EGBS: Natixis Recommend Short End SPGB Vs. BTP Tightener

Natixis note that “Spanish short-end yields cheapened too much into year end. We see this cheapening as liquidity-driven and not warranted by fundamentals and technical factors for Spain.” As such, they recommended a long position in Bono 10/2025 vs. BTP 11/2025 at -14.9bp, with a take-profit -35bp over a 3-month horizon. They set a stop loss -4.85bps.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Resistance At The 50-Day EMA Remains Intact

- RES 4: 1.3855/3899 High Nov 10 / 1 and the bull trigger

- RES 3: 1.3777 High Nov 16

- RES 2: 1.3712 High Nov 24

- RES 1: 1.3648 50-day EMA

- PRICE: 1.3593 @ 16:28 GMT Dec 8

- SUP 1: 1.3480 Low Dec 4

- SUP 2: 11.3417 Low Sep 29

- SUP 3: 1.3401 61.8% retracement of the Jul 14 - Nov 1 bull phase

- SUP 4: 1.3381 Low Sep 19 and a key support

USDCAD maintains a softer tone following and the latest recovery appears to be a correction. The recent break of trendline support, drawn from the Jul 14 low, strengthens the current downtrend and signals scope for a continuation lower near-term. Sights are on 1.3417 next, the Sep 29 low. Initial firm resistance is at 1.3646, the 50-day EMA. A breach of this hurdle is required to ease the current bearish pressure.

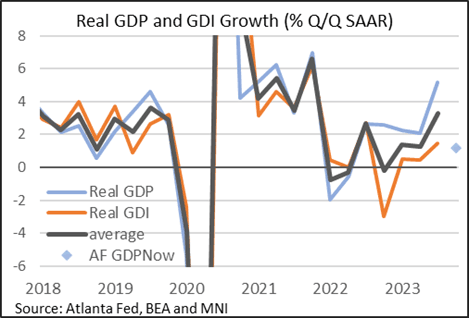

US OUTLOOK/OPINION: Macro Developments Since Nov FOMC - Growth: Booming Q3 Before Fading

- The stellar GDP growth from Q3 has not only been confirmed but was surprisingly revised even higher to 5.2% annualized from an initial 4.9%.

- Some details within it were softer though, including a surprise downward revision to personal consumption.

- The story from the advance release was domestic demand strength landing alongside a strong bounce in changes in inventories. That still stands although the domestic demand strength is now seen as less driven by private consumption than first thought, with government consumption revised higher but also encouragingly non-residential fixed investment.

- An alternate accounting approach in Gross Domestic Income (GDI) meanwhile continues to paint a far more subdued picture.

- Taken together, the average saw real economic growth accelerate to 3.3% in Q3 after an average 1.3% in 1H23.

- Data since Q3 have on balance come in softer than initial tracking suggesting, with the Atlanta Fed’s GDPNow currently pointing to real GDP growth of 1.2% annualized in Q4. A lot of this is a swing back to a negative contribution for changes in net inventories, implying relatively limited payback for final domestic demand after a very strong Q3.

US TSYS: Markets Roundup: Surprise Jobs Gain Tempered by Down-Revisions

- Tsy futures gap lower after slightly stronger than expected Change in Nonfarm Payrolls (+199k vs. 183k est, +150k prior), Change in Private Payrolls softer (+150k vs.158k est, 99k prior), Unemployment Rate dips to 3.7% vs. 3.9% est.

- Futures quickly scaled back appr half the initial post-data sell-off as markets digested the down-revisions to prior and unrounded releases.

- U.S. employers added more jobs than expected in November and average hourly earnings growth was also hotter than expected, which could add to the Federal Reserve's resolve to keep rates higher for longer to cool the labor market and rein in inflation. Projected rate cut for March 2024 consolidated from -55.2% pre-data to -44.5% by the close, May 2024 down to -63.5% vs. -70.1% pre-data.

- Average hourly earnings added 0.4% in November, a tenth higher than expected and marking a gain of 4.0% over the past 12 months. The employment-to-population rate rose 0.3 percentage point as the labor force continued to expand.

- Tsys held off lows following higher than expected U. of Mich. Expectations that climbed to 66.4 vs. 57.0 est, (56.8 prior), Sentiment 69.4 vs. 62.0 est, while 1 Yr Inflation est fell to 3.1% vs. 4.3% est (4.5% prior), 5-10 Yr Inflation 2.8% vs. 3.1% est (3.2% prior).

- All relevant ahead of next Wednesday's FOMC policy announcement while markets get to see final CPI and PPI inflationary figures on Tuesday and Wednesday respectively.