MNI US OPEN - Trump Wants 'Real End' to Iran Nuclear Programme

EXECUTIVE SUMMARY

- TRUMP WANTS 'REAL END' TO IRAN'S NUCLEAR PROGRAMME

- TRUMP SAYS G-7 EXIT FOR ‘MUCH BIGGER’ REASON THAN CEASEFIRE

- BOJ KEEPS RATE AT 0.5%; JGB TAPER TO JPY200 BLN

- EU SPURNS ECONOMIC DIALOGUE WITH CHINA OVER DEEPENING TRADE RIFT

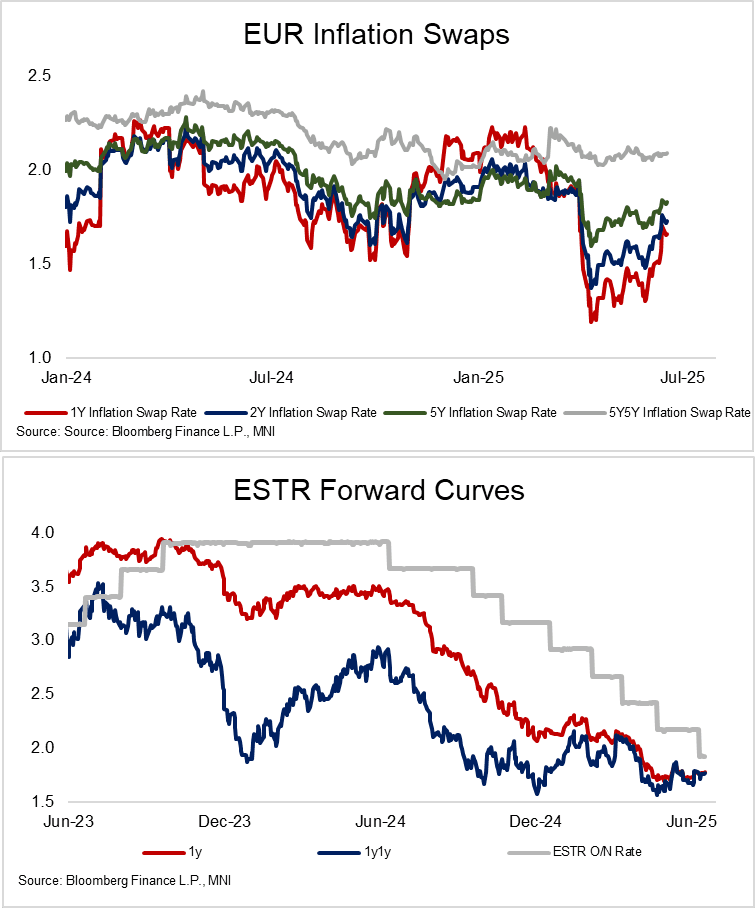

Figure 1: Fresh upside for oil drives light hawkish repricing in EUR rates

NEWS

POLITICAL RISK (MNI): Trump Wants 'Real End' to Iran's Nuclear Programme

Jennifer Jacobs at CBS puts two lengthy posts on X after US President Donald Trump left the G7 early. Some of the main points noted below: Trump says he needs to be in the White House Situation Room where he can be "well versed" on the state of play in the Middle East. Calls for a "real end" to Iran's nuclear programme with Iran "giving up entirely" on nuclear weapons. Says Israel is not slowing its barrage on Iran. Says he may end VP JD Vance or Middle East envoy Steve Witkoff to talk to Iran. Says US would "come down so hard if they do anything to our people," re: threats to US bases in Middle East. Says he hope Iran's nuclear programme "is wiped out long before [US involvement]."

US (MNI): Trump - 'Not in Mood To Negotiate' w/Iran, Wants 'Complete Give-Up' on Nukes

Speaking to reporters aboard Air Force One, President Donald Trump says on the situation in the Middle East, says he is looking for "better than a ceasefire" in Iran. Says he is "not too much in the mood to negotiate" with Iran on its nuclear programme and wants a "complete give-up" on its enrichment efforts. On trade and tariffs, Trump says that the EU is "not yet offering a fair deal on trade". Says that pharmaceutical tariffs are coming "very soon". Says he may offer Canada a separate deal to become part of Trump's touted 'golden dome' project. Adds that Canada will have to pay to participate.

US/MIDEAST (CNN): Israel Says Iran Was Racing Toward a Bomb. US Intelligence Says It Was Years Away

When Israel launched its series of strikes against Iran last week, it also issued a number of dire warnings about the country’s nuclear program, suggesting Iran was fast approaching a point of no return in its quest to obtain nuclear weapons and that the strikes were necessary to preempt that outcome. But US intelligence assessments had reached a different conclusion – not only was Iran not actively pursuing a nuclear weapon, it was also up to three years away from being able to produce and deliver one to a target of its choosing, according to four people familiar with the assessment.

US (BBG): Trump Says G-7 Exit for ‘Much Bigger’ Reason Than Ceasefire

US President Donald Trump said his early departure from the Group of Seven leaders meeting in Canada has “nothing to do” with working on a ceasefire between Israel and Iran, instead saying his reason is “much bigger than that.” In comments to reporters aboard Air Force One, Trump later said he wants a “real end” to the nuclear problem with Iran, including the country “giving up entirely” on the idea of nuclear weapons and their existing nuclear program “wiped out,” rather than simply obtaining a ceasefire in the region, according to CBS.

US (NYT): 36 More Countries May Be Added to Trump’s Travel Ban

The Trump administration is considering expanding President Trump’s new travel ban to as many as 36 additional countries if they do not address various security or diplomatic concerns within two months, according to a June 14 cable reviewed by The New York Times. Most of the countries are in Africa, while others are in the Caribbean, the Pacific region and Central Asia. The cable says that in addition to the 19 countries, the State Department had identified 36 more that must improve on certain benchmarks within 60 days. It set a deadline of 8 p.m. Eastern time on Wednesday for the affected governments to provide remediation plans.

US (BBG): Trump Tax Bill to Boost Biden’s Chip Tax Credit to 30%

The Senate’s draft tax bill calls for increasing an investment credit for semiconductor manufacturers, a potential boon for chipmakers that the Trump administration is urging to increase the size of their US projects. The measure would increase the tax credit to 30% of investments in plants, up from 25%, giving chipmakers further incentive to break ground on new facilities before an existing 2026 deadline.

US/CHINA (WSJ): Trump Officials Weighed Broader China Tech Restrictions Ahead of Trade Talks

Commerce Department officials weighed new export limits on critical technology going to China ahead of recent trade talks in London, adding to the Trump administration’s arsenal if tensions between Washington and Beijing escalate again. The Commerce Department unit overseeing export controls in recent weeks weighed tougher limits on semiconductors, including cutting off sales to China of a wider swath of chip-manufacturing equipment, people familiar with the matter said. Such a move would have covered equipment used to make everyday semiconductors, expanding beyond existing export limits on equipment for producing advanced chips.

US/JAPAN (BBG): Trump, Ishiba Fail to Reach Trade Deal at G-7 Summit

US President Donald Trump and Japanese Prime Minister Shigeru Ishiba failed to reach an agreement on a trade package on the sidelines of the Group of Seven summit, an outcome that leaves the Asian nation inching closer to a possible recession as the pain of US tariffs hits its economy. “There are still some points on which the two sides are not on the same page, so we have not yet reached an agreement on the trade package,” Ishiba said to reporters on Monday in Calgary in between G-7 meetings.

US/CANADA (BBG): Carney Says Canada and US Aiming For Trade Deal Within 30 Days

Prime Minister Mark Carney said Canada and the US are aiming to strike a trade deal within a month, a goal set during a meeting with US President Donald Trump at the Group of Seven summit. “We agreed to pursue negotiations toward a deal within the coming 30 days,” Carney said in a post on X on Monday afternoon. Trump told reporters that he and Carney still have differences over policy but that trade deal was “achievable” in the coming weeks. The president directed his team to make the best possible deal, as quickly as possible, according to a White House official.

BOJ (MNI): BOJ keeps Rate at 0.5%; JGB Taper to JPY200bln

The Bank of Japan Board on Tuesday unanimously decided to keep its unsecured overnight call rate at 0.50%, while announcing a slower pace of JGB purchase reductions to JPY200 billion per quarter from the current JPY400 billion. The BOJ said it will begin reducing JGB purchases at the slower pace from April 2026 through March 2027, with the program to be reviewed again in June 2026. The Bank also projected that its long-term JGB purchases in Q12027 will total about JPY2.1 trillion, down from JPY2.9 trillion in Q1 2026.

BOJ (MNI): Ueda Flags Gradual Hikes, Warns on JGB Volatility

Bank of Japan Governor Kazuo Ueda said Tuesday the central bank intends to raise its policy interest rate gradually to adjust the current highly accommodative stance, noting that real interest rates remain significantly low, following the Board's decision to hold the 0.5% policy rate. However, Ueda gave no specific guidance on the timing or method of the next rate hike, emphasising that any decision will depend on economic and price developments, which remain highly uncertain. The overall outlook for the economy and prices has not changed significantly from the previous meeting but the BOJ is closely watching the recent rise in crude oil prices, he added.

G7 (BBG): G-7 Leaders Seek ‘Resolution’ of Iranian Crisis in Statement

The Group of Seven leaders pushed for a de-escalation in the Middle East but didn’t call for an immediate end to the conflict between Israel and Iran in a statement that also affirmed Israel’s right to defend itself. “We urge that the resolution of the Iranian crisis leads to a broader de-escalation of hostilities in the Middle East, including a ceasefire in Gaza,” the leaders said in the statement.

EU/CHINA (FT): EU Spurns Economic Dialogue With China Over Deepening Trade Rift

The EU has refused to hold a flagship economic meeting with Beijing ahead of a leaders’ summit next month because of a lack of progress on numerous trade disputes, according to four people familiar with the matter. The bloc’s stonewalling of the talks, known as the EU-China High-Level Economic and Trade Dialogue, underlines the deep divisions between the sides despite Beijing’s efforts to court Europe as a counterweight to the US amid President Donald Trump’s tariff war.

ECB (MNI EXCLUSIVE): New Dutch CB Chief Seen as Moderate Hawk

Eurosystem sources give their view on the incoming Dutch central bank chief. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

ECB (BBG): ECB Has Found ‘Equilibrium’ on Rates, Prices, Growth: Stournaras

European Central Bank Governing Council member Yannis Stournaras says it seems the euro area has reached an equilibrium when it comes to inflation, banking-sector developments and economic growth. “It seems we have reached inflation of 2%, interest rates of 2% so the central bank’s real rate is zero,” Stournaras says in transcript of interview with Greek state TV on Monday. “We are at a first point of equilibrium. We don’t know whether this equilibrium will be maintained.”

Ahead of the publication of the MPC policy decision on Thursday, May CPI data will be published on Wednesday at 7:00BST (although the MPC will already have advance access to the data as of Monday morning). The ONS' VED (road tax) component error in the April dataset which boosted headline CPI by around 0.13ppt (on our calculations core by 0.16ppt and services CPI by 0.25ppt) will be reversed in the May data.

UK (FT): Reeves Considers Changes to Non-dom Inheritance Tax Amid UK ‘Exodus’

Chancellor Rachel Reeves is exploring reversing a decision to charge UK inheritance tax on the global assets of non-doms, following a spate of departures and lobbying by the City of London, according to government officials and financiers briefed on the discussions. The exposure of worldwide assets to inheritance tax at 40 per cent — which came into force in April — is the element of scrapping the non-dom regime that is “causing most heartburn”, one government official said. The Treasury is reviewing the decision, they added. Another official confirmed the Treasury would change the inheritance tax regime for non-doms if it was found to be good for Britain’s international competitiveness.

RUSSIA/N.KOREA (BBG): Russia’s Shoigu Meets with North Korea’s Kim Jong Un: Tass

Russia’s Security Council Secretary Sergei Shoigu started meeting with North Korea’s leader Kim Jong Un in Pyongyang, Tass reports, citing Security Council’s press service. Shoigu arrived in North Korea on a special assignment from President Vladimir Putin.

BRAZIL (BBG): Brazil Congress Threatens to Deal Fresh Blow to Lula Fiscal Plan

President Luiz Inacio Lula da Silva’s efforts to shore up Brazil’s budget are on the brink of another setback after Congress advanced a push to block tax increases on some financial transactions from taking effect. Lower house lawmakers on Monday approved by 346-97 votes an urgency request to overturn a governmental decree raising so-called IOF taxes. The procedural move opens the door to the floor vote on a proposal to cancel the measure.

CENTRAL BANK PREVIEWS

MNI FED PREVIEW - JUNE 2025: Holding in Anticipation

The FOMC will hold rates for a 4th consecutive meeting in June, and continue to convey a patient stance on future rate cut decisions amid elevated policy-related uncertainty. The new quarterly projections will still signal the resumption of rate cuts later this year, but likely only one 25bp reduction instead of the two cuts envisaged at the March meeting. While risks to both the Fed’s inflation and employment mandates remain elevated, with the new 2025 forecasts looking increasingly reflective of stagflation, the Committee should still signal rate cuts through end-2026 of a similar magnitude to its previous set of projections.

MNI RIKSBANK PREVIEW - JUNE 2025: How Low Will the Rate Path Go?

The Riksbank is expected to cut rates by 25bps to 2.00% on Wednesday, following through on the slight dovish tilt incorporated into the May policy statement. Data since May has veered in a dovish direction, with soft activity signals coming alongside an easing of inflationary pressures. As such, a cut towards the lower end of the Riksbank’s 1.50-3.00% neutral range appears prudent to offer further support to Sweden’s rate-sensitive economy. The June decision includes an updated Monetary Policy Report and rate path projection. Developments since March support a downward revision to the rate path from its current flat 2.25% level, but we don’t expect the path to move much below 2.00%.

MNI BCB PREVIEW - JUNE 2025: Hike or Hold, Caution to Remain

A narrow majority of analysts lean towards the BCB keeping the Selic rate steady in June at 14.75%. This follows lower-than-anticipated inflation figures last week, better behaved inflation expectations and the strong performance for the Brazilian real across 2025. However, with economic activity appearing resilient and the labour market still tight, the Copom may opt to hike rates by a further 25bp, as the committee continues to stubbornly pursue the convergence of inflation to target.

MNI BCCH PREVIEW - JUNE 2025: Easing Cycle Resumption Nears

The majority of analysts expect Chile’s central bank to keep its policy rate unchanged at 5.00% in June, amid a still uncertain external backdrop (exacerbated by recent geopolitical developments) and elevated inflation pressures. However, the BCCh has adopted a more dovish tone in Q2 and even discussed cutting the policy rate at the April meeting. Further benign inflation readings and improving inflation expectations suggest the resumption of the easing cycle is on the horizon, and there are some notable calls for the BCCh moving as soon as this week.

MNI BI PREVIEW - JUNE 2025: Consecutive Cuts Unlikely

Bank Indonesia's (BI) decision is announced on June 18 and it is likely to keep rates at 5.5% after cutting them 25bp in May, although 9 out of 31 analysts on Bloomberg expect another 25bp reduction. With the focus remaining on the currency, we believe that BI will be cautious regarding back-to-back easing given that the Fed is widely expected to be on hold this month and it isn’t expected to resume cutting until later this year.

DATA

GERMAN DATA (MNI): June ZEW Mirrors Brightening German Outlook

- GERMANY ZEW JUN ECONOMIC EXPECTATIONS 47.5

- GERMANY ZEW JUN CURRENT CONDITIONS -72

The German ZEW expectations index outperformed in June, rising from 25.2 to 47.5 in June, higher than consensus of 35.0 but remaining below March's 3-year high of 51.6. The current conditions index meanwhile was also stronger than expected as it improved from -82.0 to -72.0 (consensus -75.0). Wider sentiment has ticked up in Germany recently although remains subdued. Recall that the IFO institute in its latest economic projections believes the economy has moved past its weakest levels: "The crisis in the German economy reached its low point in the winter". That forecast round included a 0.1pp upward revision to GDP growth of 0.3% in 2025 and a more notable +0.7pp to 1.5% in 2026.

SWEDEN DATA (MNI): May Unemployment Rate Above Consensus, But 3mma Below Riks Forecasts

- SWEDEN MAY UNEMPLOYMENT 9.7%

The Swedish LFS unemployment rate surprisingly rose to 9.0% in May, above the 8.6% consensus and last month's 8.5% reading. The LFS data can be volatile, so it's important not to put too much stock in individual monthly outcomes. The 3mma of the unemployment rate was steady at 8.5%, so is still tracking below the Riksbank's Q2 forecast of 8.8%. The Riksbank will present updated projections in tomorrow's June MPR. Despite this, there certainly isn't enough in the report to push back on expectations for a 25bp cut tomorrow.

FOREX: JPY Looks Through Slowing of Cuts to Bond Buys, GBP Sold on Rallies

- The Bank of Japan rate decision came in broadly as expected, and while signals were given over a slower pace of cuts to their bond-buying program, this meant little to the JPY currency, which remains inside the recent range. Spot remains below last week’s high. Recent weakness suggests the correction between Jun 3 - 11, is over. The trend direction is down - moving average studies are in a clear bear-mode position, highlighting a dominant downtrend.

- GBP trades poorly, and is fading against all others in G10. As a result, GBP/USD has again struggled to hold gains above 1.36 and is on the backfoot. As such, the sell-on-rallies theme remains dominant. The outlook will deteriorate on any break and close below 1.3456, which would signal the first phase of a corrective pullback. 1.3371, the 50-dma, and 1.3270 are the first downside targets here. UK CPI prints early Wednesday ahead of the BoE rate decision on Thursday.

- In the crosses, NZDJPY is threatening to break above 87.95, which would be the highest close since January, placing the focus on the year’s highs at 89.71. For AUDNZD, spot has been consolidating in a 1.0750/1.0800 range, however MA studies do highlight bearish momentum. A sustained break above 1.0825 would be required to alter this trend.

- The US retail sales print for May is next up, with markets on watch for a slowdown in the advance retail sales headline to -0.6% from +0.1% prior. Import and export price indices will be released alongside. ECB's Villeroy and Centeno are set to speak, while the Fed remain inside their pre-rate decision media blackout period.

EGBS: Bund Futures Rangebound, Awaiting Next Material Middle East Development

- Bund futures have traded in a tight 34 tick range, currently -23 ticks at 130.62. Geopolitical tensions between Israel and Iran continue to dominate headline flow, with fixed income markets having to weigh up fresh inflation risks alongside weaker risk sentiment. Today’s subdued price action is somewhat suggestive of headline fatigue, until the next material development in the conflict arises.

- The recent pullback in Bunds is still considered corrective for now, with key short-term support seen at 130.12, the Jun 5 low.

- Meanwhile, US President Trump has provided renewed hawkish rhetoric with respect to a trade deal with the EU.

- German yields are 1-2bps higher, with the short-end underperforming. There was limited impact from the stronger-than-expected German June ZEW survey (expectations component 47.5 vs 35.0 cons, 25.2 prior).

- The EU is tapping the 3.375% Oct-39 EU-bond via syndication today, with a E5bln WNG transaction. The size came in at the bottom of MNI’s expected range. German also sold Green Bunds this morning, with solid results.

- 10-year EGB spreads to Bunds are biased wider, with equity risk sentiment dented by a re-escalation of the conflict in the Middle East.

- ECB’s Stournaras re-iterated previous comments, noting that we have “reached an equilibrium based on developments in inflation”.

GILTS: Off Lows After Auction, Curve Holds Steeper

Gilts hold lower given cues from global peers and with crude oil off yesterday’s lows, although solid demand at the latest 5-Year auction has provided some support in recent trade.

- Futures stick within yesterday’s range, trading as low as 92.37 before recovering to ~92.50.

- Bullish technical conditions remain intact in the contract, initial support and resistance located at yesterday’s low (92.23) & the 50.0% retracement of the Jun 13-16 down leg (92.95), respectively.

- Yields 1-3bp higher, curve steeper.

- 2s10s and 5s30s stick within multi-week ranges, stabilising back above 60bp and 120bp, respectively.

- BoE-dated OIS is little changed on the day, showing ~48bp of cuts through year-end, with the next 25bp step almost fully discounted through the end of the September MPC (~24.5bp of easing showing through that horizon).

- SONIA futures flat to -3.0.

- Expect global cues to dominate for the remainder of the day, with ongoing focus on the next stages of the Israel-Iran conflict.

- Locally, CPI data will cross on Wednesday, ahead of the BoE’s Thursday decision.

- We see downside risks to the headline and services CPI reading.

- Still, the data shouldn’t have too much impact on the BoE decision, with no change expected by both the sell-side and markets, but a low print could impact the vote split.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.211 | -0.2 |

Aug-25 | 4.023 | -19.0 |

Sep-25 | 3.967 | -24.5 |

Nov-25 | 3.813 | -40.0 |

Dec-25 | 3.736 | -47.7 |

Feb-26 | 3.623 | -59.0 |

Mar-26 | 3.595 | -61.8 |

EQUITIES: Eurostoxx 50 Futures Breach 50-Day EMA Following Latest Pullback

The latest pullback in the Eurostoxx 50 futures contract has resulted in a breach of the 50-day EMA at 5299.04. Price has also pierced 5255.00, the May 23 low. A clear break of both support points would signal a short-term top and highlight scope for a deeper retracement. This would open 5178.00, the May 6 low and 5081.16, a Fibonacci retracement. Initial resistance to watch is 5363.03, the 20-day EMA. The trend condition in S&P E-Minis is unchanged, it remains bullish and the contract traded to a fresh cycle high last Wednesday, reinforcing current bullish conditions. For now, the most recent pullback is considered corrective. The contract has pierced support at 6000.18, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5890.99. Key short-term resistance has been defined at 6128.75, the Jun 11 high.

- Japan's NIKKEI closed higher by 225.41 pts or +0.59% at 38536.74 and the TOPIX ended 9.82 pts higher or +0.35% at 2786.95.

- Elsewhere, in China the SHANGHAI closed lower by 1.324 pts or -0.04% at 3387.405 and the HANG SENG ended 80.69 pts lower or -0.34% at 23980.3.

- Across Europe, Germany's DAX trades lower by 275.26 pts or -1.16% at 23420.12, FTSE 100 lower by 35.13 pts or -0.4% at 8839.82, CAC 40 down 53.46 pts or -0.69% at 7687.66 and Euro Stoxx 50 down 51.23 pts or -0.96% at 5287.58.

- Dow Jones mini down 256 pts or -0.6% at 42281, S&P 500 mini down 31.5 pts or -0.52% at 6004.25, NASDAQ mini down 118 pts or -0.54% at 21823.25.

Time: 09:50 BST

COMMODITIES: Bullish Theme in Gold Remains Intact, Recent Gains Bolster Trend

WTI futures traded sharply higher last week and Friday’s early rally marked an acceleration of the current bull phase. Price action is likely to remain volatile near-term, and from a technical standpoint, the trend is currently in an extreme overbought position. A continuation higher would expose the $80.00 handle. A firm support is noted $68.49, the Jun 13 low. A breach of this level would signal scope for a deeper retracement. A bullish theme in Gold remains intact and last week’s gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen the uptrend and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3267.0, the 50-day EMA.

- WTI Crude up $0.79 or +1.1% at $72.59

- Natural Gas up $0.03 or +0.91% at $3.782

- Gold spot down $2.12 or -0.06% at $3383.16

- Copper down $2.65 or -0.54% at $486.55

- Silver up $0.15 or +0.42% at $36.4615

- Platinum up $2.63 or +0.21% at $1251.92

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 17/06/2025 | - | FOMC Meetings with S.E.P. | ||

| 17/06/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/06/2025 | 1230/0830 | *** | Retail Sales | |

| 17/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 17/06/2025 | 1315/0915 | *** | Industrial Production | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/06/2025 | 1400/1000 | * | Business Inventories | |

| 17/06/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 17/06/2025 | 1730/1330 | Bank of Canada Summary of Deliberations | ||

| 18/06/2025 | 2350/0850 | * | Machinery orders | |

| 18/06/2025 | 0600/0700 | *** | Consumer inflation report | |

| 18/06/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 18/06/2025 | 0730/0930 | ECB Elderson At SRB Legal Conference 2025 | ||

| 18/06/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/06/2025 | 0900/1100 | *** | HICP (f) | |

| 18/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/06/2025 | 1230/0830 | *** | Housing Starts | |

| 18/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 18/06/2025 | 1500/1700 | ECB Lane At Macroprudential Conference | ||

| 18/06/2025 | 1515/1115 | BOC Governor speaks in Newfoundland. | ||

| 18/06/2025 | 1600/1200 | ** | Natural Gas Stocks | |

| 18/06/2025 | 1800/1400 | *** | FOMC Statement | |

| 18/06/2025 | 1800/2000 | ECB de Guindos at Osservatorio Permanente Giovani-Editori | ||

| 18/06/2025 | 2000/1600 | ** | TICS | |

| 19/06/2025 | 2245/1045 | *** | GDP |