MNI US OPEN: New UK Chancellor Statement Awaited

EXECUTIVE SUMMARY:

- MINI-BUDGET REVERSAL TO CONTINUE - MNI GILT WEEK AHEAD

- BOJ'S KUROADA SAYS KEEPING EASY POLICY APPROPRIATE

- CHINA DELAYS RELEASE OF ECONOMIC INDICATORS

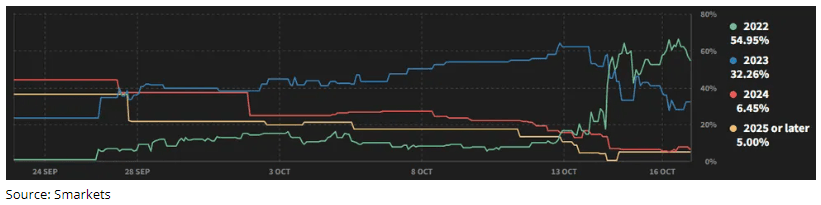

Figure 1: Betting Market Implied Probability of Year Liz Truss Leaves Office

NEWS

UK (MNI): MNI Gilt Week Ahead: Mini-Budget Reversal Continues

The Chancellor is due to make a statement this morning to row back further measures of the "Growth Plan" to provide financial stability ahead of the 31 October Medium-Term Fiscal Plan (11:00BST according to media reports).

The MNI Markets team expect gilt yields to remain high. Whatever happens from here investors will want to price an additional risk premium when assessing the value of gilts.

UK (MNI): 2022 Still Seen As Most Likely Exit Year For PM Truss By Bettors

Betting markets continue to assign a greater than 50% implied probability that PM Liz Truss leaves office in 2022, with data from Smarkets showing the figure for this year currently standing at 55.0%. This number has fallen from its weekend peak of 66.7%, but it appears bettors do not believe the replacement of chancellor with new man Jeremy Hunt and the anticipated reversal of nearly all mini-budget measures will be enough to save Truss from an imminent defenestration by her party.

UK (MNI): How could the energy price guarantee be tweaked?

There has been talk this morning of the government reversing some of the energy price guarantee. This is a very poorly targeted scheme and is applied universally. For households, it has capped the unit prices of gas to 10.3p/hWh and 34.0p/kWh for electricity (as well as capping the standing charge). This had the effect of limiting the average energy bill to 2,500/year for households.

However as energy unit prices are capped, those who are the heaviest energy users are effectively receiving the largest subsidy. The heaviest energy users tend to be the wealthiest with the largest houses - those who don't necessarily need the help of government subsidies. This also makes the scheme far more expensive than it really needs to be.

CHINA (MNI): Oct Releases Postponed, Including This Week's Q3 GDP

China's National Bureau of Statistics has delayed several key data releases due later in October, including Q3 GDP and home prices which had been due out Tuesday morning. No explanation for the postponements was provided, nor new release dates. It comes after the Customs General Administration delayed the release of trade data on Friday.

CHINA (MNI): China's Xi Pledges Reform, Eyes Domestic Demand Growth

China will expand domestic demand, improve global economic cooperation and implement further reforms as it strives for high-quality development and a reasonable growth rate over the next 15 years, President Xi Jinping told 3000 delegates during the opening ceremony of the 20th National Congress of the Chinese Communist Party in Beijing on Sunday.

China will accelerate the development of its “new development paradigm” built on the concept of "dual circulation", in which growth in domestic and overseas markets reinforce each other, with the domestic market expected to become the mainstay of growth. Development will also incorporate reforms of China socialist market economy and high-level opening up of the economy.

CHINA (MNI): Growth Recovering, Investment Welcome - NDRC

China's top economic planning agency, the National Development and Reform Commission, said the economy is recovering and will continue to open up and welcome foreign investment.

The NDRC told a 20th Party Congress press conference on Monday that economic indicators were showing upward momentum, highlighting "low inflation" and "stable" unemployment. "China’s economy has shown resilience in the face of the Covid and external factors and continues to recover”, Zhao Chenxin, Vice Chairman of the NDRC said.

JAPAN (MNI): BOJ's Kuroda Says Keeping Easy Policy Appropriate

Bank of Japan Governor Haruhiko Kuroda said on Monday that Japan’s core consumer price index will fall below a 2% year-on-year pace in fiscal 2023 and it’s appropriate for the bank to maintain easy policy to achieve its price stability target accompanied by wage hikes.

Kuroda told lawmakers at a Lower House budget committee that the year-on-year rise in core CPI will likely accelerate toward the end of this year due to rising import prices caused by high resource prices and the weak yen.

JAPAN (MNI): BOJ Wary of Slow China Recovery, Fed Hike Impact

Bank of Japan officials are worried about a slower recovery in the Chinese economy, seeing it as very unlikely that China will achieve its 5.5% growth target, MNI understands. However, they expect President Xi Jinping to use his authority to drive monetary and fiscal policies to boost economic growth, although BOJ officials cannot predict any specific economic growth outcomes.

NEW ZEALAND (MNI): Q3 CPI Preview: Underlying Inflation To Keep RBNZ Hawkish

NZ CPI for Q3 is published on Tuesday and is expected to rise 1.5%q/q (down from 1.7% in Q2), according to Bloomberg, but the range of forecasts is wide from 1.3% to 2.0%. The median would leave headline inflation at 6.6%y/y down from the Q2 32-year high of 7.3%, and past its peak. The expected easing in headline inflation is unlikely to be a reason to expect a more dovish RBNZ, as underlying inflation pressures probably didn't improve in Q3.

IRAN (MNI): EU's Borrell on Nuclear Deal - 'Don't Expect Any Moves'

Ahead of an EU Foreign Affairs Council meeting in Brussels, EU High Representative for Foreign Affairs Josep Borrell states that on the Iran nuclear deal that, "I don't expect any move. That's a pity because we were very, very, very close. We have to wait,"'. Pressure for increasing sanctions on Tehran growing as anti-regime protests and a subsequent gov't crackdown continue in Iran.

DATA

ITALY SEP HICP FINAL +9.4% Y/Y (FLSH 9.5%); AUG +9.1% Y/Y (MNI)

AUSTRALIA (MNI): Week To Be Dominated By RBA And Labour Market Data

- The focus of the week in Australia is likely to be RBA commentary and the September labour force report. On Tuesday, RBA Deputy Governor Bullock is scheduled to speak at the Australian Finance Industry Association annual conference at 11.05AEDT. This will be followed by the minutes from the October 4 RBA meeting. Given the surprise 25bp move, the minutes could be more on the dovish side and likely to be studied for more detail on the Board's reasoning.

- The MI/Westpac leading indicator for September is published on Wednesday. August marked the third consecutive fall and brought the 6-month annualised growth rate into negative territory for the first time since January. Further monetary tightening and the deteriorating global outlook are likely to weigh on the index again this month.

- September employment data is released on Thursday. Another moderate gain of 25k is expected after 33.5k last month, which should keep the unemployment rate steady at 3.5%. A result around this mark is unlikely to change the RBA's 25bp per meeting stance.

FOREX: GBP Supported Amid UK Turnaround, USDJPY Probes Cycle Highs

- Attention is on the UK today and this week with the UK CPI also release on Wednesday.

- Today, Jeremy Hunt will give a statement at 11.00BST, and will speak at the House of Commons at 15.30BST.

- Speculation of more U-Turn in the mini budget has benefited the Pound.

- Still the best performer against the USD in G10, up 0.90%.

- ALL EYES are also on the Yen this morning, and risk of more potential BoJ intervention.

- USDJPY is trading close to 148.86, Friday's high, which was also another multi decade high.

- So far, USDJPY has printed a 148.80 high.

- USD is in the red against all G10s, some unwound from the post US Michigan rallies.

- EURUSD trades within ranges this morning, but at the upper end, with Equities underpinned in early trade, in turn USD offered.

- There's 1.07bn option expiry in EURUSD at 0.9750/0.9765 for today.

- Cross assets and FX will be taking their cue from the UK.

- Looking ahead, besides Jeremy Hunt, there's no real notable data releases for the session.

- Speakers include, ECB de Cos, Lane and Nagel.

BOND SUMMARY: Gilts Lead the Way Ahead of Chancellor's Statement with Yields Down 30+bp

- Huge moves for gilts again this morning following an announcement that new Chancellor Jeremy Hunt will speak at 11:00BST / 6:00ET outlining more plans to backtrack on the government's "Growth Plan". Media reports note that everything apart from the reversal of the NIC hike is under discussion - including the energy support plan (our thoughts on how the latter could be tweaked are here). Yields are down in between 32-36bp across the entire gilt curve in response. After the Chancellor's morning statement, he will give more details in the Commons at 15:30BST / 10:30ET.

- Chinese data due tomorrow including Q3 GDP has been postponed with no explanation for the postponement announced.

- Bunds and to a lesser extent USTs are following gilts higher this morning.

- TY1 futures are up 0-14+ today at 111-01+ with 10y UST yields down -7.5bp at 3.946% and 2y yields down -5.6bp at 4.441%.

- Bund futures are up 1.43 today at 137.51 with 10y Bund yields down -12.2bp at 2.221% and Schatz yields down -8.0bp at 1.865%.

- Gilt futures are up 3.14 today at 968.86 with 10y yields down -31.8bp at 4.007% and 2y yields down -33.4bp at 3.536%.

EQUITIES: S&P E-minis Recovery Suggests Entering Corrective Phase

EUROSTOXX 50 futures traded in a volatile manner last week, rebounding sharply from 3251.00, the Oct 13 low. The strong recovery highlights a potential short-term reversal and if correct, the start of a bull cycle. The focus is on the 50-day EMA at 3473.30 and resistance at 3492.00, the Oct 6 high. A break of this zone would strengthen a bullish case. On the downside, the key support zone to watch is at 3251.00-3236.00. A volatile session last Thursday in S&P E-Minis resulted in a strong bounce from the day low as well as the trend low of 3502.00. The recovery suggests that the contract has entered a corrective phase and if correct, this will allow an oversold trend condition to unwind. Attention is on 3724.56, the 20-day EMA. A break would reinforce a bullish theme and open 3820.00, the Oct 5 high. Key support and the bear trigger lies at 3502.00.

- Japan's NIKKEI closed lower by 314.97 pts or -1.16% at 26775.79 and the TOPIX ended 18.63 pts lower or -0.98% at 1879.56.

- Elsewhere, in China the SHANGHAI closed higher by 12.955 pts or +0.42% at 3084.942 and the HANG SENG ended 25.21 pts higher or +0.15% at 16612.9.

- Across Europe, Germany's DAX trades higher by 58.79 pts or +0.47% at 12496.84, FTSE 100 higher by 38.1 pts or +0.56% at 6897.22, CAC 40 up 24.61 pts or +0.41% at 5956.53 and Euro Stoxx 50 up 13.28 pts or +0.39% at 3395.01.

- Dow Jones mini up 209 pts or +0.7% at 29916, S&P 500 mini up 31.25 pts or +0.87% at 3628.75, NASDAQ mini up 111.5 pts or +1.04% at 10855.5.

COMMODITIES: Bearish Technical Theme Persists For WTI, Gold

WTI futures traded lower Friday to register a fresh low for the week. This reinstates a near-term bearish theme and highlights potential for a continuation lower. This would open $84.94 and $82.89, Fibonacci retracement levels. On the upside, a resumption of gains would instead suggest scope for a climb towards the key short-term resistance at $93.64, the Oct 10 high. A break of this level would strengthen a bullish theme. Gold maintains a softer tone following the recent reversal from $1729.5, the Oct 4 high. A continuation lower would expose the key support and bear trigger at $1615.0, the Sep 28 low. On the upside, a break of $1729.5 is required to reinstate a bullish theme.

- WTI Crude up $0.4 or +0.47% at $86.17

- Natural Gas down $0.26 or -3.97% at $6.21

- Gold spot up $10.19 or +0.62% at $1653.36

- Copper down $3 or -0.88% at $340

- Silver up $0.21 or +1.16% at $18.4676

- Platinum up $10 or +1.11% at $911.47

| Date | GMT/Local | Impact | Flag | Country | Event |

| 17/10/2022 | 1230/0830 | ** |  | US | Empire State Manufacturing Survey |

| 17/10/2022 | 1430/1030 | ** |  | CA | BOC Business Outlook Survey |

| 17/10/2022 | 1500/1700 |  | EU | ECB Lane at Bocconi Uni & Deutsche Bank Roundtable | |

| 17/10/2022 | 1530/1130 | * |  | US | US Treasury Auction Result for 13 Week Bill |

| 17/10/2022 | 1530/1130 | * |  | US | US Treasury Auction Result for 26 Week Bill |

| 17/10/2022 | 2000/1600 |  | CA | BOC Deputy Rogers panel talk at Toronto Centre | |

| 18/10/2022 | 0030/1130 |  | AU | RBA policy meeting minutes | |

| 18/10/2022 | 0200/1000 | *** |  | CN | Fixed-Asset Investment |

| 18/10/2022 | 0200/1000 | *** |  | CN | Retail Sales |

| 18/10/2022 | 0200/1000 | *** |  | CN | Industrial Output |

| 18/10/2022 | 0200/1000 | ** |  | CN | Surveyed Unemployment Rate |

| 18/10/2022 | 0200/1000 | *** |  | CN | GDP |

| 18/10/2022 | 0800/1000 |  | IT | Trade Balance | |

| 18/10/2022 | 0900/1000 | ** |  | UK | Gilt Outright Auction Result |

| 18/10/2022 | 0900/1100 | *** |  | DE | ZEW Current Conditions Index |

| 18/10/2022 | 0900/1100 | *** |  | DE | ZEW Current Expectations Index |

| 18/10/2022 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 18/10/2022 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 18/10/2022 | 1315/0915 | *** |  | US | Industrial Production |

| 18/10/2022 | 1400/1000 | ** |  | US | NAHB Home Builder Index |

| 18/10/2022 | 1600/1800 |  | EU | ECB Schnabel Alumni Event at Uni Mannheim | |

| 18/10/2022 | 1800/1400 |  | US | Atlanta Fed's Raphael Bostic | |

| 18/10/2022 | 2000/1600 | ** |  | US | TICS |

| 18/10/2022 | 2130/1730 |  | US | Minneapolis Fed's Neel Kashkari |