voter, St Louis’s Musalem, saw the possibility it could be several months if not quarters before tariffs’ full impact would be felt.

- We haven't heard any other FOMC participants say they were seriously considering supporting a cut at the next meeting, with various members that see two cuts this year eyeing a later restart to easing (Daly / Kashkari specifically mentioned the fall/September respectively).

- In other communications, the latest Beige Book suggested that regional business contacts saw the biggest price increases from inflation are yet to come.

- The June meeting minutes noted "several participants commented that the current target range for the federal funds rate may not be far above its neutral level", pointing to an increasing number of participants that suspect the terminal rate may be higher than previously expected.