MNI ASIA MARKETS ANALYSIS: Potential US Gov Shutdown/NFP Delay

HIGHLIGHTS

- Treasuries look to finish near late session highs, focus on impending US govt shutdown with Federal agencies to run out of money at midnight Tuesday.

- Pres Trump meets with congressional leaders at 1500ET this afternoon in an attempt to avert a shutdown. In the event of a shutdown, the BLS will suspend data distribution: Thu's weekly jobless and Fri's non-farm payrolls.

- The USD index has started the week on the back foot, consolidating a modest 0.25% move lower on the session amid US government shutdown concerns.

US TSYS

MNI US TSYS: Yields Lower, Awaiting Word From Trump Ahead Potential Shutdown

- US Government shutdown concerns buoy Tsys into the close. No word as yet as Pres Trump meets with congressional leaders (1500ET) in an attempt to avert a shutdown as Federal agencies to run out of money at midnight Tuesday.

- The Bureau of Labor Statistics' key economic releases would be postponed in the event of a government shutdown, per the Department of Labor's plan for such an event - PDF link.

- The Dec'25 10Y contract (TYZ5) currently trades at 112-16.5 (+8) on light cumulative volumes of 972k. 10Y yield at 4.1387% (-.0368). Curves flatter: 2s10s -2.250 at 50.798, 5s30s -1.728 at 96.464.

- Treasury futures traded lower last week and remain in retracement mode. Thursday’s sell-off has resulted in a print below the 50-day EMA, at 112-10. A clear break of this average would undermine a bull theme and signal scope for a deeper retracement. This would open 111-13+, the Aug 18 low and the next key support. Initial firm resistance to watch is 113-00, the Sep 24 high.

- Pending home sales rose 4.0% M/M in August, handily above the 0.4% expected and the -0.3% reported in July. This was the highest index reading in 5 months, suggesting a potential pickup at the end of a weak period. Pending sales rose solidly in three of four regions, with Northeast sales falling.

- Fed speakers: StL Fed Pres Musalem said the Fed must be cautious cutting interest rates further because inflation remains too high, NY Fed Williams: policy decisions on a meeting-by-meeting basis, adding that this month's rate cut made sense given rising risks to employment, and leaves monetary policy at still-restrictive levels.

- Look ahead: Tuesday sees MNI Chicago PM, JOLTS, Conf. Board Consumer Confidence and more Fed speak.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.16% (-0.02), volume: $2.917T

- Broad General Collateral Rate (BGCR): 4.14% (-0.03), volume: $1.154T

- Tri-Party General Collateral Rate (TCR): 4.14% (-0.03), volume: $1.113T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.09% (+0.00), volume: $95B

- Daily Overnight Bank Funding Rate: 4.09% (+0.00), volume: $178B

FED Reverse Repo Operation

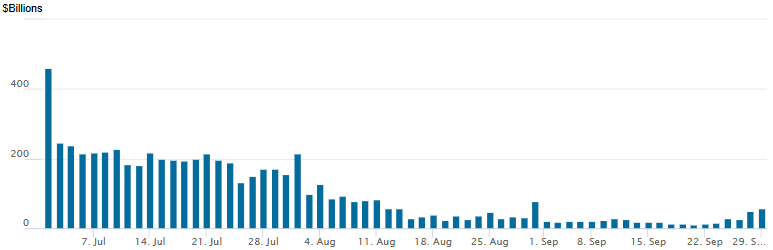

RRP usage climbs to $56.220B ahead month end with 26 counterparties this afternoon from $48.073B Friday. Compares to $11.363B on Friday, September 16 - lowest level since early April 2021. The year's high usage stands at $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options remained mixed Monday: better low delta SOFR put volumes vs. Treasury 5- and 10Y calls. Underlying futures remain higher/near highs as focus turns to US Gov shutdown (Tuesday at midnight if funding deal not reached), curves flatter. Projected rate cut pricing gaining slightly vs. late Friday levels (*): Oct'25 at -22.7bp (-22.4bp), Dec'25 at -41.3bp (-40.5bp), Jan'26 at -50.7bp (-49.9bp), Mar'26 at -60.9bp (-59.9bp).

SOFR Options:

+30,000 SFRX5 95.93/96.00/96.06 put flys, cab ref 96.29

+6,000 SFRX5 95.50/97.00 strangle w/ 95.75/96.87 strangle, 1.25 total

+10,000 SFRH6 96.50/96.68/96.87/97.06 call condors, 3.75

+5,000 SFRZ5 96.56/96.68 call spds 0.75 ref 96.275

+3,500 SFRZ5 97.50/98.00 call spds .25 ref 96.295

Update, 26,000 SFRZ5 95.87 puts, cab (huge open interest at 603,823 coming into the session)

Block, 6,015 SFRV5 96.25/96.43/96.62 call flys, 4.5 net

4,000 SFRX5 95.93/96.06 3x1 put spds

+5,400 SFRV5 96.12 puts, cab

Block 2,500 SFRV5 96.12/96.31/96.43 broken put flys, 5.0

2,000 SFRV5 96.25 straddles, ref 96.29

+2,000 0QZ5 96.25/96.50 put spds, 2.0

-6,000 SFRX5 95.93/96.06/96.18 put flys, 1.5 ref 96.285

+2,500 SFRH6 96.00/97.50/98.00 call trees, 2.0

1,500 0QV5 96.81/97.00 strangles ref 96.895

+2,300 SFRZ5 96.50/96.62 call spds, 1.0 ref 96.285

Treasury Options:

1,000 USZ5 100 puts, 1

1,000 USZ5 104 puts, 3

+20,000 FVX5 109.75 calls, 11 ref 109-04.75

3,000 TYX5 111.5/112 put spds vs. 113/114 call spds ref 112-16.5, 6 net

2,000 FVX5 111 calls, ref 109-05.75

+2,000 TUX5 104.5 calls, 3 ref 104-05

-1,400 USX5 120 calls, 14 ref 116-10

MNI BONDS: EGBs-GILTS CASH CLOSE: Bull Flattening As Euro Inflation Week Unfolds

European curves bull flattened Monday.

- Bull flattening started early, with a looming federal government shutdown in the US setting a cautious undertone.

- BOE's Ramsden sounded to be on the dovish side in an appearance and does not appear to be guiding away from a vote for a November cut so far.

- Data didn't have a major market impact. Spanish flash September core HICP was slightly softer than expected, while Eurozone economic confidence slightly above-consensus. BOE credit data was largely in-line.

- UK instruments slightly outperformed German counterparts across most of their respective curves, with the most notable divergence being at the short end.

- Periphery/semi-core EGB spreads closed mixed, with France underperforming amid continued fiscal uncertainty (Friday saw Spain upgraded by Fitch/Moody's and France's outlook lowered by Scope).

- The Eurozone flash September inflation round continues Tuesday with French, German and Italian data, with the bloc-wide figure out Wednesday. MNI's preview is here. We also get UK GDP data Tuesday, as well as several central bank speakers including BOE's Breeden and Mann, and ECB's Lagarde.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.7bps at 2.023%, 5-Yr is down 2.3bps at 2.312%, 10-Yr is down 3.9bps at 2.707%, and 30-Yr is down 5.6bps at 3.272%.

- UK: The 2-Yr yield is down 2.7bps at 3.988%, 5-Yr is down 3bps at 4.145%, 10-Yr is down 4.6bps at 4.7%, and 30-Yr is down 5.2bps at 5.509%.

- Italian BTP spread down 0.9bps at 82.6bps / French OAT up 0.5bps at 82.7bps

MNI OPTIONS: Mixed Trade To Open The Week Includes Rate, Bund Call Spread Buying

Monday's Europe rates/bond options flow included:

- RXX5 130/131.5cs, bought for 11.5 in ~2.5k

- ERZ5 97.93p, bought for 1 in 5k

- ERH6 98.00/97.9375ps vs 0RH6 97.87/97.75/97.62/97.37p condor, sold the front at 0.5 down to 0.25 in 4k

- SFIM6 96.20/95.90ps 1x2, bought for 5 in 1.5k

- SFIZ6 96.60/96.75cs vs 96.25/96.15ps, bought the cs for 0.75 in 7k Total

- SFIZ6 96.25/96.75/97.00cfly vs SFIM6 96.00p x2, traded 7.75 for the Fly in 7.5k. This trade was done Paper to Paper

MNI FOREX: US Dollar on Back Foot Amid US Shutdown Concerns

- The USD index has started the week on the back foot, consolidating a modest 0.25% move lower on the session amid US government shutdown concerns. Associated gains in G10 have been centered around the Japanese yen and notably, the Australian dollar ahead of tomorrow’s RBA decision.

- With USDJPY moving average studies highlighting a dominant uptrend, today’s 0.6% pullback appears technically corrective. Sights are on 150.92, the Aug 1 high and key resistance, while pivot support remains much further out at 145.49, Sep 17 low. Some market participants have sighted BOJ board member Asahi Noguchi’s comments as potentially assisting the yen bid on Monday.

- AUDUSD (+0.52%) edged back towards the 0.66 handle ahead of Tuesday’s central bank decision. With the RBA widely expected to be on hold in September, the focus will be on the tone of the statement and Governor Bullock’s press conference for guidance on the Board’s current thinking. Given the bullish underlying theme for AUDUSD, attention is on 0.6707, the Sep 17 high. Initial firm resistance to watch is 0.6628, the Sep 24 high.

- it’s worth noting that AUDJPY remains in a strong uptrend, with the 20-day EMA acting as very strong support in recent weeks. Additionally, an area between 97.25-45 continues to hold, while the uptrend from the April lows remains intact.

- GBPUSD’s move lower last week resulted in a break of 1.3491, a trendline support drawn from the Aug 1 low. Both 20- and 50-day EMAs also now intersect close to 1.3490, emphasising the short-term significance of this level.

- Ahead of the RBA, the BOJ summary of opinions and China PMIs are scheduled. German and French inflation releases are then due, before the US JOLTS jobs data.

MNI FX OPTIONS: Expiries for Sep30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600-05(E2.4bln), $1.1695-00(E1.8bln), $1.1725(E528mln), $1.1775(E715mln), $1.1800(E1.8bln), $1.1825-30(E850mln), $1.1850(E878mln)

- USD/JPY: Y148.00($827mln), Y149.00-15($755mln)

- AUD/USD: $0.6595-00(A$1.3bln)

- NZD/USD: $0.5785(N$1.0bln)

MNI US STOCKS: Late Equities Roundup: IT & Materials Sector Shares Outperforming

- Stocks have gradually recovered from early selling, the Nasdaq continues to outperform as Information Technology sector shares led gainers. Currently, the DJIA trades up 45.35 points (0.1%) at 46290.24, S&P E-Minis up 15.75 points (0.24%) at 6712, Nasdaq up 117 points (0.5%) at 22600.4.

- Software and semiconductor makers continued to buoy the tech sector in the second half: Western Digital +7.63%, Seagate Technology +3.78%, Micron Technology+3.72%, Lam Research +2.56% and NVIDIA +2.28%.

- Materials sector shares surged in the second half, leading gainers included: Freeport-McMoRan +5.31%, Air Products and Chemicals +1.96%, International Paper +1.24%, Amcor +1.18% and DuPont de Nemours +1.16%.

- Declining crude prices (WTI -2.55 at 63.17) continued to weigh on the Energy sector shares in late trade, leading decliners include: Devon Energy -4.11%, Targa Resources -3.97%, Diamondback Energy -3.36% and ConocoPhillips -3.33%.

- Meanwhile, the Consumer Staples sector shares decline accelerated in late trade: The Campbell's Company -3.37%, The Hershey Co -2.08%, Dollar Tree -1.83% and J M Smucker Co -1.74%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bulls Remain In The Driver’s Seat

- RES 4: 6812.29 2.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6800.00 Round number resistance

- RES 2: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6756.75 High Sep 22

- PRICE: 6722.75 @ 14:31 BST Sep 29

- SUP 1: 6640.59 20-day EMA

- SUP 2: 6577.25 Low Sep 10

- SUP 3: 6526.11 50-day EMA

- SUP 4: 6481.75 Low Sep 3

A bull cycle in S&P E-Minis remains intact. Key short-term resistance has been defined at 6756.75, the Sep 22 high where a break would resume the primary uptrend. This would open 6787.63, a Fibonacci projection. On the downside, the contract has recently pierced initial support at the 20-day EMA, currently at 6640.59. A clear breach of this average would signal scope for a deeper retracement, potentially towards the 50-day EMA, at 6526.11.

COMMODITIES

MNI Americas End of Day Oil Summary: Crude Falls

WTI crude is weaker today amid focus on excess supply concerns with flows from Kurdistan restarting at the weekend and OPEC due to meet on October 5. The next key resistance is at $68.43, the Jul 30 high, where a break is required to signal scope for a stronger recovery. For bears, a reversal lower would refocus attention on key support at $60.85. A break of this level would reinstate a bearish theme.

- OPEC+ is likely to raise output again in November after the +137kbd increased from October, Bloomberg and Reuters sources said, but capacity within the group is becoming an issue.

- Iraq has revised up its export forecast to 3.65mb/d after the resumption of shipments from Iraqi Kurdistan through the Kirkuk-Ceyhan pipeline on the weekend after a deal was finally reached with Turkey.

- WTI Nov futures were down 3.4% at $63.45

- WTI Dec futures were down 3.2% at $63.03

TUESDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 30/09/2025 | 0600/0800 | ** | Retail Sales | |

| 30/09/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/09/2025 | 0600/0800 | ** | Retail Sales | |

| 30/09/2025 | 0600/0700 | * | Quarterly current account balance | |

| 30/09/2025 | 0600/0700 | *** | GDP Second Estimate | |

| 30/09/2025 | 0645/0845 | *** | HICP (p) | |

| 30/09/2025 | 0645/0845 | ** | PPI | |

| 30/09/2025 | 0645/0845 | ** | Consumer Spending | |

| 30/09/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/09/2025 | 0755/0955 | ** | Unemployment | |

| 30/09/2025 | 0800/1000 | ** | PPI | |

| 30/09/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/09/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/09/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/09/2025 | 0900/1100 | *** | HICP (p) | |

| 30/09/2025 | 1000/0600 | Fed Vice Chair Philip Jefferson | ||

| 30/09/2025 | 1100/1300 | ECB Cipollone In Panel At Sibos | ||

| 30/09/2025 | 1150/1250 | BOE Lombardelli Panel On MonPol, Bank of Finland | ||

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 30/09/2025 | 1250/1450 | ECB Lagarde Keynote at MonPol Conference, Bank of Finland | ||

| 30/09/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 30/09/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 30/09/2025 | 1300/1500 | ECB Elderson In Panel On Climate Action | ||

| 30/09/2025 | 1300/0900 | Boston Fed's Susan Collins | ||

| 30/09/2025 | 1325/1425 | BOE Mann Fireside Chat At FT | ||

| 30/09/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/09/2025 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 30/09/2025 | 1400/1000 | *** | JOLTS jobs opening level | |

| 30/09/2025 | 1400/1000 | *** | JOLTS quits Rate | |

| 30/09/2025 | 1430/1030 | ** | Dallas Fed Services Survey | |

| 30/09/2025 | 1530/1630 | BOE Breeden Speech At Cardiff University | ||

| 30/09/2025 | 1530/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 30/09/2025 | 1600/1200 | ** | USDA GrainStock - NASS | |

| 01/10/2025 | 2300/0900 | ** | S&P Global Manufacturing PMI (f) | |

| 30/09/2025 | 2310/1910 | Dallas Fed's Lorie Logan | ||

| 01/10/2025 | 2350/0850 | *** | Tankan | |

| 01/10/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI |