US TSYS: Narrow Ranges In Holiday-Thinned Overnight Trade, ISM Mfg Ahead

May-01 10:54

Treasuries are mildly lower overnight but have kept to very narrow ranges throughout with much of Eu...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Off Highs But Recent Firmer Trend Holds Ahead Of Notable Data Docket

Apr-01 10:54

Treasuries have given back some earlier gains with Iranian comments about not opening the Strait of Hormuz although still sit firmer on the day against a backdrop of broader de-escalation hopes seen in recent days. Geopolitical headlines will remain in focus with a build-up to President Trump giving “an important update on Iran” after the close at 2100ET. In the interim there are notable data releases with ADP, retail sales and ISM manufacturing plus scope for hawkish Fedspeak.

- Cash yields are 3-4bp lower on the day across the curve.

- 10Y yields earlier came close to testing a sub-4.25% handle for the first time since Mar 19 (low 4.2574%, currently 4.279%).

- TYM6 trades at 111-10 (+08+) off an earlier high of 111-14+ on elevated cumulative volumes of 540k.

- It sees an extension of a corrective bounce that has firmed with a piercing of resistance at 111-10 (20-day EMA) to open a more important 111-26+ (50-day EMA). The bear trigger meanwhile is seen at 109-24 (Mar 27 low) with a break resuming a downtrend.

- Data: Weekly MBA (0700ET), Monthly ADP Mar (0815ET), Retail sales Feb (0830ET), S&P Global US PMI mfg Mar final (0945ET), ISM mfg Mar (1000ET), Business inventories (1000ET)

- Fedspeak: Musalem on economy (0905ET), Barr on AI/consumer issues (0910ET) – see STIR bullet

- Bill issuance: US Tsy $69B 17W bill auction (1130ET)

- Politics: Trump attends Supreme court oral arguments on birthright citizenship (1000ET), Trump in Easter lunch (1230ET), Trump speech including “an important update on Iran” (2100ET)

- Recent Iran-related headlines: Trump said he foresaw ending the war on Iran within 2-3 weeks, suggesting the US had largely accomplished its military goals and would leave it to other nations to resolve issues with the Strait of Hormuz. Against that, Iran’s Fars News reports hardline conservative Deputy Speaker Ali Nikzad says that "We will not let go of Trump's collar […] The Strait of Hormuz will not open, we have not held negotiations, and we will not hold them."

- Trump also told the Telegraph he is strongly considering pulling the US out of NATO.

OUTLOOK: Price Signal Summary - Corrective Cycle In S&P E-Minis

Apr-01 10:43

- In the equity space, a strong rally in S&P E-Minis yesterday highlights the start of a corrective phase. Note that a correction is allowing an oversold trend condition to unwind. Initial firm resistance to watch is 6660.09, the 20-day EMA. A clear break of this average would signal potential for an extension towards 6793.69, the 50-day EMA and a key area of resistance. The bear trigger has been defined at 6753.25, the Mar 31 low.

- The trend condition in EUROSTOXX 50 futures remains bearish and - for now - short-term gains are considered corrective. Note that the trend has been in oversold territory recently and a stronger recovery would allow this set-up to unwind. Key pivot resistance is seen at 5729.44, the 50-day EMA, where a clear break is required to signal a possible reversal. For bears, a resumption of weakness would open 5277.64 next, a 1.382 projection of the Mar 5 - 9 - 10 price swing.

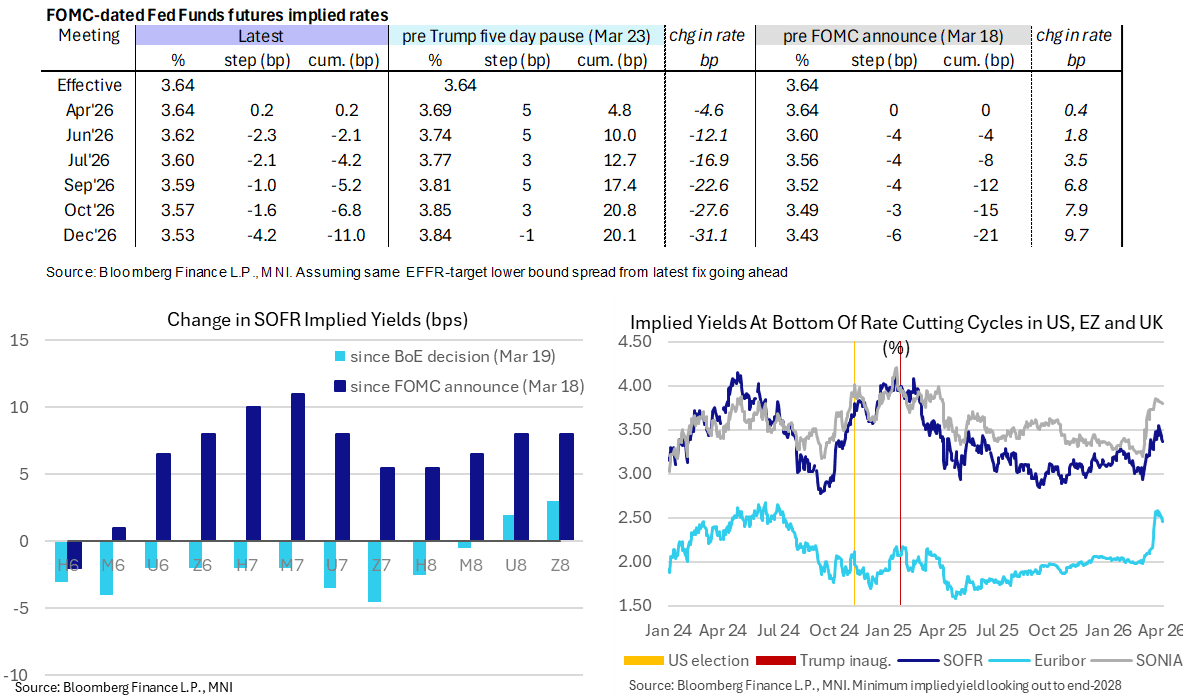

STIR: US Rates Extend Tuesday Gains On Mid-East De-Escalation Hopes

Apr-01 10:36

- US rates on balance extend yesterday’s gains on hopes of de-escalation in the Middle East conflict, although were helped off highs by Iranian comments saying the Strait of Hormuz “will never re-open” (caveated by the Iran’s parliament having already approved a bill to charge for transit).

- FF cumulative cuts from 3.64% effective: 0bp Apr, 2bp Jun, 4bp Jul, 5.5bp Sep, 7bp Oct and 11bp Dec.

- SOFR futures are currently up to 6 ticks firmer in the H7 as they continue to reverse heavy losses concentrated in that section of the strip earlier in the conflict.

- The SOFR terminal implied yield of 3.365% (Z7, -4bp) last closed lower Mar 18 and compares with the March range of 3.075% (Mar 2) to 3.55% (Mar 26) for closes.

- Today sees notable data releases including ADP employment for March, retail sales for February and ISM manufacturing for March.

- That’s along with the first post-FOMC comments from St Louis Fed’s Musalem (non-voter, hawk) on the economy and mon pol (0905ET, text + Q&A). We assume he was one of seven who pencilled in no rate cuts this year in the March SEP.

- He’s followed shortly after by another appearance from Gov. Barr (voter), this time on AI and consumer issues (0910ET, Q&A only).