NATGAS: Natural Gas End of Day Summary: Henry Hub Rallies

Henry Hub is continuing today’s rally and is ticking up around 0.4% on the week, amid thin holiday trading volumes and cooler weather and high LNG feedgas flows.

- US Natgas JAN 25 up 4.6% at 3.35$/mmbtu

- US Natgas JUN 25 up 2.4% at 3.16$/mmbtu

- Lower 48 natural gas demand has risen to the highest since February at 96.3bcf/d today, according to Bloomberg driven by current below normal Lower 48 temperatures.

- The previous five-year average is around 87.5bcf.d. Cold weather into early next week could ease with the NOAA 6-14 day forecast showing above normal in the west spreading into central areas but with below normal temperatures still on the East Coast.

- US LNG export terminal feedgas supply is estimated at the highest since January at 14.1bcf/d today, BNEF shows, with a further rise in Freeport and Sabine Pass supplies.

- US domestic natural gas production remains strong at 104.5cf/d today, according to Bloomberg, to hold near the highest since early August.

- Export flows to Mexico are estimated at 6.24bcf/d today, according to Bloomberg.

- Venture Global is set to start producing LNG from the Plaquemines LNG facility in Louisiana within days, according to the FT cited by Bloomberg.

- Changes in gas spreads between Asia and Europe have resulted in multiple LNG vessel divisions this month with more seen this week. The has become the preferred destination for diverted LNG cargoes due to slot availability vs NWE ports according to Platts vessel tracking.

- Asia’s spot LNG prices rose for a third consecutive week to reach new year-to-date highs, with colder weather driving up demand, Reuters said.

- Israeli gas output hit a record of 2.86 bcf in Q3 (7.46 bcm), with the final figure higher than provisional estimates, MEES said.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SECURITY: US Has 'Conversations' W/Israel About Ceasefire In Lebanon, State Dept

US State Department Spokesperson Matthew Miller has told reporters that the US, "has ongoing conversations with Israel about what a diplomatic resolution in Lebanon can and should look like."

- Miller noted that the US, "supports Israel's right to go after legitimate Hezbollah targets in Lebanon," but stressed that, "it's critical that Israel does so in a way that doesn't threaten the lives of civilians, and significant cultural heritage sites are protected."

- Miller adds that the Israeli military has made, "significant progress in striking Hezbollah sites along the border and clearing out its infrastructure," and notes that the conflict should be resolved, "through a diplomatic resolution well short of a prolonged campaign like in Gaza."

- The comments come after Hezbollah chief Naim Qassem today appeared to open to ceasefire talks with Israel. See: MIDEAST: Hezbollah Chief Leaves Door To Israel Ceasefire Ajar

PIPELINE: $7.25B Marsh McClennan 7Pt, $3B Philip Morris Debt Launched

In line with top end of earlier estimates, Marsh McClennan launched $7.25B in debt over 7-tranches. Waste Management 5pt guidance updated.

- Date $MM Issuer (Priced *, Launch #)

- 10/30 $7.25B #Marsh McLennan $950M 3Y +45, $300M 3Y SOFR+70, $1B +5Y +55, $1B 7Y +65, $2B +10Y +75, $500M 20Y +75, $1.5B +30Y +95

- 10/30 $3B #Philip Morris $750M 3Y +50, $750M 5Y +65, $750M 7Y +80, $750M 10Y +92

- 10/30 $Benchmark Waste Management +3Y +45, +5Y +55, +7Y +65, +10Y +75, 30Y +87.5

- 10/30 $3B #Philip Morris $750M 3Y +50, $750M 5Y +65, $750M 7Y +80, $750M 10Y +92

- 10/30 $500M *CenterPoint Energy WNG +10Y +83

- 10/30 $Benchmark Marex Group5Y +225a

- 10/30 $1B *Kingdom of Belgium WNG 10Y +64

- 10/30 $500M *Swedish Export Credit 2.5Y SOFR+35

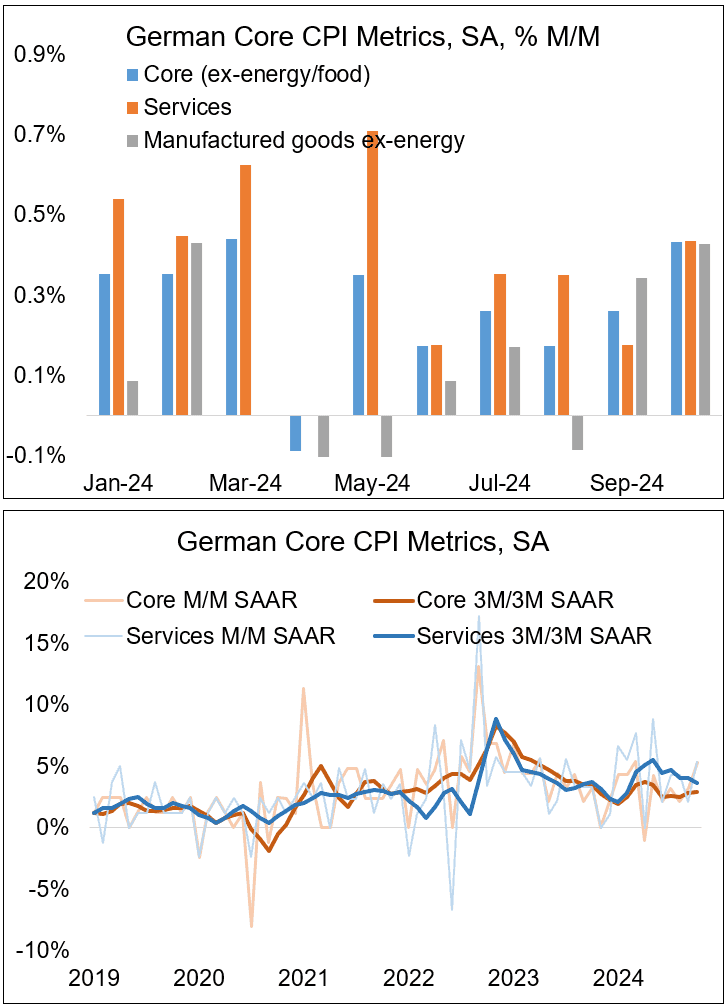

EUROPEAN INFLATION: BUBA Confirms Firmer SA Core Estimates For October

The Bundesbank’s estimate of seasonally-adjusted German CPI suggests sequential core inflation momentum accelerated significantly in October, as projected by MNI. This was driven by both services and core goods running firmer than in September - and also clearly elevated on a YTD comparison.

- Overall core inflation increased to 0.43% M/M SA (vs 0.36% MNI estimate; 0.26% in Sep, 5.3% annualized) on a seasonally adjusted basis per Buba, with services inflation at 0.44% M/M (vs 0.43% MNI estimate; 0.17% in Sep, 5.4% annualized).

- Manufactured goods ex-energy meanwhile also accelerated, to 0.43% M/M, its joint highest rate since March 2023 (vs 0.34% in Sep, 5.2% annualized, no MNI estimate).

- 3M/3M measures were a bit mixed: core 0.73% vs 0.70% prior, services 0.91% vs 1.0% prior (a base effect was behind the small dip), and manufactured goods ex-energy was 0.43% vs 0.23% prior.

- Overall, the October German inflation round clearly underscored the narrative of ongoing stickiness.