MNI US OPEN - Russia, US Delegations Discussing Ceasefire

EXECUTIVE SUMMARY

- WHITE HOUSE NARROWS APRIL 2 TARIFFS

- RUSSIA AND US TEAMS MEET AFTER UKRAINE HOLDS ‘PRODUCTIVE’ TALKS

- BOJ UCHIDA SEES NEED TO RAISE RATE ON PRICE MOVES

- TURKISH TRADERS BRACE FOR MORE VOLATILITY AFTER IMAMOGLU ARREST

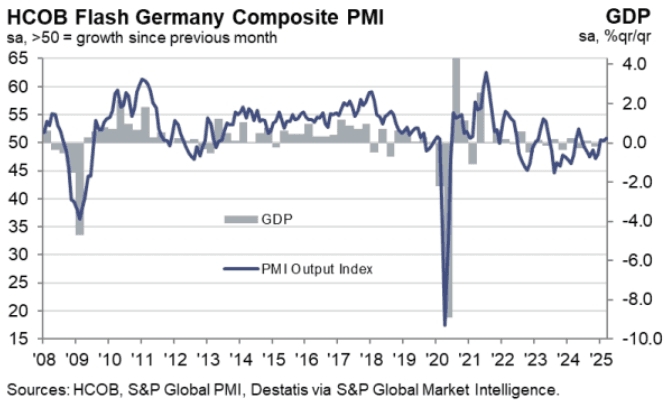

Figure 1: Manufacturing Buoys Germany Composite PMI, But Services Weak

NEWS

US (WSJ): White House Narrows April 2 Tariffs

The White House is narrowing its approach to tariffs set to take effect on April 2, likely omitting a set of industry-specific tariffs while applying reciprocal levies on a targeted set of nations that account for the bulk of foreign trade with the U.S. President Trump has declared his April 2 deadline to be “Liberation Day” for the U.S., when he will put in place so-called reciprocal tariffs that seek to equalize U.S. tariffs with the duties charged by trading partners, as well as tariffs on sectors like automobiles, pharmaceuticals and semiconductors he repeatedly said would be enacted on that day. Those sector-specific tariffs, however, are now not likely to be announced on April 2, said an administration official, who said the White House is still planning to unveil the reciprocal tariff action on that day, though planning remains fluid.

US/RUSSIA (BBG): Russia and US Teams Meet After Ukraine Holds ‘Productive’ Talks

US and Russian officials are meeting in Saudi Arabia a day after American and Ukrainian teams held talks, as President Donald Trump pushes for progress in achieving a ceasefire in the war. The Russian delegation arrived at the venue on Monday for the closed-door talks with the US in the Saudi capital Riyadh, Russia’s Tass news service reported. It’s led by former Deputy Foreign Minister Grigory Karasin and Sergei Beseda, an adviser to the head of the Federal Security Service in Moscow, the agency said.

US/CHINA (BBG): Xi Must Stop Fentanyl Flow Before Tariff Talks, Trump Ally Says

An American senator said China must halt the flow of fentanyl ingredients into the US before any trade negotiations, a demand that clouds the prospect of imminent leaders’ talks to ease tensions between the world’s two largest economies. Steve Daines, a close ally of President Donald Trump, laid out the condition in meetings with Chinese officials in Beijing over the weekend. The Republican lawmaker said he hopes a leadership meeting will take place before the end of the year, although Trump previously said it would happen soon.

US/CHINA (MNI): China Trade Leader Meets Apple’s Cook in Beijing

MNI (Beijing) The China Council for the Promotion of International Trade's President Ren Hongbin has met with Apple CEO Tim Cook in Beijing, the council announced on Monday. Ren said authorities were confident of achieving this year's economic growth target of around 5%, and would provide Apple and other foreign-funded enterprises with broader market opportunities. Cook said Apple was willing to contribute to stable Sino-U.S. relations.

CANADA (MNI): Mark Carney Calls Snap Canada Election for April 28

Mark Carney on Sunday called a snap election for April 28, with the former BOC and BOE Governor seeking a seat for himself in Parliament and a mandate for his Liberals to negotiate tariffs with Donald Trump. Carney called the vote about a week after taking over from Justin Trudeau as prime minister following a party leadership race. The move comes the day before Parliament was due to re-open with opposition parties saying they would have passed a non-confidence motion forcing an early election before one due in October.

ECB (MNI): Reasons to Keep Cutting “Reinforced” - ECB Cipollone

Developments and new data since the March Governing Council meeting have reinforced the argument for the European Central Bank to continue cutting interest rates, ECB executive board member Piero Cipollone said in an interview with Expansion published Monday. The recent fall in energy prices and the appreciation of the euro, along with the recent rise in borrowing costs at the longer-end of the yield curve erase inflation concerns from the last ECB projections round, “with the information we have makes likely that inflation target gets hit before the projections,” he said.

UK (FT): New Poll Shows Risks for Keir Starmer Over Spending Choices

A clear majority of Labour voters believe welfare spending is more important than boosting the UK defence budget, according to new polling, highlighting the political challenge facing Sir Keir Starmer as he makes the case for rearmament. The exclusive polling conducted ahead of Wednesday’s Spring Statement also revealed that voters of all parties think the government can increase spending while cutting taxes.

CHINA (BBG): PBOC to Auction $62 Billion One-Year Loans to Banks on Tuesday

China’s central bank will inject 450 billion yuan ($62 billion) of liquidity into the market via its one-year loans in a new method that allows banks to bid for the loan on different prices. The People’s Bank of China announced the new method to auction the medium-term lending facility starting from this month in a statement Monday. It will conduct an operation of one-year MLF worth 450 billion yuan on Tuesday, it said.

CHINA (MNI): PBOC Sees RRR Cut, Asset Prices Stressed

MNI (Beijing) The People's Bank of China sees room for further reductions to the reserve requirement ratio and will focus monetary policy on safeguarding asset prices, said Li Yang, chairman of National Institution for Finance and Development, during the China Development Forum on Sunday. China’s monetary policy retains flexibility based on room for an RRR cut, he added, noting 1 percentage point of easing will unlock CNY2 trillion in liquidity.

CHINA (MNI): China to Enhance Efforts for Eco Recovery - Li

MNI (Beijing) China will enhance policy efforts to achieve “around 5%” GPD target in 2025 and introduce additional supportive measures when necessary to bolster sustained and stable economic recovery, said Premier Li Qiang on Sunday at the China Development Forum. Authorities will implement more proactive policies and intensify counter-cyclical moves, Li said, adding the country will remain steadfast in advancing economic opening, advocating for fair competition under internationally recognised rules, upholding free trade and ensuring the stability and smooth operation of global industrial and supply chains.

BOJ (MNI): BOJ Uchida Sees Need to Raise Rate on Price Moves

Bank of Japan Deputy Governor Shinichi Uchida said on Monday that the BOJ will raise the policy interest rate to adjust the degree of easy policy if the economy and prices move in line with the bank’s forecasts. Uchida told lawmakers that the BOJ will manage its monetary policy in an appropriate manner to achieve the 2% target in a stable and sustainable manner, while examining price moves and risks. He added that it is appropriate for foreign exchange rates to move in a way that reflect economic fundamentals stably.

BOJ (MNI): BOJ Will Sell JGBs if Needed - Ueda

Bank of Japan Governor Kazuo Ueda said on Monday the Bank could sell Japanese government bonds if necessary, but did not elaborate further. When asked about the risk of rapid inflation, Ueda told lawmakers that the BOJ continues to pay attention to price moves and various risks, and the bank will manage monetary policy appropriately to avoid falling behind the curve. He said that the BOJ believed there was no overheated activity in financial and asset markets.

JAPAN (FT): Japan Has Not Yet Conquered Deflation, Finance Minister Warns

Japan has not yet beaten deflation despite years of persistently rising consumer prices and the largest round of annual wage increases in three decades, the country’s finance minister has warned. Katsunobu Kato’s blunt assessment in an interview with the Financial Times comes 15 months into the Bank of Japan’s efforts to “normalise” the economy and gradually reintroduce positive interest rates, after a quarter-century-long battle to steer the country away from falling prices.

AUSTRALIA (BBG): Australia’s Job Market Is Still Tight, RBA Disclosure Shows

Australia’s labor market remains tight while the gap between the level of overall demand in the economy and its capacity to supply is narrowing, according to a Freedom of Information disclosure published by the Reserve Bank on Monday. The RBA released internal documents showing its model average estimate of NAIRU - the lowest jobless rate that can be sustained without triggering faster inflation - decreased to 4.69% in March, from 4.75% in February. The decline reflects a surprisingly resilient labor market where unemployment has hovered around 3.9-4.2% over the past year. It held at 4.1% in February.

S. KOREA (NYT): South Korean Court Reinstates Impeached Premier as Acting President

The legislature impeached Han Duck-soo in December, soon after impeaching President Yoon Suk Yeol for declaring martial law. Mr. Yoon’s fate is still unclear. Prime Minister Han Duck-soo of South Korea was restored to office as acting president on Monday, after the country’s Constitutional Court overturned his impeachment by the National Assembly. But the ruling did little to herald any political stability in the country, which has lurched from crisis to crisis.

TURKEY (BBG): Turkish Traders Brace for More Volatility After Imamoglu Arrest

Turkish markets began the week on edge as the cost of borrowing lira and insuring the country’s debt against default stuck near their recent highs after the formal arrest of President Recep Tayyip Erdogan’s main political rival over the weekend. Authorities scrambled to shore up the nation’s assets, with Treasury and Finance Minister Mehmet Simsek meeeting with regulators on Sunday, and the central bank in contact with lenders over last week’s market turmoil - which was sparked by the detention of Istanbul Mayor Ekrem Imamoglu on corruption charges.

DATA

EUROZONE DATA (MNI): Continued Convergence of Manuf PMI Outcomes

- EZ MARCH FLASH MANUF PMI 48.7 (FCAST 48.2, FEB 47.6)

- EZ MARCH FLASH SVCS PMI 50.4 (FCAST 51.1, FEB 50.6)

The Eurozone-wide manufacturing PMI saw a small beat at 48.7 (vs 48.2 cons, 47.6 prior). Our calculations imply the average ex-France and Germany manufacturing PMI was between 48.9-49.1 (vs 49.2 in February). This suggests a continued convergence of outcomes between the two-largest economies and the rest of the Eurozone. Services was confirmed to be weaker-than-expected following the German reading, printing at 50.4 (vs 51.1 cons, 50.6 prior). This suggests an average ex-France and Germany PMI of 53.3-53.4 (vs 53.9 prior) - implying continued outperformance relative to the two largest economies in the bloc.

GERMAN DATA (MNI): Manufacturing Buoys Composite, But Services Weak

- GERMANY FLASH MARCH MANUF PMI 48.3 (FCST 47.0, FEB 46.5)

- GERMANY FLASH MARCH SVCS PMI 50.2 (FCST 52.0, FEB 51.1)

The German services PMI fell to its lowest since November at 50.2 (vs 52.0 cons, 51.1 prior), but this was slightly offset by the strongest manufacturing reading in 31 months (48.3 vs 47.0 cons, 46.5 prior). This helped the composite reading reach a 10-month high of 50.9 (vs 51.1 cons, 50.4 prior). Despite this, the details of the PMI screen dovish - particularly for services, which accounts or ~70% of gross value added in Germany. Underlying services demand remains weak, while both input cost and output charge inflation cooled in March.

FRANCE DATA (MNI): Manufacturing Shows Tentative Signs of Recovery

The French March flash manufacturing PMI was notably stronger-than-expected at 48.9 (vs 46.1 cons, 45.8 prior), the strongest reading since January 2023. Services also fared better than-expected at 46.6 (vs 46.0 cons, 45.3 prior), but did not fully recoup the fall from January's 48.2. Although the PMIs signal tentative signs for a recovery in the manufacturing industry, the details of report continue to display weak underyling economic conditions in both surveyed sectors. The deterioration of 12-month ahead confidence suggests little spillover from the recent step change in the German/European fiscal and defence policy complex.

UK DATA (MNI): Diverging Services and Manufacturing PMIs; More Focus on Goods CPI

- UK FLASH MARCH MANUF PMI 44.6 (FCAST 47.2, FEB 46.9)

- UK FLASH MARCH SERVICES PMI 53.2 (FCAST 51.0, FEB 51.0)

In contrast to the EZ, the UK flash services PMI surprises to the upside at 53.2 (51.0 exp and prior). Also in contrast the flash manufacturing PMI surprises to the downside. There is also a decent upside surprise to the flash composite PMI. A real contrast between the sectors here with services seeing overseas demand while manufacturers are impacted by global economic uncertainty and tariff concerns. The other big point to pick out here is that both services and manufacturers are noting costs being passed on from higher payroll costs and NIC contributions. This allies with the MPC Minutes on Friday - and adds to evidence that whereas 2024 was dominated largely by services inflation, in 2025 non-energy goods inflation will be watched much more closely too.

FOREX: JPY Slipping as Tariffs Seen Targeted

- JPY is slipping against all others in G10 early Monday, with a more solid turn-out for European equities leading the JPY lower. USD/JPY attempted a break of the Y150.00 handle in Asia-Pac trade, but failed on the approach, with tariff tumult still the key underlying driver of markets.

- Reports over the weekend that the White House are aiming for a more targeted approach to reciprocal tariffs on next week's 'Liberation Day' has helped support risk, and the gap higher for US equity futures at the resumption of trade was followed by core US yields, although the US Dollar has failed to benefit headed into the NY crossover.

- Scandi currencies outperform, with NOK and SEK both again higher. USD/NOK's print down at 10.4739 today was the lowest since September last year, extending the losing streak for the pair and narrowing the gap with the bear trigger at 10..3916.

- Preliminary PMI data from across Europe and the UK had relatively little impact on markets, with Eurozone data confirming the economy held just above a flatline across March - with the French contribution a particular weakpoint.

- Preliminary US PMI stats are the calendar highlight Monday, although central bank speakers are also in focus. Fed's Bostic & Barr are set to make appearances as well as BoE's Bailey, ECB's Escriva and RBA's Jones after-market.

EGBS: Weak German Services PMI Buoys Bunds, But Rallies Contained

Bund futures rallied after the German flash March services printed weaker-than-expected at 50.2 (vs 52.0 cons, 51.1 prior), a sign that underlying demand conditions remain subdued. Stronger-than-expected manufacturing prints in France and Germany capped upside though, with Bunds not able to close the opening gap at 128.48 (currently -11 ticks at 128.37). Beyond the opening gap, initial resistance in Bunds is the 20-day EMA at 128.83.

- Overnight weakness came on reports that US President Trump’s April 2 tariff announcement will be more targeted – as opposed to broad-based – than currently expected.

- German yields are up to 1bp higher on the session. The DFA has announced that there are no changes to auction sizes in Q2 for either capital markets or for Bubills. This was broadly as expected.

- Supply is due from the EU at 1030GMT, which will also be limiting rallies in Bunds.

- Earlier, ECB Executive Board member Cipollone provided characteristically dovish comments, suggesting the case for an April rate cut has grown.

- 10-year EGB spreads to Bunds are generally tighter on the session (BTP/Bund is 1.5bps tighter at 109.5bps), even as European equities move away from session highs. IRISH bonds underperform.

GILTS: Stronger-Than-Expected PMIs Limit Recovery Rally, Outperforming Bunds

Gilts move away from session highs after the firmer-than-expected flash UK Services PMI data, limiting a recovery from early session lows.

- Futures last +11 at 91.74 (91.23-91 range)

- Initial support and resistance located at 91.07/93.01, with the bearish technical theme in the contract intact.

- Yields 2-3bp lower across the curve, front end outperforms.

- 2s10s and 5s30s continue to respect psychological resistance levels at 50bp & 100bp, respectively.

- 10s ~2bp tighter to Bunds on the day. Little to explain the outperformance ahead of a raft of UK risk events, with gilts outperforming

- Comments from BoE’s Bailey are due this evening (18:00 GMT).

- A little further out, Wednesday will bring the release of the latest round of CPI data, the Spring Statement, gilt remit and OBR projections, while Friday will see the release of retail sales and final Q4 GDP.

- Local headline flow has focused on continued spending cuts in Whitehall and Chancellor Reeves stressing adherence to the fiscal rules, leaving spending cuts front and centre ahead of Wednesday.

- GBP STIRs have followed swings in the long end.

- BoE-dated OIS now shows 15bp of cuts for May, 19bp through June, 30bp through August and 46bp through year-end. Contracts are little changed to a couple of bp more dovish on the day.

- SONIA futures flat to +2.0.

EQUITIES: E-Mini S&P Starts the Week on a Firmer Note, But Trend Remains Bearish

Eurostoxx 50 futures continue to trade above their recent lows. The medium-term trend direction is up and the recent pullback is considered corrective. Support to watch is the 50-day EMA, at 5285.44. It has recently been pierced. A clear break of it would highlight a stronger short-term bear threat and suggest scope for a retracement towards 5160.00, the Feb 4 low. The bull trigger is 5516.00, the Mar 3 high. The trend condition in S&P E-Minis is bearish and the latest recovery appears corrective. Moving average studies are unchanged -they remain in a bear-mode set-up, highlighting a dominant downtrend. Sights are on 5483.50, a Fibonacci projection. Note that the short-term trend condition is oversold. Recent gains are allowing this set-up to unwind. Initial firm resistance to watch is 5801.77, the 20-day EMA. The bear trigger is 5559.75, Mar 13 low.

- Japan's NIKKEI closed lower by 68.57 pts or -0.18% at 37608.49 and the TOPIX ended 13.28 pts lower or -0.47% at 2790.88.

- Elsewhere, in China the SHANGHAI closed higher by 5.197 pts or +0.15% at 3370.028 and the HANG SENG ended 215.84 pts higher or +0.91% at 23905.56.

- Across Europe, Germany's DAX trades higher by 136.08 pts or +0.59% at 23025.14, FTSE 100 higher by 42.06 pts or +0.49% at 8689.88, CAC 40 up 35.66 pts or +0.44% at 8079.32 and Euro Stoxx 50 up 27.74 pts or +0.51% at 5451.71.

- Dow Jones mini up 329 pts or +0.78% at 42649, S&P 500 mini up 57.5 pts or +1.01% at 5775.75, NASDAQ mini up 247 pts or +1.24% at 20207.75.

Time: 08:50 GMT

COMMODITIES: Gold Holding Onto Recent Gains, Sights on $3079.20 Next

Despite holding on to its recent gains, a bearish condition in WTI futures remains intact and the latest recovery appears corrective. Key pivot resistance to watch is $69.12, the 50-day EMA. A resumption of the downtrend would signal scope for an extension towards $63.73 next, the Oct 10 ‘24 low. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A clear uptrend in Gold is intact and last week’s resumption of the bull cycle reinforces current conditions. The yellow metal is holding on to the bulk of its recent gains. Last Thursday’s fresh trend high reinforces the bull theme and sights are on $3079.2 next, a Fibonacci projection. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Support is at $2962.0, the 20-day EMA.

- WTI Crude down $0.2 or -0.29% at $68.15

- Natural Gas down $0.04 or -0.88% at $3.948

- Gold spot up $5.95 or +0.2% at $3027.73

- Copper up $6.7 or +1.31% at $517.9

- Silver up $0.23 or +0.71% at $33.27

- Platinum up $3.53 or +0.36% at $983.51

Time: 08:50 GMT

| Date | GMT/Local | Impact | Country | Event |

| 24/03/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/03/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/03/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 24/03/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 24/03/2025 | 1800/1800 | BOE's Bailey lecture on UK growth | ||

| 24/03/2025 | 1910/1510 | Fed Governor Michael Barr | ||

| 25/03/2025 | 0700/0800 | ** | PPI | |

| 25/03/2025 | 0800/0900 | ** | PPI | |

| 25/03/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 25/03/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 25/03/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 25/03/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 25/03/2025 | 1240/0840 | Fed Governor Adriana Kugler | ||

| 25/03/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 25/03/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 25/03/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 25/03/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 25/03/2025 | 1305/0905 | New York Fed's John Williams | ||

| 25/03/2025 | 1400/1500 | ** | BNB Business Confidence | |

| 25/03/2025 | 1400/1000 | *** | New Home Sales | |

| 25/03/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 25/03/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 25/03/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note |