MNI US OPEN - Trump Pushes for Putin-Zelenskyy Meeting

EXECUTIVE SUMMARY

- 'COALITION OF THE WILLING' TO HOLD CALL AFTER WHITE HOUSE TALKS

- NVIDIA WORKING ON NEW AI CHIP FOR CHINA THAT OUTPERFORMS THE H20

- S&P AFFIRMS US AA+ RATING, KEEPS OUTLOOK STABLE

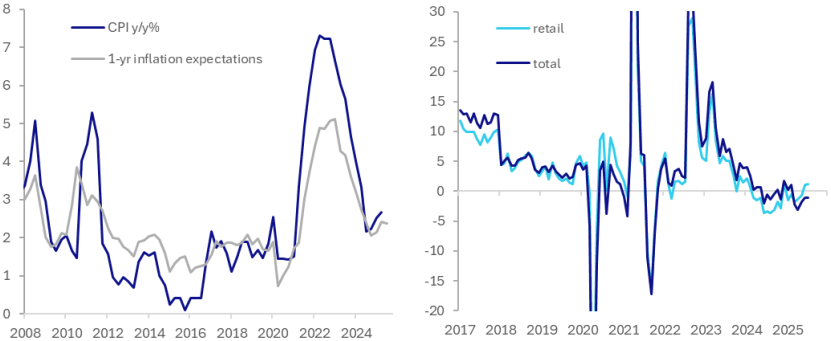

- MNI RBNZ PREVIEW - RATE CUT, FOCUS ON OCR PATH

Figure 1: New Zealand inflation expectations stable (LHS), consumption remains subdued (RHS)

Source: MNI/Bloomberg Finance L.P./ABS

NEWS

SECURITY (MNI): 'Coalition of the Willing' to Hold Call After White House Talks

The 'coalition of the willing' group, formed by countries that have committed to 'boots on the ground' in Ukraine in the event of a ceasefire/peace deal, will hold a national leaders videoconference at 06:00ET/11:00BST/12:00CET. The call will allow those leaders present at the White House talks on 18 August to brief the other leaders on the situation vis-a-vis US security guarantees, a trilateral meeting, and other key outcomes from the talks. The most important outcome of the talks from the perspective of Ukraine and its European allies will be the pledge from US President Donald Trump on security guarantees for Kyiv. Trump instructed Secretary of State Marco Rubio to begin work on establishing what these will look like. They could range from US boots on the ground (the best outcome for Ukraine, but the least likely), to aerial and/or maritime patrols, to providing intelligence and logistical support for Ukraine and its allies.

US/UKRAINE (FT): Ukraine Offers Trump $100bn Weapons Deal to Win Security Guarantees

Ukraine will promise to buy $100bn of American weapons financed by Europe in a bid to obtain US guarantees for its security after a peace settlement with Russia, according to a document seen by the Financial Times. Under the proposals, Kyiv and Washington would also strike a $50bn deal to produce drones with Ukrainian companies that have pioneered the technology since Russia’s full-scale invasion in 2022.

US/CHINA (RTRS): Nvidia Working on New AI Chip for China That Outperforms the H20

Nvidia is developing a new AI chip for China based on its latest Blackwell architecture that will be more powerful than the H20 model it is currently allowed to sell there, two people briefed on the matter said. U.S. President Donald Trump last week opened the door to the possibility of more advanced Nvidia chips being sold in China. But the sources noted U.S. regulatory approval is far from guaranteed amid deep-seated fears in Washington about giving China too much access to U.S. artificial intelligence technology.

US (MNI): S&P Affirms US AA+ Rating, Keeps Outlook Stable

S&P affirmed the AA+/A-1 US credit rating, whilst maintaining a stable outlook. S&P notes: "Amid the rise in effective tariff rates, we expect meaningful tariff revenue to generally offset weaker fiscal outcomes that might otherwise be associated with the recent fiscal legislation, which contains both cuts and increases in tax and spending. We affirmed our 'AA+/A-1+' sovereign credit ratings on the U.S. The outlook remains stable, reflecting our expectation of continued resilience in the U.S. economy; credible, effective monetary policy execution; high, but not rising, fiscal deficits that underpin the increase in net general government debt; and the $5 trillion increase in the debt ceiling."

US (BBG): Trump Administration Said to Discuss Taking 10% Intel Stake

The Trump administration is in discussions to take a stake of about 10% in Intel Corp., according to a White House official and other people familiar with the matter, a move that could see the US become the beleaguered chipmaker’s largest shareholder. The federal government is considering a potential investment in Intel that would involve converting some or all of the company’s grants from the US Chips and Science Act into equity, said the people, who asked not to be identified because the information is confidential.

UK (MNI): Blue Book Advance Estimates Revise Up Economy Size to 2023

Ahead of the publication of the Blue Book on 31 October, the ONS has released some advance aggregate estimates for GDP revisions up to 2023 which will be incorporated into the GDP release on 30 September. The level of nominal GDP is estimated to be 1.5% higher in 2023 than previously, albeit a large part of this was due to pre-2019 changes. At the end of 2023 GDP is now estimated to be 2.2% above the pre-Covid peak (revised up from 1.9%). In per capita terms, it is now 1.0% below the pre-Covid peak (revised from 1.4% below the pre-Covid peak).

INDIA/RUSSIA/CHINA (BBG): Modi Hails ‘Friend’ Putin, Boosts China Ties in Tilt From US

Indian Prime Minister Narendra Modi hailed Russian leader Vladimir Putin as a “friend” while his government moved to bolster relations with China, another sign the South Asian nation is tilting away from the US in the face of Donald Trump’s tariff threats. Modi held a phone call with Putin following the Russian president’s summit with Trump in Alaska. During the conversation, the two discussed issues of bilateral cooperation and agreed to remain in close touch, according to an official statement from New Delhi.

MNI RBNZ PREVIEW - AUGUST 2025: Rate Cut, Focus on OCR Path

The RBNZ meets on Wednesday August 30 and is likely to cut rates 25bp to 3.0%, the mid-point of its estimated "neutral" range. While it paused at the July meeting, it was with a clear easing bias. With the cut widely forecast, attention will be on the revised RBNZ outlook and tone of the statement and press conference. The focus is likely to be on the projected OCR path and whether it is revised lower suggesting further easing towards stimulatory territory as excess capacity persists.

MNI BANK INDONESIA PREVIEW - AUGUST 2025: BI to Watch & Wait

Bank Indonesia (BI) cut rates 25bp at its July meeting but is likely to leave them at 5.25% on August 20. It holds monthly meetings and so has the flexibility to choose its timing for further easing, especially given that inflation remains around the mid-point of its 1.5-3.5% target band and Q2 growth was slightly stronger than expected. BI is likely to maintain its gradual approach and monitor the Fed, rupiah, global developments, the transmission of its previous 100bp of cuts and the domestic economy, while maintaining its easing bias. With four meetings left after this one, at least one more cut before end-2025 is highly likely.

DATA

AUSTRALIA DATA (MNI): Sentiment Improving Towards Neutral as Real Incomes Rise

Westpac's consumer confidence is trending towards the breakeven 100-level. Sentiment rose 5.7% m/m to 98.5 in August, the highest since February 2022, before the last tightening cycle began. The RBA's third rate cut this year on August 12 helped to boost confidence but the improvement was not just seen amongst mortgage holders. Governor Bullock also pointed out that further easing is consistent with inflation at the target mid-point.

CHINA DATA (MNI): China Youth Unemployment Reaches 12-Month High

MNI (Beijing) China’s urban unemployment rate for 16-24 year olds reached 17.8% in July, up from 14.5% in June, the highest reading in 12 months, National Bureau of Statistics data showed on Tuesday. Urban unemployment for 25–29 and 30–59 year olds was 6.9% and 3.9%, versus 6.7% and 4.0% the previous month.

FOREX: Coalition of the Willing Set to Discuss Structure of Security Guarantees

- Following yesterday's drift into the Monday close, EUR/USD is higher early Tuesday, but the recent range is being largely respected. Near-term focus remains on the tentative progress made at the meeting between President Trump, European leaders and Ukraine's Zelenskyy in the Oval Office yesterday. The so-called 'coalition of the willing' is now due to be holding conferences later today, at which the topic of security guarantees is highly likely to be discussed. The shape and structure of these guarantees could have a material impact on the sustainability of any peace deal or ceasefire.

- Following yesterday's sharp gains for the UK yield curve, GBP still appears fragile. GBPUSD has pulled back from its latest highs but a bull cycle remains intact. Recent gains resulted in a breach of resistance at 1.3589, the Jul 24 high. Sights are on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1.

- The Canadian inflation print is set for release later today, at which markets expect core CPI to tick higher on a trimmed mean basis to 3.1% from 3.0% - a release that should again feed into the October rate decision pricing - which currently sits close to 50/50 on the potential for a 25bps cut. Ahead of the print, USD/CAD remains toward the top-end of the recent range, with the 1.3831 level the short-term bull trigger. Clearance here puts the price at the best level since early August.

- Outside of the Canadian inflation print, US housing starts and building permits are due for release. Fed's Bowman is set to speak again, with broader focus still on Powell's appearance at Jackson Hole later in the week.

BONDS: 10-Year Gilt/Bund Spread Consolidates Yesterday’s Widening

The 10-year Gilt/Bund spread has broadly consolidated yesterday’s widening, currently 1bp narrower on the session at 196bps. The 200bp handle presents initial resistance for the spread, which will be in focus if UK CPI is higher-than-expected tomorrow morning.

- 10-year Gilt yields were unable to push above 4.75%, currently -1bp at 4.73%. The 4.80% handle presents a key near-term resistance. Yesterday’s selloff appeared to be due to ongoing concerns around the UK’s fiscal outlook, coupled with hawkish-leaning BOE signals since the August decision.

- German yields are up to 0.5bps higher across the curve, with the 2.80% handle presenting initial resistance for the 10-year. 30-year yields briefly reached a fresh multi-year high of 3.362% earlier. For now, the 103bp handle has capped upside in the German 5s30s curve.

- 2.20% Oct-30 Bobl supply saw stronger results than the previous re-opening.

- EU-bonds underperform Bunds, after Bloomberg reported overnight that ICE will not include EU-wide joint debt in its sovereign bond indices. 10-year spreads are 2.5bps wider today at ~31.5bps, with other EGB spreads to Bunds up to 1bp tighter on the session.

- In futures, Gilts are +6 ticks at 90.65, off earlier session lows of 90.43. Bunds are +9 ticks at 128.92. Bearish technical conditions remain in play for both contracts.

- The Eurozone June current account surplus widened to E35.8bln (vs E31.8bln prior).

- The remainder of today’s Eurozone/UK calendar is light, while Russia/Ukraine headline flow is still being monitored. The UK ONS has announced a delay to Friday’s retail sales release.

EQUITIES: Eurostoxx 50 Futures Remain Close to Recent Highs

A bullish theme in Eurostoxx 50 futures remains intact and the contract is trading closer to its latest highs. The print above the May and July highs strengthens a bull theme and signals scope for a climb towards 5575.00, the Mar 3 high (cont) and key resistance. Moving average studies remain in a bull-mode position, highlighting an uptrend. Support to watch lies at 5349.70, the 50-day EMA. The dominant uptrend in S&P E-Minis remains intact and the contract is trading at its recent highs. Moving average studies are in a bull-mode position, highlighting a clear uptrend. A resumption of gains would pave the way for a climb towards 6523.63, a Fibonacci projection. On the downside, supports to watch are; 6399.62, the 20-day EMA, and 6275.78, the 50-day EMA.

- Japan's NIKKEI closed lower by 168.02 pts or -0.38% at 43546.29 and the TOPIX ended 4.33 pts lower or -0.14% at 3116.63.

- Elsewhere, in China the SHANGHAI closed lower by 0.739 pts or -0.02% at 3727.288 and the HANG SENG ended 53.95 pts lower or -0.21% at 25122.9.

- Across Europe, Germany's DAX trades higher by 46.78 pts or +0.19% at 24362.06, FTSE 100 higher by 15.81 pts or +0.17% at 9173.73, CAC 40 up 43.98 pts or +0.56% at 7927.86 and Euro Stoxx 50 up 24.22 pts or +0.45% at 5458.94.

- Dow Jones mini down 5 pts or -0.01% at 44981, S&P 500 mini down 6 pts or -0.09% at 6463.5, NASDAQ mini down 21.75 pts or -0.09% at 23776.75.

Time: 10:00 BST

COMMODITIES: Moving Average Studies for Gold Remain in Bull-Mode Position

WTI futures remain in a clear bear cycle and the contract is trading closer to its recent lows. A key support at $61.99, the Jun 30 low, has been breached, strengthening a bearish theme. A continuation lower would open $57.71, the May 30 low. Key short-term resistance has been defined at $69.36, the Jul 30 high. Clearance of this level would cancel a bear theme. Initial resistance to watch is $64.00, the 50-day EMA. A bull cycle in Gold remains intact and this is highlighted by moving average studies that remain in a bull-mode position. The sideways trend that has been in place since the Apr peak appears to be a corrective phase - a pause in the uptrend. A resumption of gains would open $3439.0, the Aug 23 high. Key resistance and the bull trigger is at $3500.1, the Apr 22 low. On the downside, first support to watch lies at $3268.2, the Jul 30 low.

- WTI Crude down $0.59 or -0.93% at $62.79

- Natural Gas down $0.02 or -0.55% at $2.874

- Gold spot up $6.16 or +0.18% at $3338.61

- Copper up $0.8 or +0.18% at $454.4

- Silver up $0.04 or +0.1% at $38.053

- Platinum up $15.02 or +1.13% at $1345.32

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 19/08/2025 | 1230/0830 | *** | CPI | |

| 19/08/2025 | 1230/0830 | *** | Housing Starts | |

| 19/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 19/08/2025 | 1810/1410 | Fed Vice Chair Michelle Bowman | ||

| 20/08/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 20/08/2025 | 2301/0001 | * | Brightmine pay deals for whole economy | |

| 20/08/2025 | 2350/0850 | * | Machinery orders | |

| 20/08/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 20/08/2025 | 0600/0700 | *** | Consumer inflation report | |

| 20/08/2025 | 0600/0800 | ** | PPI | |

| 20/08/2025 | 0710/0910 | ECB Lagarde at WEF Intl Business Council | ||

| 20/08/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 20/08/2025 | 0900/1100 | *** | HICP (f) | |

| 20/08/2025 | 0900/1100 | Q2 Flash Vacancies and Labour Cost Index | ||

| 20/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 20/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 20/08/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 20/08/2025 | 1500/1100 | Fed Governor Christopher Waller | ||

| 20/08/2025 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 20/08/2025 | 1800/1400 | FOMC Minutes | ||

| 20/08/2025 | 1900/1500 | Atlanta Fed's Raphael Bostic |