US TSYS: Modestly Bid; Pre-FOMC Blackout Beckons

U.S.Tsys have richened as we have worked our way through the Asia-Pac session, unwinding a little of Thursday’s cheapening in the process.

- The move higher comes amidst softness in the USD (DXY), as the JPY has strengthened on fresh warnings from the likes of BoJ Gov. Kuroda and FinMin Suzuki re: yen weakness, adding to

- TYZ2 is -0-01 at 115-30 last, just shy of session highs, but coming nowhere near to approaching its peak on Thursday (116-23).

- Cash Tsys run 1.5-3.0bp richer across the curve, with the belly leading the bid. The bid in Tsys has seen 2-Year Tsy yields slip below the 3.50% mark at writing, but remain a little below recent 15-year highs observed on Sep 1 (~3.55%).

- Looking ahead, final July wholesale inventories data is due, with a final round of scheduled Fedspeak by Chicago Fed Pres Evans (‘23 voter), Gov. Waller (voter), and Kansas City Fed Pres George (voter) due ahead of the pre-FOMC blackout period (Sept. 10-22).

- Note that Pres Evans is due to speak on”career opportunities in economics”, and is unlikely to cover comments on monetary policy.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUND TECHS: (U2) Corrective Pullback

- RES 4: 161.38 2.00 projection of the Jun 16 - 24 - 28 price swing

- RES 3: 160.00 Round number resistance

- RES 2: 159.79 High Apr 4 (cont)

- RES 1: 158.33/159.70 High Aug 3 / 2 and the bull trigger

- PRICE: 156.36 @ 05:25 BST Aug 10

- SUP 1: 155.72/155.16 Low Aug 5 / 20-day EMA

- SUP 2: 153.36 50-day EMA

- SUP 3: 149.69 Low Jul 21 and key short-term support

- SUP 4: 148.24 Low Jul 1

The Bund futures outlook is unchanged and the S/T trend direction is up. The latest pullback is considered corrective. A fresh high last week reinforced the bull theme and confirmed a resumption of the uptrend. MA studies are in a bull mode condition. The focus is on 159.79 next, Apr 4 high (cont). Key trend support has been defined at 149.69, Jul 21 low. A break is required to signal a potential top. Initial firm support is 155.16, the 20-day EMA.

USD: Recent Upside US CPI Surprises Haven't Seen Much USD Follow Through

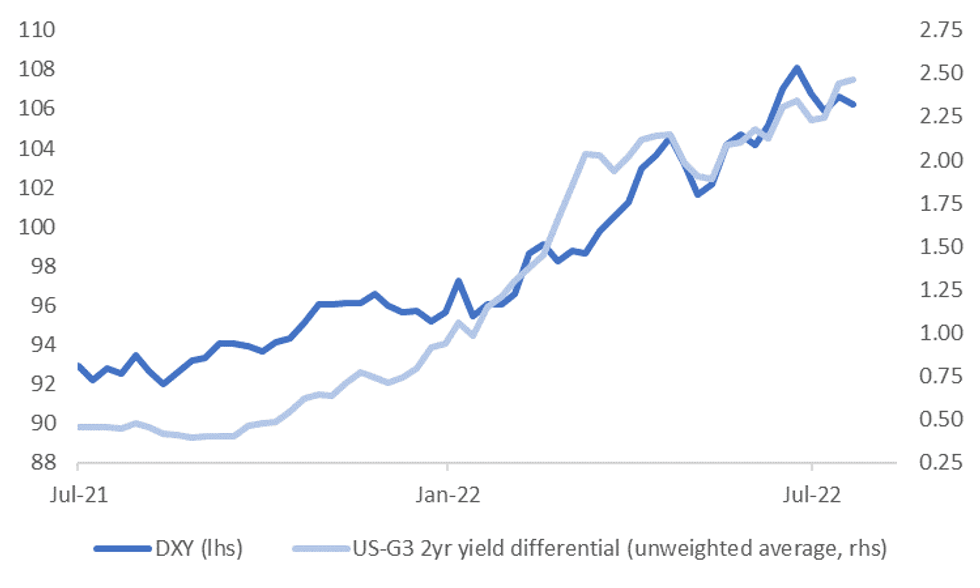

The DXY has drifted lower since the start of the week. We sit a little below 106.30 currently, which is slightly weaker than what 2yr yield differentials with the rest of the G3 imply, see the first chart below. To be sure though, the yield differential has only nudged up a touch over this period after last week's strong gains (+20bps). The market is clearly awaiting this week's key event risk in terms of tonight's US CPI print.

Fig 1: DXY Versus The 2yr Yield Differential

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

- Whilst this may leave the risks skewed to the upside for the USD, particularly if the CPI surprises on the upside, in recent months there hasn't been a great deal of follow through USD strength post inflation outcomes.

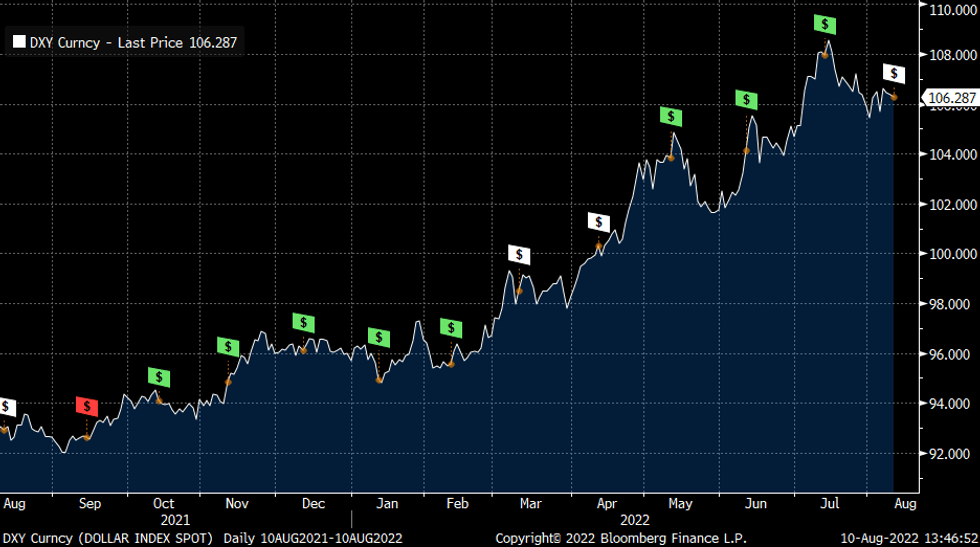

- The second chart below plots the DXY against US CPI release dates (the $ symbols on the chart). Green symbols represent upside surprises, while white symbols are as expected outcomes, red symbols are downside surprises relative to expectations.

- The last 3 CPI prints have been upside surprises for the CPI, but the DXY peaked shortly after each print. Part of this no doubt reflected profit taking to a degree, as the USD typically rallied ahead of these releases. The market may have also felt we were getting closer to peak inflation pressures in the US.

- The set-up is different this time around, with the USD broadly range bound to slightly lower in recent weeks and not rallying like has been the case in recent months. This is a caveat to keep in mind in terms of expecting a repeat outcome following tonight's US CPI release.

Fig 2: DXY Has Peaked Shortly After Recent US Inflation Beats

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

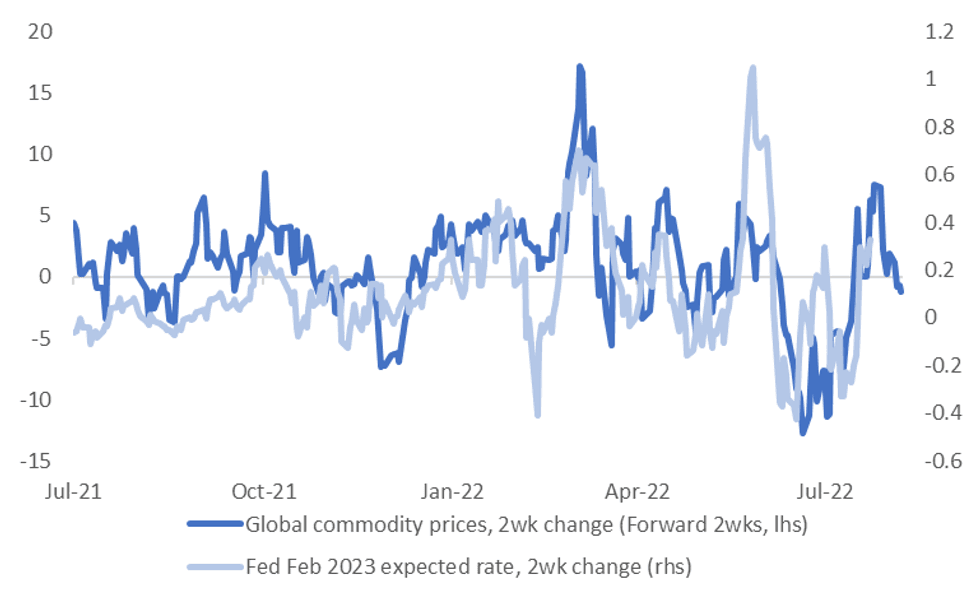

- There can still be other influences on the Fed hiking outlook, although we would note pricing for early 2023 Fed fund levels has caught up with the recent rebound in commodity prices, see the final chart below.

Fig 3: US Fed Expectations & Commodity Price Changes

Source: MNI/Market News/Bloomberg

Source: MNI/Market News/Bloomberg

EQUITIES: Lower In Asia; Tech Sentiment Softens After Micron Warning

Virtually all Asia-Pac equity indices are softer at typing amidst underperformance in tech-related names, tracking the tech-led decline on Wall St. after Micron Technology’s warning re: the weakened demand outlook for chips (adding to prior, similar warnings from the likes of Nvidia and Intel).

- Chinese and Hong Kong stocks fell to session lows in the wake of Chinese inflation data that had missed expectations but showed CPI hitting two-year highs, driving down expectations from some quarters re: PBOC monetary easing going forward.

- The Hang Seng deals 2.1% weaker, hitting fresh one-week lows with nearly every constituent in the red at writing. China-based tech struggled (HSTECH: -3.1%), adding to heavy losses observed in the Hang Seng’s finance (-1.3%) and property (-1.6%) sub-indices amidst persistent sector-wide gloom after Hong Kong regulators clarified earlier on Tuesday that there are no plans for the relaxation of stamp duties on home purchases.

- The CSI300 trades 0.9% lower, led by losses in richly-valued consumer staples and healthcare equities. The ChiNext index deals 1.0% weaker at writing, reflecting underperformance in chipmakers in the wake of Micron’s announcement,

- The ASX200 sits 0.2% worse off at writing, with heavy losses in tech (S&P/ASX All Tech Index: -2.4%) countering gains in commodity-related and financial equities.

- The Taiex sits 0.6% weaker at typing, with index heavyweight TSMC (-1.6%) contributing the most to losses.

- E-minis are flat to 0.1% worse off at typing, holding on to the bulk of their losses observed on Tuesday.