MNI US OPEN - Eurozone Services HICP at Lowest Since Mar 2022

EXECUTIVE SUMMARY

- UEDA SAYS BOJ TO REVIEW JGBS, CONSIDER MARKET VIEW

- EURO AREA INFLATION FALLS BELOW ECB TARGET IN MAY

- SOUTH KOREA HOLDS SNAP PRESIDENTIAL ELECTION

- POLAND PM TO CALL CONFIDENCE VOTE IN BID TO REGAIN INITIATIVE

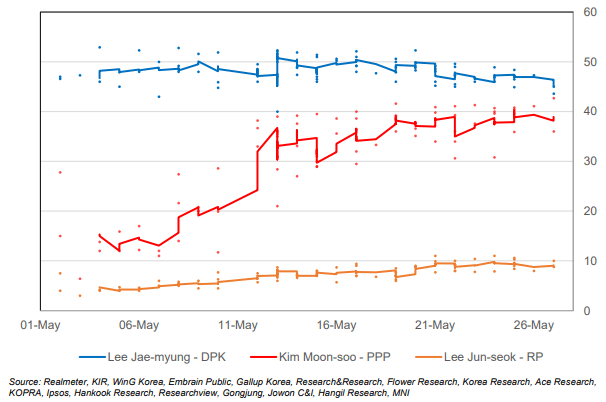

Figure 1: S. Korea presidential election opinion polling, %, short-term and 2-poll moving average (as of May 30)

NEWS

GLOBAL (MNI): OECD Cuts Global Outlook for 2nd Time This Year on Tariffs

Global economic growth forecasts were trimmed by the OECD for the second time this year because of the U.S.-led global trade war, with the new report Tuesday saying tariffs are also making central banks delay interest rate cuts because of sticky inflation. "Weakened economic prospects will be felt around the world, with almost no exception. Lower growth and less trade will hit incomes and slow job growth," chief economist Alvaro Pereira said in the report. The Paris-based group now sees global growth at 2.9% this year and next. That's down from March when the forecast was reduced to 3.1% from 3.3% for this year, and to 3% from 3.3% for 2026.

BOJ (MNI): BOJ to Review JGBs, Consider Market View - Ueda

The Bank of Japan will conduct an interim assessment of its bond tapering plans at the June 16-17 policy meeting, taking market participants’ views into account when deciding the course of JGB purchases, Governor Kazuo Ueda told lawmakers Tuesday. He noted there has been no request to revise the planned reduction of JGB buying by JPY400 billion per quarter through March 2026. However, he acknowledged that market participants hold varying views on tapering beyond April 2026.

BOJ (MNI): Gradual BOJ Hikes Intact Despite Uncertainty - Ueda

The Bank of Japan will maintain its stance of gradually raising the policy rate if economic and price conditions are realised, despite uncertainties surrounding the economic and price outlook remaining high, Governor Kazuo Ueda told lawmakers Tuesday. “Even if the U.S. tariffs were determined, uncertainties over how they will affect economies and trade remain high,” Ueda told lawmakers, repeating his view that the BOJ’s baseline scenario on the economy and prices, outlined in the May 1 Outlook Report, could change considerably depending on evolving tariffs and the global economy.

US/JAPAN (BBG): Japan’s Akazawa Still Aims for Full Reprieve on Tariffs in Talks

Japan will continue to seek a full reversal of the US tariffs, top trade negotiator Ryosei Akazawa said, as he continues to seek a deal with Washington before a temporary tariff reprieve on imports from Japan expires in early July. “There is no change to our stance that we are strongly seeking for the US to revise and reverse the various tariff measures,” he says in a press conference held Tuesday.

US/INDIA (BBG): Lutnick Sees US-India Trade Deal in ‘Not-Too-Distant Future’

Commerce Secretary Howard Lutnick said he’s “very optimistic” about prospects for a trade deal between the US and India, suggesting an agreement could come before a July deadline for higher tariffs. “You should expect a deal between the United States and India in the not-too-distant future,” Lutnick said at the US-India Strategic Partnership Forum’s Leadership Summit in Washington. “We’ve found a place that really works for both countries.”

CANADA (MNI): Carney Lays Out Faster Plan to Build Oil Pipeline

Canadian Prime Minister Mark Carney on Monday laid out a short list of conditions needed for resource projects to be fast-tracked into a two-year approval timeline, and said he's open to oil pipelines linking Alberta's landlocked heavy crude to overseas markets. Projects will be deemed in the national interest if they provide "undeniable benefits to Canada," are likely to be built out by private industry, “drive Canada’s clean growth potential” and win support from indigenous leaders, Carney said. Executives in the past have complained mines take up to 15 years to develop or that rules were so burdensome under Justin Trudeau investors were abandoning a country with some of the world's largest oil and gas reserves.

MNI POLITICAL RISK: South Korea Election Briefing

South Korea holds a snap presidential election on Tuesday, 3 June, two years ahead of schedule. The election takes place at a time of heightened political, security, and economic tensions for South Korea, with two strongly opposing views of the country’s future offered by the main candidates. Under the presidency of Yoon Suk-yeol, South Korea moved to significantly bolster relations with the US and Japan as a bulwark against China in the region. The outcome of this election could see a moderation in this stance should the defeated 2022 candidate Lee Jae-myung win, or an acceleration under foreign policy hawk Kim Moon-soo.

Polling stations are open from 06:00 to 20:00KST (07:00ET, 12:00BST, 13:00CET). Three South Korean broadcasters, KBS, MBC and SBS, will conduct an exit poll interviewing ~100k voters in person at polling stations and an additional 11,500 via telephone. This poll will be published 10 minutes after polls close at 20:10KST (07:10ET, 12:10BST, 13:10CET). In the 2022 presidential election, it took nine hours after the close of voting for Yoon Suk-yeol to be declared the winner in what was the closest presidential election in the country’s history.

POLAND (MNI): Tusk to Call Confidence Vote in Bid to Regain Initiative

Prime Minister Donald Tusk announced that he will call a confidence vote to test his parliamentary majority before the start of cohabitation with new President Karol Nawrocki. He said that his coalition has a 'contingency plan' and will start tabling draft legislation regardless of the President's stance. Tusk said that the confidence vote will be used to demonstrate 'also to our rivals in the country and abroad that we are ready for this situation, that we understand the gravity of the moment, but we are not planning to take a single step back.' The main opposition Law and Justice (PiS) went on the offensive after its candidate defeated Tusk's ally Rafał Trzaskowski in the presidential run-off. The conservative party's leader and Tusk's political nemesis Jarosław Kaczyński called for a resignation of the cabinet and proposed talks towards the establishment of a non-partisan 'technical government' after Tusk's administration 'received a red card.'

NETHERLANDS (MNI): Wilders Pulls PVV Out of Coaltion Amid Asylum Rule Row

Dutch broadcaster NOS reports that Geert Wilders, leader of the right-wing nationalist Party for Freedom (PVV) has withdrawn from the coalition, collapsing the four-party gov't. Following late-night and early-morning discussions, in which Wilders demanded stricter asylum rules, Wilders posted on X: "No signature for our asylum plans. No adjustment to the Main Outlines Agreement. PVV leaves the coalition." As MNI noted in May, the coalition has been riven with divisions for some time. Last week, Wilders blindsided the other governing parties with the 10-point agreement that would sit on top of the coalition agreement (which took five months to negotiate). The Netherlands' Council of Ministers, now sitting as a minority gov't, will meet today at 13:30CET (07:30ET, 12:30BST) to assess its options.

BOE (MNI): BOE Mann Says Can't Offset QT Impact With Rate Cut

It is not possible to simply offset the impact of quantitative tightening on financial conditions by cutting Bank Rate, Bank of England Monetary Policy Committee member Catherine Mann said. QT, which the BOE is engaged in both passively and actively, by running down and selling its gilt stock, is likely to have some tightening effect on monetary and financial conditions. A policymaker could seek to offset this through an extra rate cut, or cuts if the effect was large enough, but Mann argued against doing so.

UK (FT): Reeves Locked in UK Spending Review Showdown With Four Ministers

Rachel Reeves is facing a showdown with four leading cabinet ministers as her spending review goes down to the wire, in spite of allies’ claims that the chancellor is increasing spending by £300bn over the parliament. Angela Rayner, deputy prime minister, is fighting to defend housing and local government budgets, while Yvette Cooper, home secretary, is trying to bolster police spending to meet Labour’s crime-cutting “mission”. Meanwhile government officials confirmed that Ed Miliband, energy secretary, and Bridget Phillipson, education secretary, are yet to settle their budgets, even though final decisions will be announced on June 11.

UK (FT): KKR Drops Out of Thames Water Rescue Deal

Thames Water has announced that US private equity firm KKR will not proceed with a planned deal to inject billions of pounds of equity into the utility, throwing the future of Britain’s largest water utility into doubt. Thames Water in late March selected KKR as its preferred partner for an equity recapitalisation deal, under which the US firm would take over the near-insolvent utility and rescue it from the brink of nationalisation. However, on Tuesday Thames Water said that “KKR has indicated that it will not be in a position to proceed, and its preferred partner status has now lapsed”.

UK (The Times): Tax Rises Loom to Put Britain on a War Footing

Paul Johnson, head of the Institute for Fiscal Studies think tank, told Times Radio that there would have to be “some really quite chunky tax increases” to pay for the commitments on defence and welfare. In an interview with Andrew Neil on Times Radio, Jack Straw, foreign secretary from 2001 to 2006, said: “Taxes will have to rise. I don’t see any alternative to that and at the same time there will have to be some quite difficult retrenchment, particularly on parts of the social security budget.”

EUROPE (BBG): Macron and Meloni Aim to Reconcile as Europe Seeks United Front

French President Emmanuel Macron and Italian Prime Minister Giorgia Meloni will look to patch up difficult relations during a bilateral meeting in Rome on Tuesday, as Europe grapples with the seismic geopolitical shifts caused by the Trump administration. The talks are seen as a potential way to reset relations ahead of key NATO and Group of Seven summits scheduled for later this month, said people familiar with the matter. The meeting could even pave the way for a high-level intergovernmental summit between Paris and Rome, the people said, following years of tensions and public disputes between the two leaders.

RBA (MNI): Domestic Economy Drove 25bp Cut - RBA Minutes

Domestic economic developments on their own justified the Reserve Bank of Australia board's May decision to lower the cash rate by 25 basis points to 3.85%, with the easing case strengthened by global trade uncertainty, according to the minutes released Tuesday. However, board members did not see the case for a 50b reduction despite debating the possibility, noting limited evidence that international tensions were materially harming the local economy and warned that certain adverse scenarios could push inflation higher.

RBA (MNI): Exports to Weather Trade Volatility - RBA's Hunter

Australia’s bulk commodities exporters should weather global trade volatility in the short term, assuming Chinese authorities support their economy through fiscal stimulus, Reserve Bank of Australia Assistant Governor Sarah Hunter told an industry association Tuesday. “Australia’s resource export volumes are less sensitive to movements in global demand than other exports as we are a relatively low-cost producer of bulk commodities like iron ore,” she noted. However, Hunter acknowledged that the global environment is increasingly unpredictable, with significant uncertainty around how it will affect the domestic economy.

MEXICO (BBG): Mexico’s Supreme Court Announcement Delayed Until Tuesday: INE

The announcement of the results of the election for Mexico’s Supreme Court was postponed after being originally scheduled for Monday evening as authorities waited to complete the vote count, according to a member of the country’s electoral authority. A preliminary count with 87% of votes considered showed the three current Supreme Court justices, Lenia Batres, Yasmin Esquivel and Loretta Ortiz, leading the five female seats, followed by Maria Estela Rios and Sara Irene Herrerias.

DATA

EUROZONE DATA (MNI): Services EZ HICP Lowest Since March 2022

- EUROZONE MAY FLASH HICP +1.9% Y/Y

- EUROZONE MAY FLASH CORE HICP +2.3% Y/Y

Eurozone May flash HICP Y/Y inflation came in at 1.92%, 8 hundredths below the rounded consensus of 2.0% (vs 2.17% April) but inline with MNI's tracking estimate. On a monthly basis, Eurozone inflation came in at -0.03% (0.0% cons, 0.57% April). Services inflation stands out, seeing its lowest Y/Y rate since March 2022. Core HICP also printed below consensus, at 2.29% Y/Y and -0.01% M/M (2.4% cons; Apr 2.75% Y/Y, 1.02% M/M). Looking at the individual categories: Services inflation notably decelerated to 3.24% (3.98% Apr) - this means the category more than reversed April's unexpectedly firm print, now coming in 22 hundredths softer than March (3.46% Y/Y) and below May consensus (around 3.5% ahead of the national-level data). National-level data suggested that Easter Effect unwinds were at play here to some extent, and

the Netherlands might have an outsized negative drag this time.

EUROZONE APR UNEMPLOYMENT RATE 6.2% (MNI)

ITALY DATA (MNI): Fall in April Unemployment Rate Due to Smaller Labour Force

The Italian unemployment rate fell to 5.9% in April, below the 6.1% consensus, and prior. The fall was due to a small decline in labour force participation, with total employment unchanged for the third consecutive month. That leaves 3m/3m employment growth at 0.4% (vs 0.6% prior). The positive employment growth is consistent with the EC's expected employment indicator, which remains above the neutral 100 level (104.2 vs 103.8 prior).

SWITZERLAND DATA (MNI): May CPI Moves Below SNB Target

- SWISS MAY CPI +0.1% M/M, -0.1% Y/Y

Swiss CPI inflation printed inline with consensus at -0.1% Y/Y in May (vs -0.1% cons; 0.0% prior), and 0.1% M/M (vs 0.1% cons; 0.0% prior). Core CPI meanwhile decelerated to 0.5% Y/Y (vs 0.6% prior). This means that Swiss inflation left the SNB's target range of 0%-2% for the first time since March 2021. Despite this, remember that SNB President Schlegel has reiterated their aversion to negative rates multiple times historically, and has recently highlighted that even sub-zero prints might be acceptable for the SNB in single months. As such, the signal for near-term SNB policy expectations may be more muted, with the SNB's easing bias now well established.

NETHERLANDS DATA (MNI): Netherlands 0.8pp Below Consensus Amid Massive Services Drop

Dutch flash HICP inflation dropped to 2.95% Y/Y in May, down from 4.14% in April and notably softer than the 3.8% consensus estimate (which only consisted of 5 analysts). This equates to a 0.85% M/M sequential drop (-0.2% cons). The headline decrease was services-driven: The category fell to 2.81% Y/Y, more than making up for April's jump to 5.97% for the lowest rate since March 2022.

AUSTRIA DATA (MNI): Services Leads Austria CPI Moderation

Austrian HICP flash inflation eased by 0.3pp to 3.0% Y/Y in May along with -0.1% M/M. CPI headline inflation also dipped -0.1% M/M although saw a steadier moderation of 0.1pp to the same 3.0% Y/Y. CPI details: "Services remain the main driver of inflation with prices rising by 4.4% Y/Y - still strong, though slightly less than in recent months [4.8% April]. Prices for industrial goods saw only a slight increase of 0.8% [0.9% April]", the statistics office adds.

CHINA DATA (MNI): Caixin May Manufacturing PMI Falls Into Contraction

MNI (Beijing) China's Caixin manufacturing PMI came in at 48.3 in May, down from April's 50.4, falling into the contraction zone below the 50 mark for the first time since October 2024, the financial publisher said on Monday. The new order sub-index dropped below 50 to hit the lowest level since October 2022, partly due to the impact of the U.S. reciprocal tariff, said Caixin, adding that the new export order sub-index further declined into the contraction range. The production sub-index also ended the continuous expansion that lasted 1.5 years and fell to the lowest level since December 2022.

AUSTRALIA DATA (MNI): Net Exports Detracted From Q1 Growth

- AUSTRALIA Q1 CURR ACCT BALANCE -14663M

Not only was the current account deficit larger than expected but Q4 was revised significantly wider, but that meant that it narrowed in Q1. It was $14.7bn in Q1 after $16.3bn in Q4. Net exports detracted 0.1pp from growth while the 0.2pp contribution in Q4 was revised down to a 0.1pp detraction. The Q1 improvement in the current account was due to a smaller net income deficit as lower coal prices resulted in less dividends paid to overseas investors. The primary income deficit narrowed $2.2bn to $19.4bn. The goods & services surplus narrowed $0.2bn to $5.2bn due to a widening in the services deficit. Exports rose 1.9% q/q while imports picked up 2.2% q/q.

AUSTRALIA Q1 BIZ INDICATORS INVENTORIES +0.8% (MNI)

AUSTRALIA Q1 BIZ INDICATORS GROSS OP PROFITS -0.5% (MNI)

TURKEY DATA (MNI): Consumer Price Growth Slightly Below Estimates in May

- TURKEY MAY CPI +1.53% M/M

Consumer prices in Turkey rose 35.41% y/y in May versus +37.86% in April, a touch below estimates of a more moderate decline to +36.00%. Food and non-alcoholic beverages, transportation and housing have the three highest weights in the CPI basket, contributing 8.25ppts, 4.07ppts and 9.34ppts to the total headline figure, respectively. On a month-on-month basis, consumer prices rose 1.53% (Est: +2.00%) compared with +3.00% in April. Meanwhile, core consumer prices rose 35.37% y/y (Est: +35.70%) versus +37.12% prior. As a reminder, the CBRT kept its year-end inflation forecast of 24% unchanged as part of its latest inflation report, with analysts divided on whether a rate cut would arrive when the central bank meet next on June 19 or later.

FOREX: Mild Relief Rally for USD; EUR CPI Justifies ECB Rate Cut

- The USD is undergoing a mild corrective bounce early Tuesday, reversing a small part of the Monday underperformance as catalysts for a further phase of USD weakness dry up somewhat. The market bias remains wholly negative dollars, with the looming background threat of trade headlines still working in favour of the short side. That said, there remain short-term drivers of a potential relief rally for the USD; particularly this Friday's NFP print, at which the Fed will be watching carefully for further signs of a deterioration of the labour market. For now, the USD is the strongest currency in G10 on the day.

- Eurozone inflation data came in on the low side of expectations, with a particular step lower for services pricing prompting headline inflation to slip below the ECB's target and further justify an ECB rate cut at this Thursday's meeting. EUR/GBP edged lower in response, putting the cross to 0.8439, but still clear of the Monday lows. These remain the first downside level of note at 0.8424.

- AUD sold off on the most recent RBA rate decision, and the currency is weaker again today following the minutes of the meeting at which the bank discussed the option of a 50bps cut to the benchmark rate, with members increasingly concerned over the prospects for growth from Trump's trade tariff policies. AUD/USD found support just ahead of the 0.6450 level, but is once again pressuring that mark into early NY hours.

- JOLTS jobs data is the data highlight Tuesday, with markets expecting job openings to ebb again toward multi-year lows. Speakers set for Tuesday include Fed's Goolsbee, Cook & Logan as well as members of the BoE MPC testifying in front of UK lawmakers.

EGBS: Little Impact on Bunds From EZ HICP; DSLs Widen a Little as Govt Collapses

The softer-than-expected Eurozone flash May HICP reading did not have a material impact on Bund futures, which currently trade +20 ticks today at 131.33. A bullish theme in Bunds remains intact, with initial resistance the May 30 high at 131.44. First support lies at 130.39, the May 29 low.

- Flash headline HICP was 1.9% Y/Y (vs 2.2% prior), with soft services dragging core down to 2.3% Y/Y (vs 2.7% prior). Meanwhile, the April unemployment rate was in line at 6.2% (vs an upwardly revised 6.3% prior).

- The German curve has lightly bear flattened, with the belly aided by a solid 10-year JGB auction overnight. Yields are 0.5 to 2bps lower.

- Austria has sold RAGBs this morning, while the E4.5bln 1.70% Jun-27 Schatz auction from Germany saw solid results.

- The Dutch Government has collapsed, with right-wing leader Wilders pulling out after talks over migration policy broke down. The 10-year DSL/Bund spread widened ~1bp following the headlines, currently at 22bps.

- The Dutch news also contributed to further downside in European equity futures (-0.4% today), which sees leaves broader 10-year EGB/spreads also biased wider.

- Regional focus remains on Thursday’s ECB decision. MNI’s preview will be released today.

GILTS: Curve Flatter, Long End Auction Sees Good Demand

Gilts trade around recently registered session highs, with feedthrough from wider core global FI markets (well-received 10-Year JGB auction and slightly soft Eurozone HICP) providing some of the impetus.

- Solid demand (firmer cover than prev., tight tail, solid pricing) at the latest 4.00% Oct-63 gilt auction then added further support to the long end, with the curve already flattening ahead of supply.

- A downtick in equities also provides support for bonds.

- Gilt futures through a resistance cluster (91.87/89 & 92.00), posing a deeper threat to bears. Bulls now look to the May 8 low (92.40).

- Yields 4-7bp lower, curve flatter, but 2s10s and 5s30s remain within recent ranges.

- 10s tighten vs. Bunds, spread 4bp narrower to ~210bp. Some desks point to ongoing speculation re: UK fiscal tightening as supportive for gilts.

- GBP STIRs a little more dovish on the day as a result of the gilt move.

- SONIA futures flat to +4.0.

- BoE-dated OIS little changed to 3bp more dovish across the next 8 meetings, just under 40bp of cuts priced through year-end.

- A Treasury Select Committee hearing with BoE’s Bailey, Breeden, Dhingra & Mann is underway, pre-release comments from Dhingra & Breeden didn’t move markets.

- Little else of note on the UK calendar for the remainder of the day, which will leave focus on the TSC hearing and cross-market/macro inputs.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.216 | +0.4 |

Aug-25 | 4.085 | -12.6 |

Sep-25 | 4.041 | -17.1 |

Nov-25 | 3.897 | -31.4 |

Dec-25 | 3.816 | -39.5 |

Feb-26 | 3.704 | -50.7 |

Mar-26 | 3.686 | -52.5 |

EQUITIES: E-Mini S&P Trend Unchanged Following Recent Breach of Bull Trigger

The trend cycle in Eurostoxx 50 futures remains bullish and recent weakness appears corrective. Moving average studies are in a bull-mode position, highlighting a clear dominant uptrend. Sights are on 5516.00, the Mar 3 high and the key bull trigger. Clearance of this level would strengthen a bull theme. Key support to watch lies at 5258.36, the 50-day EMA. A clear break of this average is required to signal a possible reversal. The trend condition in S&P E-Minis is unchanged and remains bullish. Recent gains delivered a print above 5993.50, the May 20 high and a bull trigger. The break highlights a resumption of the uptrend and maintains a price sequence of higher highs and higher lows. 6000.00 has been pierced, an extension would open 6057.00 next, the Mar 3 high. Key support lies at 5756.81, the 50-day EMA. A clear break of this average is required to highlight a reversal.

- Japan's NIKKEI closed lower by 23.86 pts or -0.06% at 37446.81 and the TOPIX ended 6.18 pts lower or -0.22% at 2771.11.

- Elsewhere, in China the SHANGHAI closed higher by 14.489 pts or +0.43% at 3361.976 and the HANG SENG ended 354.52 pts higher or +1.53% at 23512.49.

- Across Europe, Germany's DAX trades lower by 24.18 pts or -0.1% at 23907.42, FTSE 100 lower by 26.68 pts or -0.3% at 8747.59, CAC 40 down 32.09 pts or -0.41% at 7703.87 and Euro Stoxx 50 down 19.52 pts or -0.36% at 5335.3.

- Dow Jones mini down 197 pts or -0.46% at 42174, S&P 500 mini down 29.5 pts or -0.5% at 5917.5, NASDAQ mini down 97 pts or -0.45% at 21436.5.

Time: 10:00 BST

COMMODITIES: WTI Futures in Consolidation Mode and Close to Recent Highs

WTI futures are in consolidation mode but remain closer to their recent highs. A bear threat remains present and the recovery since Apr 9, appears corrective. Key resistance to monitor is $62.47, the 50-day EMA. It has again been pierced. A clear break of it would highlight a stronger reversal and open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. A bullish theme in Gold remains intact and yesterday’s gains reinforce current conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. A continuation higher would open $3435.6 next, the May 7 high. On the downside, key support and the bear trigger to watch, has been defined at $3121.0, the May 15 low.

- WTI Crude up $0.3 or +0.48% at $62.84

- Natural Gas down $0.01 or -0.27% at $3.684

- Gold spot down $19.75 or -0.58% at $3361.33

- Copper down $11.25 or -2.32% at $474.7

- Silver down $0.52 or -1.5% at $34.244

- Platinum down $9.23 or -0.86% at $1059.27

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 03/06/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 03/06/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 03/06/2025 | 1400/1000 | ** | Factory New Orders | |

| 03/06/2025 | 1645/1245 | Chicago Fed's Austan Goolsbee | ||

| 03/06/2025 | 1700/1300 | Fed Governor Lisa Cook | ||

| 03/06/2025 | 1930/1530 | Dallas Fed's Lorie Logan | ||

| 04/06/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 04/06/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 04/06/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 04/06/2025 | 0130/1130 | *** | Quarterly GDP | |

| 04/06/2025 | 0700/0900 | ** | Industrial Production | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 04/06/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 04/06/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 04/06/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 04/06/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 04/06/2025 | 1215/0815 | *** | ADP Employment Report | |

| 04/06/2025 | 1230/0830 | Atlanta Fed's Raphael Bostic | ||

| 04/06/2025 | 1345/0945 | *** | Bank of Canada Policy Decision | |

| 04/06/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 04/06/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI | |

| 04/06/2025 | 1400/1000 | *** | ISM Non-Manufacturing Index | |

| 04/06/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/06/2025 | 1430/1030 | BOC press conference | ||

| 04/06/2025 | 1800/1400 | Fed Beige Book |