AUSSIE BONDS: Modest Bull-Flattener Ahead Of US CPI Data

Sep-11 2025 05:01

ACGBs (YM +2.0 & XM +4.0) are modestly stronger after today's inflation expectations data.

- Melbourne Institute consumer inflation expectations jumped back to 4.7% in September, in line with July, after moderating in August to 3.9%. Q3 averaged 4.4% unchanged from Q2, signalling no progress on this front with the series zigzagging sideways for over a year. While petrol prices declined in August and September, they were little changed on the quarter in Q3. The widely reported July CPI jumped 0.9pp to 2.8% y/y with the trimmed mean up 0.6pp to 2.7%, which Westpac noted may have been driven by consumer expectations for the lower economic outlook in September.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's US CPI data.

- Cash ACGBs are 2-3bps richer with the AU-US 10-year yield differential at +19bps.

- The bills strip is little changed, with a slight flattening bias.

- A 25bp rate cut in September is given a 12% probability, with a cumulative 29bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will be empty apart from RBA Brad Jones' appearance at the FINSIA Regulators Conference.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

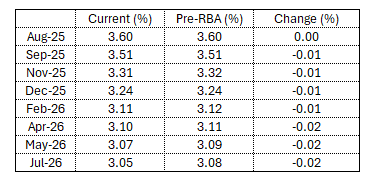

STIR: RBA Dated OIS Slightly Softer After RBA Cuts 25bps

Aug-12 2025 05:00

RBA-dated OIS pricing is flat to 2bps softer across meetings after the decision, with mid-2026 leading.

- A 25bp rate cut in August was given a 97% probability.

- A cumulative 36bps of easing priced by year-end.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA

Source: Bloomberg Finance LP / MNI

BONDS: NZGBS: Subdued Session Ahead Of US CPI Data

Aug-12 2025 04:51

NZGBs closed little changed after trading in narrow ranges on a data-light day.

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's US CPI data.

- (MNI) The CPI report for July is released on Tuesday Aug 12, at 0830ET. Consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June and unrounded analyst estimates broadly echo this with a median 0.32% M/M. It would mark a further acceleration from 0.23% M/M in June and 0.13% M/M in May for its fastest pace since January, with the latest firming seen coming from core goods inflation doubling to 0.4% M/M.

- Swap rates are unchanged.

- With the next RBNZ meeting approaching (August 20), this week contains a number of high frequency releases that the MPC monitors and should give a sense for how the economy began Q3.

- July card spending is out tomorrow and while it is off its lows, growth has remained soft. There could be some payback in the month following the 0.5% m/m rise in June.

- RBNZ dated OIS pricing is unchanged across meetings. 23bps of easing is priced for August, with a cumulative 40bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 2.75% Apr-37 bond.

AUSSIE BONDS: RBA Cuts As Expected, Limited Reaction

Aug-12 2025 04:49

ACGBs (YM -0.5 & XM -1.0) are moderately richer after the RBA cut the cash rate by 25bps to 3.60%.

- The Board noted that inflation continues to moderate toward the 2–3% range. Trimmed mean inflation fell to 2.7% and headline inflation to 2.1% in the June quarter. Domestic demand is gradually recovering, household incomes have risen, and labour market conditions, though easing, remain tight.

- With 75bps of cuts this year, the Board remains cautious but ready to respond to shifts in global or domestic conditions, maintaining its focus on price stability and full employment.

- Cash ACGBs are 1-2bps richer after the RBA decision, with the AU-US 10-year yield differential at -2bps.

- Swap rates are 2-4bps lower after the decision, with the 3s10s curve steeper.

- The bills strip has richened since the decision but sits flat on the day.

- RBA-dated OIS pricing is flat to 3bps softer across meetings after the decision, mid-2026 leading. A 25bp rate cut in August was given a 97% probability today. A cumulative 36bps of easing priced by year-end.

- Tomorrow, the local calendar will see the Q2 Wage Price Index.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond tomorrow and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.