LATAM: National Leaders & Finance Ministers Set To Speak At CAF Forum

The International Economic Forum of Latin America & the Caribbean gets underway later today in Panam...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: Monday Data Calendar: Pending Home Sales, Dallas Fed Mfg Activity

- US Data/Speaker Calendar (prior, estimate). All times ET

- 12/29 1000 Pending Home Sales MoM (1.9%, 1.0%), YoY (-0.4%, 0.1%)

- 12/29 1030 Dallas Fed Mfg Activity (-10.4, -6.0)

- 12/29 1130 US Tsy $86B 13W & $77B 26W bill auctions

- Source: Bloomberg Finance L.P. / MNI

BONDS: Off Highs As Oil Trims Friday's Losses & Early Bid Stalls

Core global FI markets have firmed after Europe & the UK returned from the Christmas break.

- Oil is lower vs. pre-Christmas levels, but comfortably off Friday lows.

- Geopolitical headlines have provided much of the focus, with U.S. strikes on an ISIS target in Nigeria, the ongoing blockade of Venezuelan oil and Russia-Ukraine matters front and centre.

- The latest round of U.S.-Ukraine & U.S.-Russia talks seemingly yielded positive results, albeit with some sticking points still noted. Ukrainian President Zelensky suggested that the weekend talks are "90%" of the way to a deal.

- Bunds have breached first resistance, although bulls have been unable to test the 20-day EMA (127.87), with the rally topping out at 127.77. A break above that average would pose a deeper threat to the bearish technical theme. Meanwhile, first support located at 126.75.

- Yields ~1bp lower across the German curve, early flattening theme moderates.

- EGB spreads to Bunds flat to 1bp tighter, even as global equity benchmarks edge lower.

- EUR short end pricing ~4.5bp of tightening for ’26.

- Gilt futures trade as high as 91.39, through initial resistance at 91.18. Next upside level of note 91.78. Conversely, initial support is located at 90.50.

- UK yields 1.0-2.5bp lower, curve flatter. 10s back below 4.50%, oscillating around that level since early December.

- Gilt/Bunds stable around 164bp after the recent failed foray below 160bp.

- GBP STIRs a little more dovish on the day given cues from further out the curve. Next 25bp BoE rate cut fully discounted through June, ~39bp of easing priced through November.

- No tier 1 risk events on the G20 calendar today.

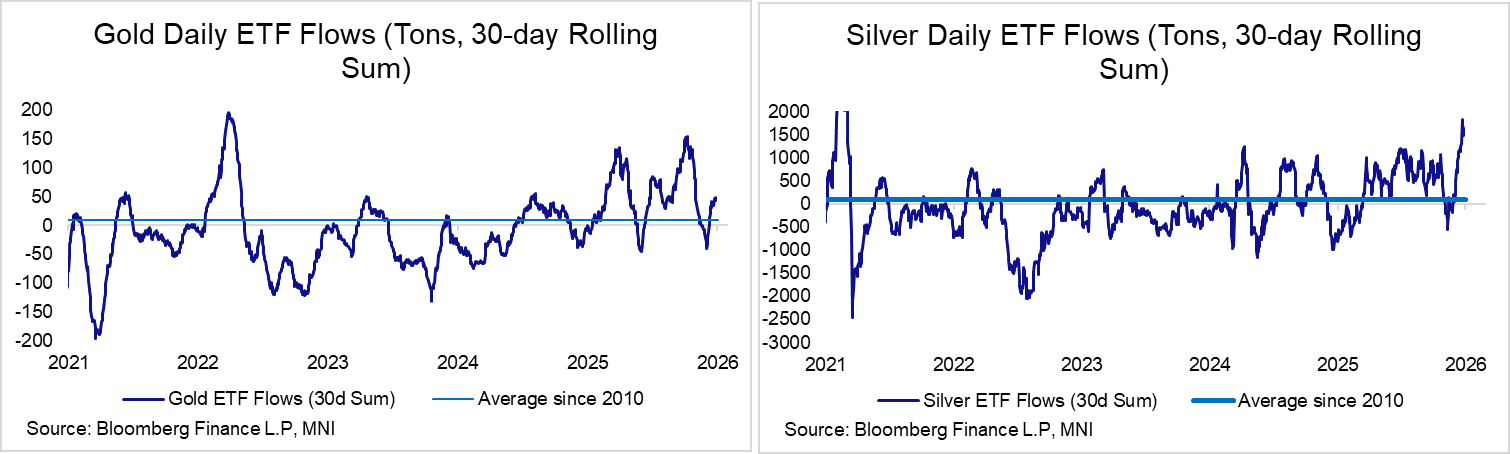

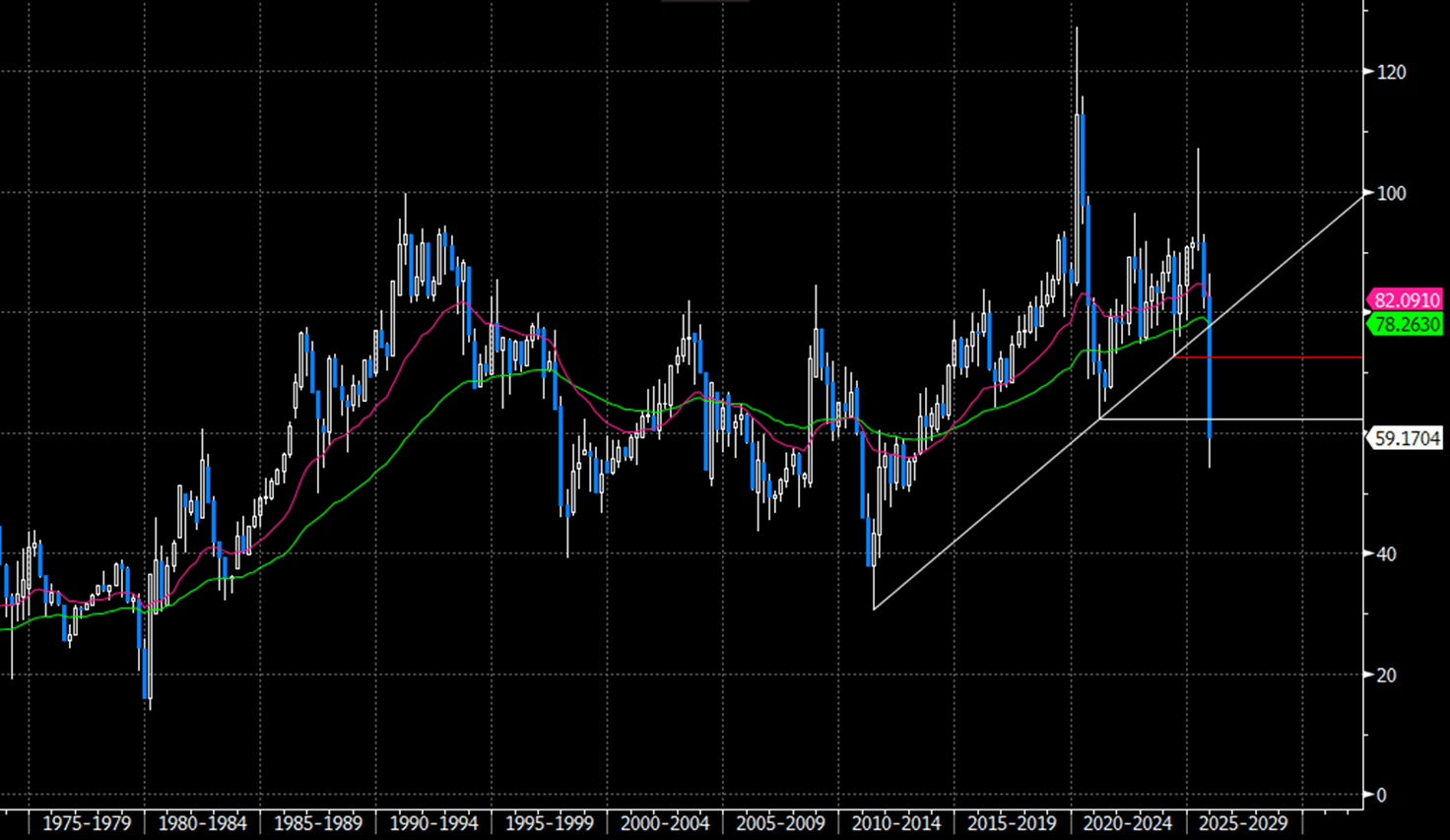

PRECIOUS METALS: Gold/Silver Ratio Off Multi-year Lows; ETF Inflows Have Surged

Today’s near-5% pullback in silver helps the gold/silver ratio back to ~59, off 12-year lows of 54 registered overnight. Thinner trading conditions over the Christmas-New Year period will be contributing to price swings intraday, with more focus on how the metals complex fares in January when the bulk of market participants return to their desks. Some have cited profit taking/tax selling as a bearish risk to monitor in the coming weeks.

- The chart below highlights the surge in silver ETF inflows through December, including a 533-tonne inflow on December 23. Several narratives have been touted as drivers of the recent rally (e.g London physical market stress, Chinese export restrictions, industrial supply-demand imbalances and ongoing geopolitical tensions), incentivising participation from retail accounts.

- Gold ETF inflows have also increased in recent weeks, but to a much lesser extent relative to historical averages.

Figure 1: Gold/Silver Ratio Quarterly Chart (Source: Bloomberg Finance L.P)

Figure 2: Gold and Silver ETF Inflows