NEW ZEALAND: Moody's Revises NZ Outlook To Negative, Rating Affirmed At Aaa

Apr-22 09:28

Moody's has revised New Zealand's outlook to negative from stable, while affirming its Aaa rating. T...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: 0QM6 96.25/96.125 Put Spread Blocked

Mar-23 09:21

{US} SOFR OPTIONS: Latest block trade lodged at 09:06:21 London/05:06:21 NY:

- 0QM6 96.25/96.125 put spread 4.6K lots blocked at 5.0, looks like a buyer.

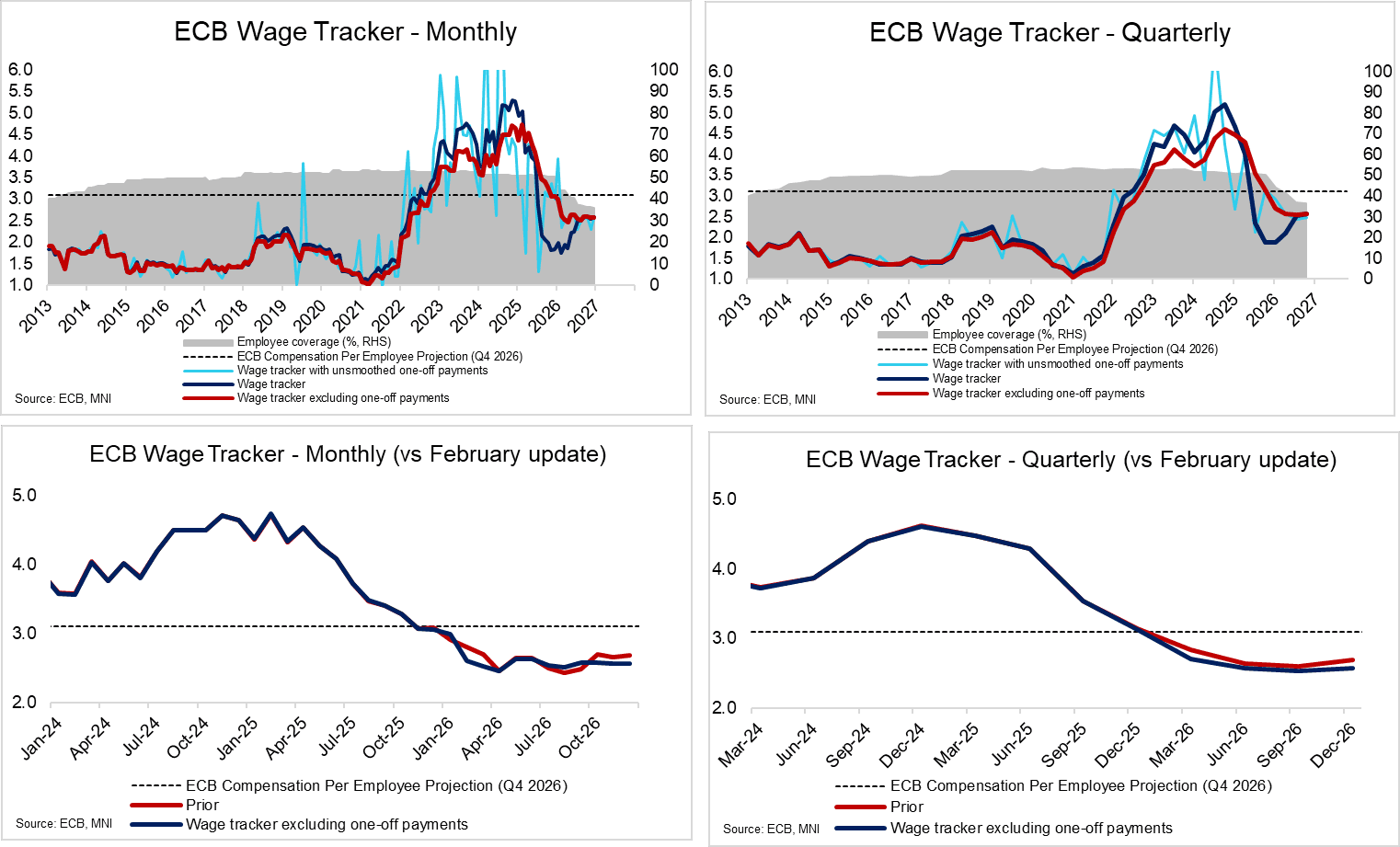

ECB: Wage Tracker Sees Downward Revision vs Feb, Key Focus In Months Ahead

Mar-23 09:16

The ECB’s forward looking wage tracker pointed to negotiated wages excluding one-off payments at 2.575% in Q4 2026, down from 2.693% in the February update. Employee coverage for Q4 2026 rose to 36.3% from 28.5% prior. Wage tracker updates have historically seen upward revisions over time, so this goes against that recent trend. It’s too soon for any Iran-war impacts to be reflected in negotiated wages, but this will be a focus point for the ECB in the months ahead.

- A reminder that negotiated wages are only one subset of total employee compensation. The second non-negotiated wages component is what surprised the ECB’s projection to the upside in Q3 2025 (though Q4 2025 did see a downward surprise).

- The ECB upgraded its Q4 2026 compensation per employee projection up to 3.1% in March, from 2.9% in December.

- In the ECB’s “adverse” alternative scenario for the Iran war, compensation per employee rises to 3.7% in Q4 2026. In the “severe” scenario, compensation is seen at 4.6%.

- The transmission from higher headline inflation, to higher wage demands, to higher services inflation is a key propagation mechanism ECB officials are concerned about. However, our previous work has shown that the labour market is less tight than in 2022, potentially suggesting weaker worker bargaining power.

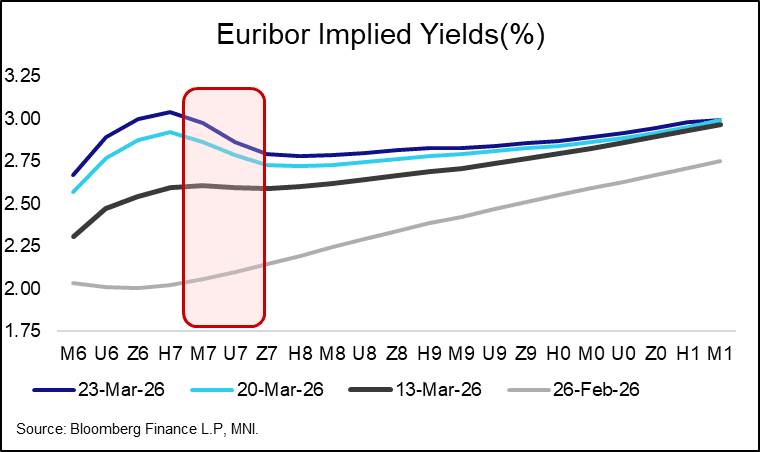

STIR: EUR STIRs – Pricing In The “Policy Mistake”

Mar-23 08:50

- While it is difficult to have much confidence fading front-end hawkish repricing in the current market environment, those believing the ECB is making a “policy mistake” by delivering pre-emptive hikes may look to position for continued flattening in 2027 curves.

- The Euribor implied terminal rate for the anticipated hiking cycle is currently 3.04%, associated with the H7 contract. That’s up from 2.92% at Friday’s settle, 2.60% on March 13 and 2.03% before the Iran war started.

- Beyond March 2027, the Euribor curve starts to price in an unwind of these hikes, with the H7/Z7 spread currently at -24.5 ticks. This reflects the negative growth impact of both sharp rate hikes and the energy price shock itself.

- The memories of 2022 mean the bar to ECB hikes in the face of an energy supply shock is lower than before. However, the differing demand/labour market backdrop in 2026 could mean the risk of second round effects is smaller than four years ago.

- That would work against the hawkish assumptions embedded in the ECB’s March alternative scenarios, which “incorporate stronger indirect and second-round inflation effects than those implied by standard model-based elasticities in order to account for non-linearities in the transmission of large inflationary shocks to prices and wages, such as those seen during the 2021-22 energy crisis”