STIR: Modest Hawkish Extension In Fed Pricing On Claims Data

Jan-22 14:05

Modest hawkish extension in the USD short end after weekly jobless claims data registers lower than expected figures.

- SOFR futures +0.25 to -2.5 vs +0.25 to -1.0 into the data, with implied terminal rate pricing 3.185% vs. 3.175% pre-data.

- SFRZ6 is set for the lowest close since July 15.

- Dec-FOMC dated OIS now prices ~42bp of easing vs. ~50bp late last week and 43bp heading into the data. Data flow, reduction in global risk premia and lower odds of NEC Chair Hassett succeeding outgoing Fed Chair Powell have all factored into this week’s repricing.

- Further forwards, 1bp of easing priced for this month, 4bp through March, 8bp through April and 18.5bp through June, incrementally more hawkish than pre-release levels.

- Our macro team notes that the latest weekly claims data maintained the theme of a low-firing, low-hiring environment ahead of the Fed's next meeting on Jan 27-28. But the latest improvements will affirm conviction for a rate hold in the absence of further deterioration in the labour market - indeed, judging from claims alone, it has notably steadied in the last few months.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: Hawkish Fed Repricing After Firm GDP

Dec-23 14:04

Contained hawkish repricing on the back of the much-firmer than-expected GDP & headline PCE data, adding to the modest hawkish reaction that followed the weekly ADP employment release. Major short end metrics stick within recent ranges.

- 55bp of easing now priced into Fed Funds futures across ’26 vs. 58.5bp pre-data.

- In terms of market views around the next rate cut, ~19bp of easing is priced through April, with 32bp showing through May. That compares to 22bp and 35bp ahead of the data.

- SOFR futures now -0.5 to -4.0 on the day. SOFR-implied terminal rate pricing 3.16% vs. 3.11% heading into ADP.

- Looking closer at the data, consumption and net exports provide the most meaningful contribution the GDP beat, and there weren’t any major caveats, making for a strong overall reading.

US TSY FUTURES: Post-Data Update

Dec-23 14:04

- Treasury futures extending post-data lows, TYH6 -4.5 at 112-06.5 vs. 112-05.5 low, albeit on light pre-holiday volume of 340k. Revisiting last week Monday lows.

- Curves bear flattening: 2s10s -.377 at 65.022, 5s30s -1.775 at 110.421. A resumption of weakness would refocus attention on 111-29, the Dec 10 low and a key short-term support. A breach of this support resumes the bear cycle that started Oct 17.

- Up next: IP/Cap-U at 0915ET, Conf Board Consumer Confidence & Richmond Fed Mfg Index at 1000ET.

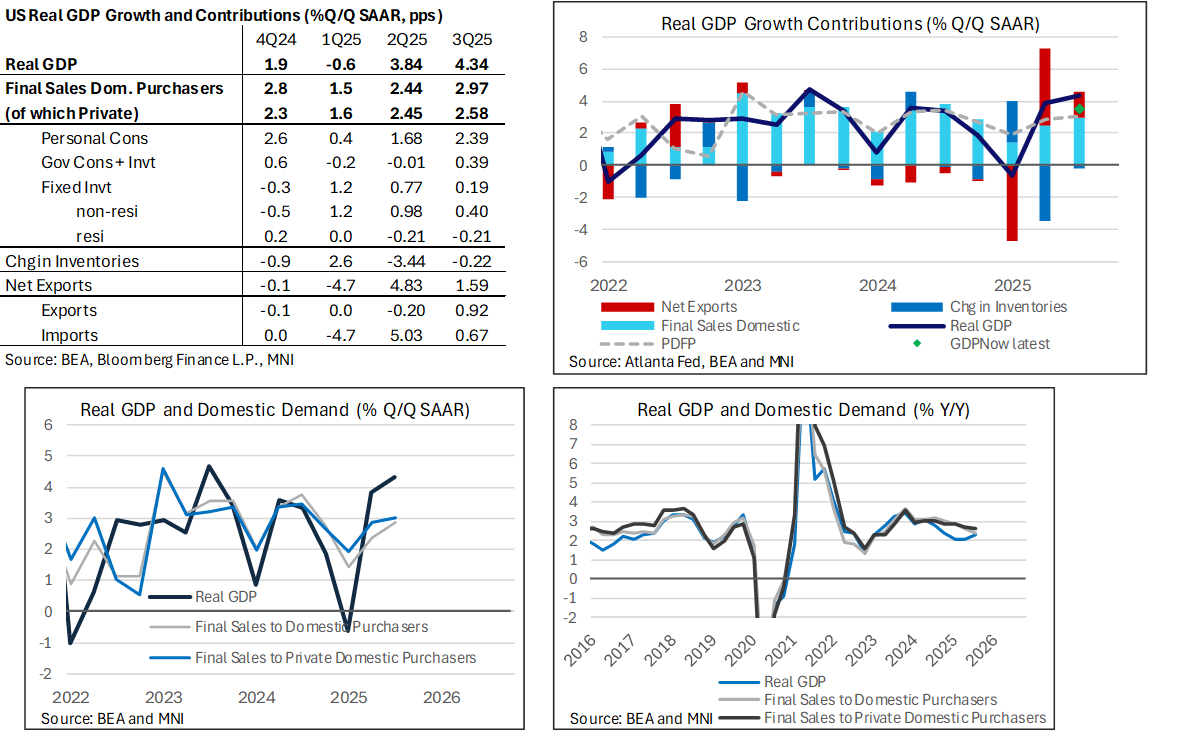

US DATA: Consumption Drives Surprisingly Strong Q3 GDP With Help From Trade

Dec-23 13:56

Real GDP growth was clearly stronger than most expected in the “initial” Q3 release, with the largest upside coming from personal consumption but also with a larger than expected boost from net exports that was only partly offset by a larger than expected drag from inventories. Real GDP increased a strong 4.3% whilst PDFP was also solid at 3.0%.

- Real GDP was stronger than most expected in the first look at Q3 data, rising 4.3% annualized vs 3.5% in Atlanta Fed’s GDPNow and 3.3% for Bloomberg consensus. That said, the Dallas Fed’s weekly economic index had been pointing to a 4+% increase.

- Personal consumption saw an impressive beat at 3.5%, considering September PCE data released on Dec 5 had implied a 2.7% increase, which unsurprisingly had fed into both GDPNow and consensus. It saw PCE add 2.4pp to annualized GDP growth vs the 1.84pp estimated by GDPNow.

- Sticking to domestic demand components, the government added a reasonable 0.4pp (GDPNow 0.3pp) whilst fixed investment moderated to 0.2pp (GDPNow 0.3pp).

- Strip out the government and PDFP increased a robust 3.0% annualized in Q3 after 2.9% in Q2 and 1.9% in Q1, for its fastest quarterly rate since 3Q24.

- As for more volatile components, there was an upside surprise for net exports (added 1.6pps vs 1.0pp in GDPNow, after 4.8pp in Q2 and -4.7pp in Q1) that was only partly offset by a miss for changes in inventories (-0.2pp vs 0.1pp in GDPNow, after -3.4pp in Q2 and 2.6pp in Q1).

- Taking somewhat of a step back, real GDP growth stood at 2.3% Y/Y in Q3 (GDPNow had implied 2.1%, Dallas Fed WEI 2.4%). That leaves it in good stead to exceed the FOMC median forecast of 1.7% for 4Q25 having only been revised a tenth higher less than two weeks ago.

- PDFP meanwhile moderated a tenth but remains firm at 2.6% Y/Y, having averaged 2.8% since 1Q23-2Q25.