MNI US OPEN - Tariff Relief Rally Begins to Fade

EXECUTIVE SUMMARY:

- RISK RALLY FALTERS, USD ERASES TRUMP-LED RECOVERY

- CHINA LEADERS TO MEET ON STIMULUS, PBOC RATE CUT SPECULATION RISES

- RUSSIA-US HOLDS TALKS ON RESUMING TIES IN ISTANBUL

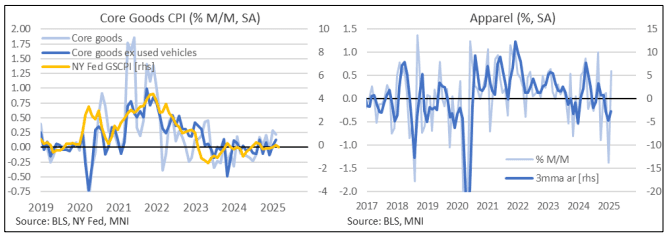

- US CPI WATCHED FOR INITIAL TARIFF PASSTHROUGH

Figure 1: Core Goods CPI in focus for March

NEWS

MNI US CPI Preview: Watching Initial Tariff Passthrough

We have published and e-mailed to subscribers the MNI US CPI Preview for today's release. Please find the full report including MNI analysis and a wide range of analyst expectations here: https://media.marketnews.com/USCPI_Prev_Apr2025_de0699a656.pdf

Minneapolis Fed President Neel Kashkari said Wednesday he doesn't want to see the U.S. central bank intervene in markets, adding that recent gyrations have been driven by economic fundamentals. "With the Fed, we don't want to intervene in markets. We wanna let markets correct themselves. There have been some pressures in markets in recent days. And in my judgment, those pressures are born by economic fundamentals," Kashkari said in an interview with CBS News.

China’s top leaders are poised to meet Thursday to discuss additional economic stimulus after US President Donald Trump ratcheted up tariffs, according to people familiar with the matter. The ad-hoc meeting is set to focus on support measures for housing, consumer spending and technological innovation, said the people, asking not to be identified discussing a private matter. Other government bodies, including financial regulators, are also convening to discuss steps to boost the economy and stabilize the markets, the people said. The schedule could still change, they added.

A Chinese state newspaper suggested it’s time to ease monetary policy to support the economy as rising trade tensions with the US threaten its growth outlook. The Securities Daily published a front-page commentary on Thursday saying it is an appropriate time for the Chinese central bank to cut interest rates and banks’ reserve requirement, a sign Beijing may soon move to offset headwinds brought on by soaring tariffs.

Taiwan is planning a surge in US purchases over the next decade that would triple the share of American liquefied natural gas in the island’s mix. State-operated entities could buy goods worth $200 billion from the US over the next 10 years, Minister of Economic Affairs Kuo Jyh-Huei said Thursday, according to a report from Taipei-based Economic Daily News. The purchases would include boosting the share of US LNG in Taiwan’s total imports to 30% from current levels around 10%, he said.

Yvette Cooper, the home secretary, said that Trump’s climbdown reinforces the UK’s strategy of being “pragmatic” rather than getting “buffeted around from day to day”. She told BBC Radio 4’s Today programme: “We don’t want to see a trade war and we will continue to take a calm, steady approach to this and negotiate in the UK’s interests.

China and the EU will immediately start negotiations on price commitment on Chinese EVs and discuss investment cooperation of the automotive industry, according to a statement on the Ministry of Commerce website Thursday, citing a video conference between Commerce Minister Wang Wentao and European Commissioner for Trade and Economic Security Maroš Šefčovič held on April 8.

Russia and the US on Thursday started a new round of talks aimed at normalizing diplomatic relations in Turkey’s Istanbul, even amid a lack of apparent progress in separate negotiations on ending the invasion of Ukraine. The talks will focus on restoring the two countries’ diplomatic missions as well as direct flights between the two nations that Washington suspended after Russia’s February 2022 invasion of Ukraine. The war in Ukraine is not on the agenda.

Australia has swiftly turned down China's offer to "join hands" against Donald Trump's tariffs, as Washington escalates its trade war with Beijing. China's ambassador to Australia Xiao Qian argued joint resistance is "the only way" to stop the "hegemonic and bullying behaviour of the US", appealing for Canberra's cooperation in an opinion piece on Thursday. Prime Minister Anthony Albanese, however, said Australians would "speak for ourselves", while the country's defence minister said the nation would not be "holding China's hand".

The Philippine central bank cut its key interest rate and signaled further monetary policy easing this year, moving to support confidence and growth as markets are whipsawed by changing US plans to impose global tariffs. The Bangko Sentral ng Pilipinas cited a challenging external environment as it reduced its target reverse repurchase rate by 25 basis points to 5.5% on Thursday, a move seen by 26 of 28 economists in a Bloomberg survey. Two predicted it would extend a pause in easing.

MNI discusses the U.S. tariff impact on the BOJ's hiking strategy. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

MNI discusses the RBA's May strategy and beyond. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

DATA

MNI: ITALY FEB INDUSTRIAL PRODUCTION -0.9% M/M; JAN 2.5%

ITALY FEB INDUSTRIAL PRODUCTION -2.7% Y/Y; JAN -0.8%

China's Consumer Price Index fell 0.1% y/y in March, narrowing from February's 0.7% decline but missing the expected +0.1%, data from the National Bureau of Statistics showed on Thursday. CPI fell 0.4% m/m, following February's 0.2% decline, the Bureau added. However core CPI, excluding food and energy prices, rose 0.5% y/y, reversing the previous decline of 0.1%, due to policies to boost consumer demand.

GILTS: Early Curve Flattening Holds, Uncertainty Lingers

Long end outperformance intact on the day, yields 1bp higher to 16bp lower, aggressive curve flattening unwinds a fair amount of yesterday’s steepening.

- 5s30s ~12bp flatter at ~124bp, after registering the highest close since ’17 on Wednesday. 2s10s ~11bp flatter at ~67bp after respecting the ’21 closing highs.

- Relative front end weakness has been driven by hawkish BoE repricing after U.S. President Trump delayed the imposition of reciprocal tariffs on most countries (China being the exception, given its retaliation).

- Meanwhile, long end gilts recover further from yesterday’s lows, after being pressured by what felt like deleveraging and ongoing worry surrounding the UK’s fiscal situation in the early part of Wednesday afternoon.

- Futures +84 at 91.54.

- Initial support and resistance defined at yesterday’s low (89.99) and the 20-day EMA (91.99), respectively. The longer run bearish technical setup remains in place.

- GBP STIRs comfortably off hawkish session extremes as geopolitical and tariff uncertainty persists, despite yesterday’s U.S. tariff delay.

- BoE-dated OIS 5-8bp more hawkish on the day.

- 22.5bp of cuts priced for May, 32bp showing through June and 76.5bp priced through year end (~80bp was priced through December at yesterday’s close).

- SONIA futures -7.5 to +7.5, strip flattens. October highs remained intact across most of the strip during the rally seen in recent sessions.

- BoE’s Breeden will appear at an MNI event from 14:00 London, speaking on the topic of ‘UK economic and Financial Stability prospects’.

EGBS: Bund Futures Recover From Post-Settlement Lows As Equities Fade

Bund futures have retraced ~60% of yesterday’s post settlement sell-off, with European equities fading some of the tariff delay-induced rally. Currently -82 ticks at 129.75, yesterday’s low at 128.60 provides initial support, with resistance seen at 130.32 (50.0% retracement of the Apr 7 - 9 pullback).

- The German curve has bear flattened, with Schatz yields up 11.5bps to 1.84% as markets trim 2025 ECB easing expectations. A 25bp April cut remains ~90% implied by OIS though.

- ASWs vs. 3-month Euribor are 4.0-5.5bp lower on the day, with Schatz spreads leading.

- The fade in risk sees 10-year peripheral/semi-core spreads to Bunds move away from earlier lows, with the BTP/Bund spread currently 8bps tighter today at 121bps (vs a ~116bp opening low).

- Spain sold the top of its target range at today’s Bono/Obli auction (E6.457bln vs E5.5-6.5bln target), with mixed results seen across lines.

- US CPI headlines today’s macro data calendar, but markets will continue to exhibit sensitivity to any tariff-related developments.

FOREX: Risk Rally Lacks Follow-Through, USD Lower

- Unsurprisingly, European equities shot higher at the cash equity open Thursday, mimicking the record-setting Wednesday close on Wall Street. Markets have faded off highs, but are still maintaining a considerable rally on Trump's U-turn yesterday. US policy uncertainty remains well-elevated, with the US policy uncertainty index remaining at elevated levels, which continues to undermine the USD.

- The USD's initial rally has all but reversed, leaving EUR/USD at pre-U-turn levels. It is notable that the pair yesterday did not reverse as materially as equities did following the tariff pullback - which may be a strong signal that markets continue to discount the USD vs prior, pre-Liberation Day valuations, and that while tariff policy may have reversed, the implications for inflation and growth in the US this year persist.

- From a technical perspective, the trend condition in EURUSD is unchanged and remains bullish. Sights are on 1.1188 next, a Fibonacci projection. Initial firm support lies at 1.0854, the 20-day EMA.

- US CPI data is a focus going forward - although the risk premia surrounding the event have fallen notably since the tariff relief late yesterday. Markets expect 0.1% M/M, 2.5% Y/Y, but slightly higher prints in the core metrics.

- Several Fed speakers are set to make appearances Thursday: Fed's Logan, Schmid, Goolsbee and Harker are due, while the Senate are due to hold hearings on Bowman's nomination as the Fed's top banking supervisor.

EQUITIES: Volatility Clouds Technical Picture

A short-term reversal in S&P E-Minis yesterday highlights the start of what appears to be a corrective cycle. The trend condition has been oversold following recent weakness and the move higher is allowing this set-up to unwind. Eurostoxx 50 futures have traded in an extremely volatile manner and rallied sharply higher from this week’s lows. The climb highlights the start of a corrective cycle and if this is correct, marks an unwinding of the recent oversold trend condition.

- Japan's NIKKEI closed higher by 2894.97 pts or +9.13% at 34609 and the TOPIX ended 190.07 pts higher or +8.09% at 2539.4.

- Elsewhere, in China the SHANGHAI closed higher by 36.828 pts or +1.16% at 3223.638 and the HANG SENG ended 417.29 pts higher or +2.06% at 20681.78.

- Across Europe, Germany's DAX trades higher by 1019.08 pts or +5.18% at 20696.08, FTSE 100 higher by 298.6 pts or +3.89% at 7978.84, CAC 40 up 347 pts or +5.06% at 7210.2 and Euro Stoxx 50 up 245.86 pts or +5.32% at 4867.93.

- Dow Jones mini down 644 pts or -1.58% at 40196, S&P 500 mini down 105 pts or -1.91% at 5387.25, NASDAQ mini down 429.5 pts or -2.23% at 18861.75.

COMMODITIES: Trend Condition for Gold Remains Bullish

The trend condition in Gold remains bullish and the latest pull back appears to have been a correction. Moving average studies are unchanged, they remain in a bull-mode position highlighting a dominant uptrend. A bearish theme in WTI futures remains intact and yesterday’s rally from the day low is - for now - considered corrective. The move higher is allowing an oversold trend condition to unwind. Recent weakness has resulted in the breach of a number of important support levels.

- WTI Crude down $2.06 or -3.3% at $60.27

- Natural Gas down $0.12 or -3.25% at $3.692

- Gold spot up $26.36 or +0.86% at $3108.85

- Copper up $15.45 or +3.69% at $434.7

- Silver down $0.07 or -0.23% at $30.9595

- Platinum up $0.93 or +0.1% at $937.27

| Date | GMT/Local | Impact | Country | Event |

| 10/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 10/04/2025 | 1230/0830 | * | Building Permits | |

| 10/04/2025 | 1230/0830 | *** | CPI | |

| 10/04/2025 | 1300/1400 | BoE's Breeden at MNI Connect ‘UK economic and Financial Stability prospects’ | ||

| 10/04/2025 | 1330/0930 | Dallas Fed's Lorie Logan | ||

| 10/04/2025 | 1400/1000 | Kansas City Fed's Jeff Schmid | ||

| 10/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 10/04/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 10/04/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 10/04/2025 | 1600/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/04/2025 | 1600/1200 | Chicago Fed's Austan Goolsbee | ||

| 10/04/2025 | 1630/1230 | Philly Fed's Pat Harker | ||

| 10/04/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 10/04/2025 | 1800/1400 | ** | Treasury Budget | |

| 10/04/2025 | 2000/1600 | Boston Fed's Susan Collins | ||

| 11/04/2025 | 2301/0001 | ** | KPMG/REC Jobs Report | |

| 11/04/2025 | 0600/0700 | ** | UK Monthly GDP | |

| 11/04/2025 | 0600/0800 | *** | Final Inflation Report | |

| 11/04/2025 | 0600/0700 | ** | Trade Balance | |

| 11/04/2025 | 0600/0700 | ** | Index of Services | |

| 11/04/2025 | 0600/0700 | *** | Index of Production | |

| 11/04/2025 | 0600/0800 | *** | HICP (f) | |

| 11/04/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 11/04/2025 | 0700/0900 | *** | HICP (f) | |

| 11/04/2025 | 0945/1145 | ECB's Lagarde at Eurogroup Press Conference | ||

| 11/04/2025 | - | *** | Money Supply | |

| 11/04/2025 | - | *** | New Loans | |

| 11/04/2025 | - | *** | Social Financing | |

| 11/04/2025 | - | BoE's Saporta on 'How financial crisis reshape market and strategies’ | ||

| 11/04/2025 | 1230/0830 | *** | PPI | |

| 11/04/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 11/04/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 11/04/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 11/04/2025 | 1500/1100 | New York Fed's John Williams | ||

| 11/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 11/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |