FED: NatWest, Nomura, BMO, Rabo, Swedbank Tweak Fed Views (2/3)

Sep-18 15:57

The following analysts revised their Fed calls after the September meeting:

- NatWest: Pulling forward a cut to Q4 2025 from Q1 2026, and adding 75bp of cuts beginning in June: Their new view sees "a quicker steady stream of consecutive 25bp rate cuts", with 25bp in Oct and 25bp in Dec (previously only saw 25bp cuts in Dec and Mar). "We are also folding in an additional 75bps of easing post-Powell into our forecast profile, as we are growing increasingly concerned about potential slowing in the labor market along with the likelihood of a more dovish leaning FOMC composition once a new Fed chair takes over."

- Nomura: Adding 3 cuts to their expected rate path: "We have revised our forecast and now expect two additional cuts this year (we had previously forecast a pause in October and a cut in December). Less emphasis on inflation risks and a likely shift in Fed leadership next year leads us to forecast three additional cuts in 2026 in March, June, and September. We had previously expected the easing cycle to end after March....our updated expectation the terminal rate is 2.875%, down from 3.625% prior to today."

- BMO: Adding an October cut: "With policy rates still 100-to-125 bps above the neutral level and the deterioration in labour market conditions expected to persist through at least the turn of the year, we reckon the ‘dot plot’ is a decent road map for the remainder of this year. We now look for two more quarter point rate cuts this year (October-end and mid-December), compared to only one more action previously. Afterward, as before, we expect the rate cut cadence to slow (to once per quarter), lowering the fed funds range to 2.75%-to-3.00% (just a tad below neutral). We’re just getting there a little more quickly as the Fed looks past still sticky inflation with an eye on the labour market."

- Rabobank: Adding an October cut: "Powell’s dovish tone and shift in the mandate towards labor suggests that we may see more frontloading of cuts than originally anticipated (though certainly not the 100bp by year-end proposed by a certain anonymous member of the board). We now forecast another 25bp cut at the October 29 meeting, and still see a terminal Fed Funds rate of 3.00%. The risk to our view is skewed to two more cuts this year over none, due to the rapidly deteriorating state of the U.S. labor market."

- Swedbank: Adding an October cut: "Given Fed’s messaging today, we change our call and now expect the Fed to cut interest rates by 25 bps both in October and December (previously we forecasted a cut only in December). We keep our forecast for the terminal rate next year unchanged, however."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (U5) Monitoring Support

Aug-19 15:56

- RES 4: 113-23 76.4% retracement of the Sep’24 - Jan’25 sell-off

- RES 3: 113-07 76.4% retracement of the Apr 7 - 11 sell-off

- RES 2: 112-23 High May 1

- RES 1: 112-15+ High Aug 5

- PRICE: 111-23 @ 16:51 BST Aug 19

- SUP 1: 111-10+ 50-day EMA

- SUP 2: 110-23+/08+ Low Aug 1 / Low Jul 15 & 16

- SUP 3: 110-03 76.4% retracement of the May 22 - Jul 1 bull leg

- SUP 4: 109-28 Low Jun 6 and 11

The underlying bullish theme in Treasury futures remains intact, supported by the recent clearance of 112-12+, the Jul 1 high. Short-term weakness is considered corrective. A resumption of gains would open 112-23, the May 1 high and the next important resistance. Above 112-23, retracement levels are layered between 113-07 and 113-23. Key support is 110-08+, the low on Jul 15 and 16. First key support is yet to be tested at 110-23+, the Aug 1 low.

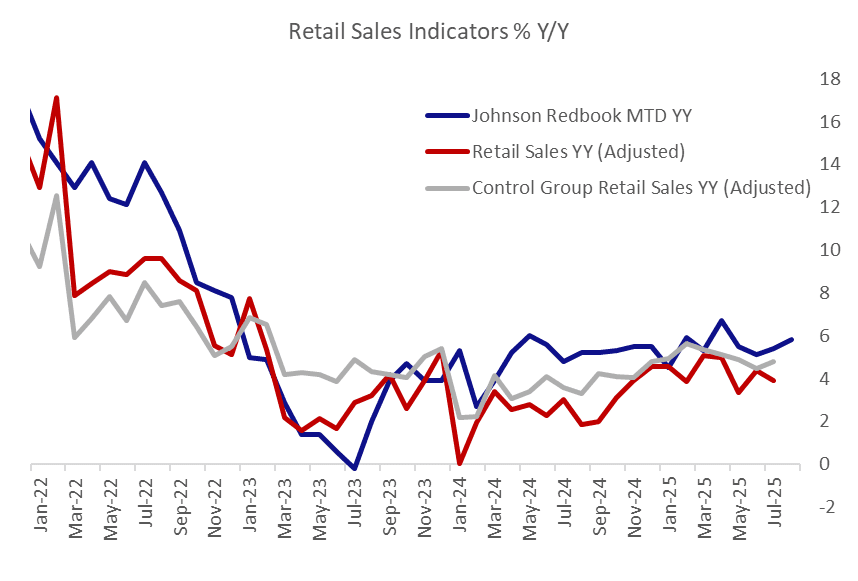

US DATA: Redbook Retail Sales Remain Solid Through Mid-August

Aug-19 15:38

Retail sales as measured by the Johnson Redbook index rose 5.9% Y/Y in the week ending August 16, up from 5.7% the prior week and bringing the month-to-date rise to 5.8%.

- That's very solid outright, albeit somewhat below retailers' targeted 6.2% gain. Per the report's anecdotes: "Early back-to-school sales results have generally fallen short of expectations. Some markets, particularly in the Midwest and Southeast, have already begun their back-to-school season, while others have not yet started. Additionally, the tail-end of state tax-free holidays in Florida, Maryland, Massachusetts, Ohio, and Texas has contributed to increased traffic and sales. Due to regional differences in school calendars and variations in merchandising schedules, the rollout of new seasonal programs has varied from store to store; it is still too early to gauge consumer reactions to these programs. Many major retailers are set to report their second-quarter earnings this week and next week, which may provide insights into how tariffs are affecting value-conscious consumers and consumer spending overall."

- On a Y/Y basis, Census Bureau retail sales came in at 3.9% overall in July, down from 4.4% prior, though control group sales picked up to 4.8% from 4.5%. While the Johnson Redbook has tended to "over-estimate" Census Bureau sales on this basis, sustained growth continues to suggest solid consumption dynamics through the middle of Q3 (with the usual caveat that these are in nominal and not price-adjusted terms).

OPTIONS: Larger FX Option Pipeline

Aug-19 15:35

- EUR/USD: Aug21 $1.1600(E1.3bln), $1.1700(E1.6bln), $1.1750(E2.0bln), $1.1800(E3.0bln); Aug25 $1.1640-55(E2.0bln)

- USD/JPY: Aug21 Y145.95-00($1.2bln), Y146.70-80($1.8bln); Aug22 Y147.90($1.4bln)

- AUD/USD: Aug21 $0.6590-00(A$1.8bln); Aug25 $0.6510-25(A$1.1bln)