MNI US OPEN - Japan Said to Consider Trimming Long Issuance

EXECUTIVE SUMMARY

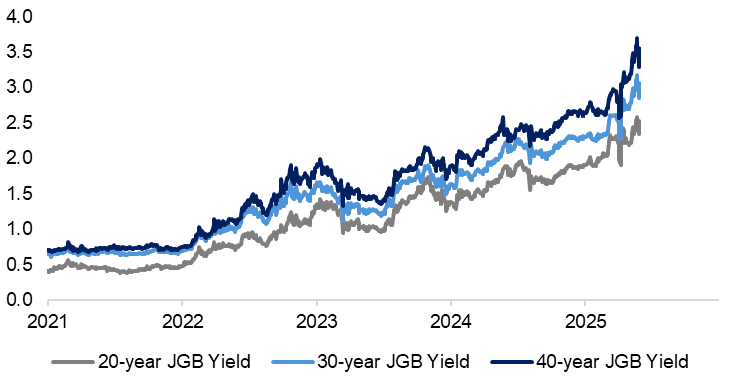

- JAPAN TO CONSIDER TRIMMING SUPER-LONG BOND ISSUANCE, RTRS SOURCES SAY

- KASHKARI FAVORS MAINTAINING FED RATES UNTIL MORE TARIFF CLARITY

- GERMANY GFK CONSUMER CONFIDENCE INCHES HIGHER FOR 3RD CONSECUTIVE MONTH

- FRANCE HICP BELOW CONSENSUS, TRANSPORT SERV/COMMS SOFTER

Figure 1: Long-end JGB yields drop as MOF reportedly consider trimming super-long bond issuance

Source: MNI/Bloomberg

NEWS

JAPAN (RTRS): Japan to Consider Trimming Super-Long Bond Issuance, Sources Say

Japan will consider trimming issuance of super-long bonds in the wake of recent sharp rises in yields for the notes, two sources told Reuters on Tuesday, as policymakers seek to soothe market concerns over worsening government finances. The Ministry of Finance (MOF) will consider tweaking the composition of its bond programme for the current fiscal year, which could involve cuts to its super-long bond issuance, said the sources who had direct knowledge of the plan. The MOF will make a decision after holding discussions with market participants around mid- to late-June, the sources said. The plan comes amid recent rises in super-long bond yields to record levels, due largely to dwindling demand from traditional buyers like life insurers.

BOJ (MNI): BOJ's Ueda Sees Inflation Near 2%, Easing Still Needed

Inflation expectations remain below the Bank of Japan's 2% target, despite reaching their highest levels in 30 years, which suggests that the BOJ must maintain accommodative policy for now, said Governor Kazuo Ueda said Tuesday. “Inflation expectations began to rise again in 2022, responding to global inflation dynamics and Japan’s continued monetary easing, Ueda said in opening remarks at the 2025 BOJ-IMES Conference. "They now stand between 1.5-2.0%, the highest in 30 years, though still below the 2% target. In other words, we have managed to de-anchor expectations from zero, but have yet to re-anchor them at 2%. This is why we are still maintaining an accommodative policy stance."

JAPAN (BBG): Japan Government Panel Warns on Rising Yields’ Hit on Finances

A Japanese government advisory panel urged authorities to step up fiscal consolidation efforts, as the Bank of Japan’s ongoing monetary tightening efforts raise the risk of higher debt-servicing costs for the world’s most indebted developed nation. The Fiscal System Council warned that the BOJ’s interest rate hikes and scaled-back bond purchases are fueling a steady rise in government bond yields, and the country’s finances need more attention, according to a proposal submitted to Finance Minister Katsunobu Kato on Tuesday.

JAPAN (NYT): Japan Will Spend $6.3 Billion to Shield Its Economy From Trump’s Tariffs

Japan has joined a growing list of nations, including Spain and Canada, that are assembling aid plans to help blunt the domestic impact of President Trump’s tariffs. On Tuesday, Japan approved a $6.3 billion spending package to “fully support” businesses and households adversely affected by the tariffs, Cabinet Secretary Yoshimasa Hayashi said in a briefing. The funds will bolster the finances of small and medium-sized businesses and subsidize household energy costs, he said.

US (BBG): Kashkari Favors Maintaining Fed Rates Until More Tariff Clarity

Federal Reserve Bank of Minneapolis President Neel Kashkari doubled down on his case for caution amid uncertainty caused by the trade war and the “paramount” need to defend inflation expectations. Speaking at a Bank of Japan event in Tokyo on Tuesday, he said there was a “healthy debate” among policymakers about whether to look through the inflation effect of US President Donald Trump’s tariffs as a transitory shock, or view it as a longer-lasting condition. “It may take months or years for negotiations to fully conclude,” Kashkari said in prepared remarks, noting that levies on intermediate goods take time to pass through, and the risks of inflation expectations becoming unmoored could increase over time.

US/EU (BBG): EU to Focus on Critical Sectors in Bid to Avoid Trump’s Tariffs

The European Union is seeking to accelerate trade talks with the US just six weeks before President Donald Trump’s threatened 50% tariffs come into effect. The European Commission, which handles trade matters for the EU, will focus its new strategy on critical sectors as well as tariff and non-tariff barriers, according to people familiar with the plans. The commission will also link its approach to addressing regulatory barriers with its plans to simplify rules. The EU’s trade chief, Maros Sefcovic, will lead political negotiations on industries such as steel and aluminum, automobiles, pharmaceuticals, semiconductors and civilian aircraft, said the people, who spoke on the condition of anonymity. Those talks will happen in parallel with the technical discussions on tariffs and non-tariff barriers.

UK (FT): UK Turns to Shorter-Term Borrowing as Fiscal Pressure Mounts

The UK government is shifting to shorter-term borrowing to lower its interest bill as a global debt sell-off adds to the pressure on its tax and spending plans. Jessica Pulay, head of the UK’s Debt Management Office, said the agency was softening a reliance on long-term borrowing that has made the country an outlier among major global bond markets, amid falling demand from institutional investors. Shorter-term debt is currently cheaper to take out — an important consideration for a country whose issuance costs have surged this year and whose Labour government is struggling to remain within its tight fiscal rules.

UK (The Times): Bank of England Faces Interest Rate Dilemma After 9% Wage Rise

Starting salaries rose at their quickest pace in nearly three years last month, underscoring the Bank of England’s tricky path towards further interest rate cuts, data on Tuesday showed. The average advertised wage climbed to £42,278 in April, up by nearly 9 per cent on an annual basis, representing the steepest increase since June 2022, according to Adzuna, a job search site. Salaries offered for vacant positions rose 0.75 per cent from March to April.

GERMANY (MNI): Chamber of Industry and Commerce Sees -0.3% GDP Growth in 2025

The German chamber of industry and commerce (DIHK) remains rather pessimistic in their spring economic survey. "None of our indicators are positive. The economic upturn that we all want and that our country needs is not yet in sight" - overall, they see -0.3% GDP growth in Germany in 2025. That is weaker than the government's forecast (0.0%), the joint economic forecast of a set of research institutes (-0.1%), and MNI's collation of sellside analysts (0.0%).

GERMANY (MNI): Exports Could Fall Up to 4% in 50% US Tariff Scenario - IFO

German exports could fall by up to E60bln or around 3-4% under a 50% US tariff scenario according to IFO calculations. "A significant proportion of German export business in the USA could become unprofitable", IFO comments. Note that US rhetoric on trade matters with the EU has softened since last week's 50% tariff threat by President Trump, with the threatened start date kicked back from Jun 1 to Jul 9. For reference, E60bln would be around 1.4% of German 2024 GDP. Initial IFO calculations following the April 2 'Liberation Day' announcements estimated a negative 0.3pp impact on German 2025 GDP (based on the 20% EU tariff rate planned then).

FRANCE (MNI): PM Bayrou to Outline Plans for Spending Cuts Early July

Speaking to BFM TV, Prime Minister Francois Bayrou says that the gov't will seek E40B in spending cuts in the next budget, with the gov't to present its proposals in early July, saying he "will ask all French people to make an effort" to steady the public finances. The PM says savings must be found as "The country is in a situation of over-indebtedness[...]. Every month, we spend 10% more than what comes into our coffers. It's an unbearable situation that cannot continue," Bayrou says that come the start of July, "I will outline in an overall plan the choices we are making to return to a certain balance in three or four years."

FRANCE (BBG): Macron Courts Southeast Asia Nations Trapped by US-China Dispute

French President Emmanuel Macron is spearheading the latest effort by European leaders to woo Southeast Asian nations worried about becoming collateral damage in the US trade war and security disputes between Washington and Beijing. Macron already announced €9 billion ($10.3 billion) in deals and promises of closer defense cooperation on a visit to Vietnam on Monday. He’ll aim to build on that momentum later this week in Indonesia and then in Singapore, where he’s giving a keynote address to the annual Shangri-La Dialogue security forum on Friday.

MNI RBNZ PREVIEW - MAY 2025: May 25bp Cut, Then?

The RBNZ decision is announced on May 28 and rates are widely expected to be cut 25bp to 3.25% bringing total easing this cycle to 225bp. 23 out of 24 analysts surveyed by Bloomberg are forecasting this outcome. Given heightened uncertainty, the MPC is likely to retain its easing bias again stating it has “scope” to cut rates further if required and its updated OCR path will be scrutinised to this end. A downward revision bringing the terminal to below 3%, estimated 'neutral', would signal a need for accommodation.

MNI NBH PREVIEW - MAY 2025: Another Cautious Hold

The National Bank of Hungary is expected to keep its base rate on hold at 6.50% again this month, despite a further slowdown in headline inflation in April. Comments from central bank officials continue to indicate that it is highly unlikely that any changes will be made to the Bank’s hawkish guidance either, with officials committed to anchoring inflation expectations. Among sell-side, no analyst we have surveyed expect to see any change to rates this month, with some still expecting the base rate to remain unchanged for the remainder of the year given the unstable risk backdrop.

DATA

GERMANY DATA (MNI): GFK Consumer Confidence Inches Higher for Third Consecutive Month

- GERMANY GFK CONSUMER CLIMATE JUNE -19.9

German June GFK consumer confidence was essentially in line with consensus at -19.9 (cons -20.0), up slightly from May's -20.8. "Both the slight decline in the willingness to buy and the increasing willingness to save are currently having a dampening effect on consumer climate and are preventing the noticeable growth in income and economic prospects from having a stronger impact on the Consumer Climate this month. The savings indicator rises by 1.6 points in May - following a significant decline in the previous month - and climbs to 10.0 points". "Consumers' income expectations increase noticeably in May. The indicator gains 6.1 points, climbing to 10.4 points".

FRANCE DATA (MNI): HICP Below Consensus, Transport Serv/Comms Softer

- FRANCE MAY HICP -0.2% M/M, +0.6% Y/Y

- FRANCE MAY CPI -0.1% M/M, +0.7% Y/Y

French HICP came in notably lower than estimated, falling to 0.62% Y/Y in May vs 0.9% consensus and 0.92% in April. National-level CPI also came in lower, at 0.67% Y/Y (0.9% cons; 0.82% April). Looking at national-level CPI, services inflation slowed down to 2.11% Y/Y (2.39% April), with transport services and communications behind the lower print according to INSEE; ahead of the release, analysts expected a decent reversal transport services due to air fares. Energy CPI dropped further into deflationary territory, at -8.11% Y/Y vs -7.77% in April. Manufactured goods CPI meanwhile was little changed at -0.23% Y/Y (-0.17% April). Food CPI accelerated a little, to 1.34% Y/Y vs 1.24% April.

SWEDEN DATA (MNI): May Economic Tendency Survey Highlights Difficult Riksbank Trade-off

The Swedish Economic Tendency Indicator eased back to 94.6 in May (vs 95.0 prior). The index has now been below the neutral 100 handle for 34 consecutive months. Sentiment fell in all industries other than construction, and while consumer confidence ticked up, it remains at heavily subdued levels. The survey doesn't provide a clear steer for the Riksbank. Weak sentiment works in favour of a rate cut in June, but expected price metrics remain elevated. There's still plenty of data due later this week, including the final Q1 GDP report.

UK MAY BRC SHOP PRICES +0.2% M/M, -0.1% Y/Y (MNI)

JAPAN DATA (MNI): Japan April Services PPI Rises 3.1% vs. Mar 3.3%

- JAPAN APRIL SERVICES PPI +3.1% Y/Y; MAR REV +3.3%

- JAPAN APRIL SERVICES PPI +0.5% M/M: MAR REV +0.8%

Japan’s services producer price index (SPPI) rose 3.1% y/y in April, easing from March’s revised 3.3%, suggesting that while corporate pass-through of cost increases remains solid, momentum is slowing, preliminary Bank of Japan data showed Tuesday. Slower gains in leasing and rental services (+1.6% vs. +2.5%) and advertising (+1.7% vs. +3.1%) weighed on April’s result. On a monthly basis, the SPPI rose 0.5% in April, following a 0.8% gain in March. Prices for services with a high labour cost ratio rose 3.5% y/y, slightly down from 3.6% in March, while those with a low labour cost ratio rose 2.7%, easing from 3.0%.

CHINA DATA (MNI): China Industrial Profits Increase in April

MNI (Beijing) China saw profits of large-scale industrial enterprises increase by 1.4% y/y from January to April, an acceleration of 0.6 percentage points compared to Q1, the National Bureau of Statistics announced on Tuesday. In April alone, profits rose 3.0% y/y, 0.4 pp faster than March, the bureau added. The results demonstrated China's industrial resilience and ability to withstand shocks, officials said in a statement on the bureau’s website, but admitted the foundation for sustained profit recovery needs further consolidation.

FOREX: Global Curve Dynamics Roil Currencies, USD/JPY Rallies 1.3%

- Global bond markets and the shape of yield curves remain the key driver for currencies, as renewed volatility in the JGB market triggers a slump in the JPY and a broad USD rally. According to sources, the Japanese Ministry of Finance solicited market opinions on the curve and the government's issuance approach via a questionnaire - triggering broad speculation that the government would re-orient away from longer-end issuance.

- The ensuing bull-flattening of the Japanese curve worked against the JPY, boosting USD/JPY by over 1.3% off the overnight low, and well within range of the Y144.00 handle. A close at current or higher levels for the pair would snap the short-term downtrend that had reversed the pair off the Y148.65 mid-May high. The initial resistance zone at 144.40, last Thursday’s high and the 20-day EMA. Above here, the 50-day EMA currently intersects at 145.73.

- EUR losses posted off the back of a lower-than-expected French CPI miss are holding, with a new pullback low at 1.1341, dipping the price below the Friday close - and reversing the entirety of the gains posted off the Trump EU tariff threat delay from yesterday. USD strength is also playing a part here - dollar's rallying alongside equities as the inverse relationship between yields and the currency continues - with strong USD/JPY demand adding an extra tailwind.

- Technically, EUR/USD sees scant support until 1.1271, the 20-day EMA, meaning today's dip lower is counter-trend. But a clear break below here would highlight a stronger reversal and signal scope for a deeper retracement. EUR/GBP meanwhile is testing major support at the 200-dma of 0.8383. This level was briefly pierced intraday last week, but hasn't sustained a break below since March earlier this year. Weakness through 0.8380 would result in the lowest print since April 3rd.

- Focus for markets Tuesday rests on prelim durable goods orders and May consumer confidence from the US. Fed's Barkin and ECB's Nagel make up the Fedspeak.

BONDS: German Paper Outperforms Gilts Across the Curve; JGBs Set Tone for FI

Moves in long-end JGBs have provided the main impetus for global FI this morning, helping the German and UK curves flatten. German paper outperforms Gilts across the curve though, leaning bull flatter with yields -0.5 to -4bps lower. The Gilt curve has twist flattened, with 2-year yields up 3bps and 30-year yields down 4bps.

- French flash May inflation was much softer-than-expected at 0.6% Y/Y (vs 0.9% cons and prior), which is supporting outperformance at the EUR short-end relative to GBP.

- 30-year Gilt yields were 8bps lower at one point this morning, temporarily finding support from an FT interview with the DMO head. Pulay noted that “there has been an important shift in the relative proportions [of short/long-end Gilts to be issued] this year”, owing to the “declining strength” of demand for longer-dated paper.

- Bund futures are +23 ticks at 130.96, off session highs of 131.22. Gilts opened at a high of 91.89, but have since eased back to 91.36 (+36 ticks today). Rolls are dominating volume in Gilts today, with U5 expected to become the front contract from tomorrow.

- 10-year EGB spreads to Bunds are mixed, with peripherals leaning slightly wider but semi-core bonds little changed to a touch tighter.

- BTP Short Term / BTPei results were digested smoothly, while the Netherlands sold 5-year DSLs this morning. The new 7-year BTP Italia is on offer for retail investors between today and Thursday.

- Eurozone economic confidence was slightly better-than-expected at 94.8 (vs 94.1 cons, 93.8 prior).

- Overnight, the UK May BRC shop price index was in line with consensus at -0.1% Y/Y (vs -0.1% prior). The CBI distributive trades survey is due at 1100BST.

EQUITIES: Latest Gains Reinforce Bullish E-Mini S&P Trend Condition

A bullish theme in Eurostoxx 50 futures remains intact and the recent pullback appears corrective. Moving average studies are in a bull-mode position, highlighting a clear uptrend and recent gains maintain the sequence of higher highs and higher lows. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Key support to watch lies at 5230.62, the 50-day EMA. Clearance of this average would signal a possible reversal. A bullish trend condition in S&P E-Minis remains intact and the latest pullback is considered corrective. Last Friday’s sell-off resulted in a print below the 20-day EMA, at 5779.53. A key support lies at 5719.58, the 50-day EMA. A clear break of this average is required to highlight a stronger reversal and signal scope for a deeper retracement. Sights are on the bull trigger at 5993.50, the May 20 high.

- Japan's NIKKEI closed higher by 192.58 pts or +0.51% at 37724.11 and the TOPIX ended 17.58 pts higher or +0.64% at 2769.49.

- Elsewhere, in China the SHANGHAI closed lower by 6.152 pts or -0.18% at 3340.687 and the HANG SENG ended 99.66 pts higher or +0.43% at 23381.99.

- Across Europe, Germany's DAX trades higher by 124.65 pts or +0.52% at 24149.55, FTSE 100 higher by 79.72 pts or +0.91% at 8797.59, CAC 40 up 14.36 pts or +0.18% at 7841.82 and Euro Stoxx 50 up 19.65 pts or +0.36% at 5414.45.

- Dow Jones mini up 539 pts or +1.29% at 42210, S&P 500 mini up 87 pts or +1.5% at 5903.5, NASDAQ mini up 352.25 pts or +1.68% at 21325.75.

Time: 09:50 BST

COMMODITIES: Gold Medium-Term Trend Signal Unchanged and Bullish

WTI futures traded to a fresh S/T cycle high last Wednesday before finding resistance. The recovery since Apr 9, appears corrective. Key resistance to watch is $62.71, the 50-day EMA. It has been pierced, a clear break of it would highlight a stronger reversal and open $65.82, Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. The price pattern on May 21 is a shooting star - a reversal signal. Gold has recovered from its recent lows. The climb signals the end of the corrective phase between Apr 22 - May 15. Medium-term trend signals are unchanged and remain bullish. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. A continuation higher would open $3435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3121.0, the May 15 low.

- WTI Crude up $0.1 or +0.16% at $61.64

- Natural Gas down $0.07 or -2.1% at $3.264

- Gold spot down $43.41 or -1.3% at $3300.13

- Copper down $7.95 or -1.64% at $475.65

- Silver down $0.48 or -1.42% at $33.0085

- Platinum down $11.51 or -1.06% at $1079.6

Time: 09:50 BST

| Date | GMT/Local | Impact | Country | Event |

| 27/05/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/05/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1300/0900 | ** | FHFA Quarterly Price Index | |

| 27/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 27/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 27/05/2025 | 1700/1300 | * | US Treasury Auction Result for 2 Year Note | |

| 28/05/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 28/05/2025 | 0130/1130 | *** | CPI Inflation Monthly | |

| 28/05/2025 | 0130/1130 | *** | Quarterly construction work done | |

| 28/05/2025 | 0200/1400 | *** | RBNZ official cash rate decision | |

| 28/05/2025 | 0600/0800 | ** | Retail Sales | |

| 28/05/2025 | 0600/1400 | ** | MNI China Money Market Index (MMI) | |

| 28/05/2025 | 0645/0845 | ** | PPI | |

| 28/05/2025 | 0645/0845 | *** | GDP (f) | |

| 28/05/2025 | 0645/0845 | ** | Consumer Spending | |

| 28/05/2025 | 0700/0900 | ** | Economic Tendency Indicator | |

| 28/05/2025 | 0755/0955 | ** | Unemployment | |

| 28/05/2025 | 0800/0400 | Minneapolis Fed's Neel Kahkari | ||

| 28/05/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 28/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 28/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 28/05/2025 | 1400/1000 | ** | Richmond Fed Survey | |

| 28/05/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 28/05/2025 | 1500/1600 | BOE's Pill on monetary policy panel at Austria National Bank / SUERF | ||

| 28/05/2025 | 1530/1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 28/05/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/05/2025 | 1800/1400 | FOMC Minutes |