MNI US OPEN - EU-UK Reach Deal Ahead of Key Leaders' Summit

EXECUTIVE SUMMARY

- TRUMP TAX BILL ADVANCES AFTER GOP DEAL FOR FASTER MEDICAID CUTS

- PUTIN HEADS INTO TRUMP CALL CONFIDENT THAT RUSSIA HAS UPPER HAND

- EU-UK DEAL REACHED AHEAD OF LEADERS' SUMMIT

- PORTUGAL’S PRIME MINISTER WINS VOTE, FAR-RIGHT PARTY SURGES

Figure 1: Relief for Romanian leu as centrist Dan wins second round of presidential election

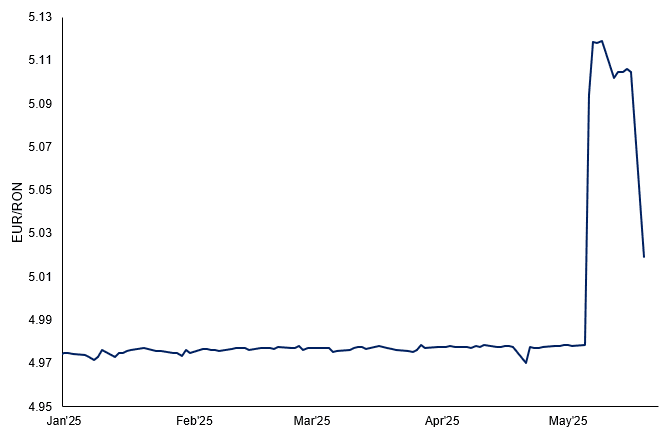

Source: MNI/Bloomberg

NEWS

US (BBG): Trump Tax Bill Advances After GOP Deal for Faster Medicaid Cuts

A key House committee advanced President Donald Trump’s giant tax and spending package after Republican hardliners won agreement from party leaders to speed up cuts to Medicaid health coverage. The House Budget Committee approved the legislation late Sunday night after a weekend of negotiations with four ultraconservatives on the panel who on Friday joined with Democrats to reject the legislation. Those hardliners instead abstained on Sunday and voted present, allowing the bill to advance.

US (MNI): Bear Steepening Extends as 30s Hover Round 5%; Does Downgrade Matter?

UST bear steepening has extended this morning, as markets digest Moody's US ratings downgrade late Friday. While the move may not have been expected, Moody's were previously the last of the three major agencies to still assign the top rating (Aaa) to US debt. US 5s30s is 5bps higher at 90bps, still shy of the multi-year high of 100bps on May 1. 30-year yields are up 5bps, hovering around the 5% handle once again. This level has provided solid resistance since Q4 2023, and was most recently respected last Thursday. Early moves in USD FX suggest the deterioration in US credit worthiness was partially priced in through the recent tax bill headlines and tariff volatility. Meanwhile, Tsy Secretary Bessent played down the ratings action over the weekend, noting Moody's - and ratings agencies more generally were a "lagging indicator" of US fiscal health.

US/RUSSIA/UKRAINE (BBG): Putin Heads Into Trump Call Confident That Russia Has Upper Hand

Vladimir Putin believes he has a strong hand ahead of a phone call Monday with Donald Trump and European leaders are trying to prevent the US president from rushing through a deal. Putin is confident that his forces can break through Ukraine’s defenses by the end of the year to take full control of four regions that he has claimed for Russia, according to a person familiar with the Russian president’s thinking who asked not to named discussing private conversations. That means the Russian president is unlikely to offer any meaningful concessions to Trump when the two leaders speak and European officials are worried that Trump may try to force through a settlement regardless.

US/JAPAN (BBG): Japan’s Ishiba Says Won’t Fixate on US Trade Talk Time Limits

Japan won’t compromise its national interests in trade talks with the US by fixating on time limits, Prime Minister Shigeru Ishiba said, signaling Tokyo isn’t rushing into an agreement. The nation won’t simply be going down the same path after the UK became the first nation to reach a trade agreement with the Trump administration earlier this month, and China reached a temporary truce with the US, Ishiba said in parliament on Monday. Japan will continue to seek exemptions for all additional tariffs imposed by the US, the prime minister said, as recent polls showed his support rate slipping further.

ISRAEL (WaPo): Israeli Ground Operations Underway in Gaza; Some Food to Be Allowed in

Israeli forces have launched "extensive" ground operations in northern and southern Gaza, the military said Sunday, as airstrikes across the territory killed about 100 people and flagging ceasefire negotiations between Israel and Hamas were underway in Qatar. The Israel Defense Forces said in a statement that the ground maneuvers were part of Operation Gideon's Chariots, a military offensive that Israeli leaders have described as including a potential long-term occupation of the Gaza Strip. Later Sunday, the office of Israeli Prime Minister Benjamin Netanyahu said his government would "introduce a basic amount of food to the population" of Gaza, after blocking all food and aid from entering the enclave for more than two months. Last week, the world's leading body on hunger crises warned that all of Gaza was at risk of famine.

PORTUGAL (BBG): Portugal’s Prime Minister Wins Vote, Far-Right Party Surges

Portugal’s ruling center-right coalition won a snap election Sunday in a vote that saw the far-right surging, rocking the two-party system that’s dominated the country’s political life for 50 years. Prime Minister Luis Montenegro’s coalition got nearly 33% of the vote and increased its seats in parliament to at least 89, up from 80, early official results showed. While that’s a stronger performance than last year’s vote, it still leaves the ruling party well short of the 116 seats required for an absolute majority in the 230-seat parliament, meaning the premier will lead a minority government.

ROMANIA (MNI): RON Extends Relief Rally on Election, But Challenges Ahead to Curb Ratings Downgrade

The clear margin of victory for centrist and pro-EU candidate Nicusor Dan against nationalist George Simion in the second round of Romania’s presidential election is perceived to be the most market-friendly outcome. Accordingly, RON has rallied below 5.050/EUR for the first time since the result of the first round two weeks ago with the leu’s 1.7% surge today its biggest intraday move since 2022. Yields on EUR-denominated bonds are as much as 50bps lower, while the Bucharest BET index has now rallied around 7% over the past two sessions. Despite the relief for Romanian assets today, with the nation’s ratings outlook having been revised from Stable to Negative by Fitch in December, S&P in January and Moody’s in March, Dan faces the difficult challenge of forming a stable, majority government and then passing a fiscal consolidation package to deal with the unsustainable deficit.

POLAND (MNI): First-Round Vote Count Confirms Unconvincing Lead of Liberal Gov't Ally Trzaskowski

Official vote count from all precincts confirmed that Rafał Trzaskowski (KO) and Karol Nawrocki (supported by PiS) will face off in the second round in what is shaping to be a very tight race. Official results from all precincts showed that the pro-government Mayor of Warsaw garnered 31.36% of the vote, with conservative opposition Law and Justice party's ally Nawrocki treading on his heels with 29.54%. The third and fourth places were taken by outperforming far-right candidates Sławomir Mentzen and Grzegorz Braun, who took 14.81% and 6.34% of the vote, respectively. The National Electoral Commission (PKW) is holding a press conference to formally announce the results while the two leading candidates are back on the campaign trail. Polish assets came under some pressure in reaction to the results, but EUR/PLN has now erased the bulk of earlier gains.

EU/UK (MNI): Deal Reached Ahead of Leaders' Summit

The UK's Minister for EU Relations, Nick Thomas-Symonds, confirms that a deal has been reached with the EU ahead of the EU-UK Summit taking place later today. Reports in the past hour suggested the EU and UK have reached a deal on fisheries that will allow a broader agreement to be signed at today's UK-EU summit. Chris Mason at the BBC writes "A 12-year deal has been done on fishing access for EU boats into UK waters, which will no doubt prompt a big row. The government will argue it has secured improved trading rights for food and agricultural products into the European Union. A defence and security pact will be central to the deal set out in a few hours. Both sides will emphasise the shared desire for deepening cooperation."

Topline details being reported on Reuters regarding the deal reached. The 'common understanding document' is said to include passages stating that the two sides: [On youth mobility, higher education and culture] "will work towards a balanced youth experience scheme on terms ot be mutually agreed", "should work towards the association of the eUK to the EU Erasmus+ programme", and "continue their efforts to support travel and cultural exchange, including the activities of touring artists'.

UK (Telegraph): Labour Revolt Over Starmer’s Brexit ‘Betrayal’

Labour rebels have turned on Sir Keir Starmer over his “reset” deal with the European Union. The agreement, to be announced on Monday by the Prime Minister and Ursula von der Leyen, the European Commission president, will mark Britain’s biggest move towards Brussels since the 2021 EU trade deal. The “reset” deal will commit to plans allowing young EU migrants to move to Britain and force the UK to follow European food standards, in what Brexiteers said amounted to “the worst of both worlds”. Labour MPs warned that the agreement would drive voters into the arms of Reform UK and flood Britain with more foreign workers, undermining Sir Keir’s pledge last week to crack down on immigration.

EUROPE (MNI): EC Downgrades Euro Area Growth, Inflation Outlook

The European Commission has significantly downgraded its Euro Area's growth and inflation outlook due to the weaker global trade environment as well as the continuing uncertainty surrounding US tariff policy. The EC revised EA growth for the year down to 0.9% for this year and to 1.4% for next year from the 1.3% and 1.6% forecast in the autumn. Inflation was also revised down to 2.1% and 1.7% in 2025 and 2026 from the 2.4% and 2.0% estimates made in the autumn forecast.

FRANCE (BBG): France Touts Record Foreign Investment at Macron’s Annual Summit

French President Emmanuel Macron will tally €37 billion ($41.4 billion) in foreign investment at an annual gathering with business leaders, seeking to send an upbeat message as the slow-growing economy faces headwinds from US trade tariffs. The projects will be announced on Monday at the “Choose France” summit, which brings together executives at the gilded Château de Versailles near Paris. Finance Minister Eric Lombard said the total investment will set a record for the event that Macron initiated seven years ago in an effort to re-industrialize the country. Of the total, €17 billion was already announced at a separate AI summit in February.

GERMANY/FRANCE (FT): Germany Drops Opposition to Nuclear Power in Rapprochement With France

Germany has dropped its long-held opposition to nuclear power, in the first concrete sign of rapprochement with France by Berlin’s new government led by conservative Chancellor Friedrich Merz. Berlin has signalled to Paris it will no longer block French efforts to ensure nuclear power is treated on par with renewable energy in EU legislation, according to French and German officials.

CHINA (MNI): China Trade Industry to Maintain Growth - NBS

MNI (Beijing) China’s foreign trade industry can withstand pressure and continue to grow this year, given the nation's industrial foundation and strong adaptability, Fu Linghui, spokesperson for the National Bureau of Statistics, told reporters on Monday. Officials will promote trade diversification and step up support for export firms, including increased tax rebates, Fu added. Fu said the China and U.S. agreement to reduce tariffs was conducive to world economic growth and increasing bilateral trade.

BOJ (MNI EXCLUSIVE): BOJ's JGB Reduction Pace Vital - Yamamoto

MNI discusses the BOJ's JGB holdings with a former official. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

BOJ (MNI): Prices Adversely Affecting Consumption - Uchida

Bank of Japan Deputy Governor Shinichi Uchida said Monday that the central bank recognises high prices, driven by rising import and rice costs, are weighing on private consumption. Speaking to lawmakers, Uchida said it remains appropriate for the BOJ to maintain its accommodative policy stance to support economic activity. However, he noted that the Bank will consider raising the policy interest rate to adjust the degree of monetary easing, should its economic forecasts materialise.

JAPAN (BBG): Japan PM Ishiba’s Support Falls, No Ouster Seen Before July

Support for Prime Minister Shigeru Ishiba’s government weakened, according to public opinion surveys published by major Japanese news organizations over the weekend, although it remains unlikely he’ll be ousted before a national election in July. Polls published by the Yomiuri and Mainichi newspapers, as well as a survey from Kyodo News, showed support for Ishiba’s cabinet ranging from 22% to 31%, the lowest levels in each survey since Ishiba became national leader in October last year.

MNI RBA PREVIEW - MAY 2025: 25bp Cut, Will CPI Reach 2.5%?

The RBA decision is announced on May 20 and a 25bp rate cut to 3.85% is widely expected (31/33 analysts on Bloomberg are forecasting -25bp with two expecting -50bp) after Q1 trimmed mean CPI fell within the 2-3% target band with activity, especially consumption, remaining lacklustre. The economy has broadly developed in line with the RBA's February expectations and thus forecast revisions this month are likely to be minimal. RBA-dated OIS pricing has a 95% probability of a 25bp rate cut in May, with a cumulative 75bps of easing priced by year-end.

CORPORATE (BBG): Nvidia CEO Unveils New Technologies to Protect AI Chip Lead

Nvidia Corp. Chief Executive Officer Jensen Huang unveiled technologies from faster chip systems to software aimed at sustaining the boom in demand for AI computing — and ensuring his products stay ahead as competition stiffens. Huang on Monday kicked off Computex in Taiwan, Asia’s biggest electronics forum, touting new products and cementing ties with a region vital to the tech supply chain. The CEO introduced updates to the ecosystem around Nvidia’s accelerator chips, which are key to developing and running AI services. The central goal is to broaden the reach of Nvidia products and get more industries and countries to adopt AI.

DATA

EUROPE DATA (MNI): EZ Services Inflation Upwardly Revised in April Final Data

- EUROZONE APR FINAL HICP +0.6% M/M, +2.2% Y/Y

- EUROZONE APR FINAL CORE HICP +1% M/M, +2.7% Y/Y

Rounded Eurozone HICP headline / core inflation was unrevised in the final April release. On an unrounded basis, headline came in at 2.17% (2.16% flash) after 2.18% in March. Core meanwhile was 2.75% (2.72% flash, 2.43% in March). In terms of contributions vs March, services adding 0.24pp was broadly outweighed by energy taking away 0.25p, while FAT and NEIG contributions were broadly unchanged. Services inflation was upwardly revised by 5 hundredths to 3.98% Y/Y (highest since August 2024), bringing the rounded rate to 4.0% - the highest since December 2024 (3.93% flash, 3.45% March). Despite the material April uptick (even the 3.93% flash reading was above all analyst estimates), general consensus is for services inflation to tick down again in the months to come.

CHINA DATA (MNI): Hard to See Significant Tariff Impacts in April Data

- CHINA APR INDUSTRIAL OUTPUT +6.1% Y/Y VS MEDIAN +5.7% Y/Y

- CHINA APR RETAIL SALES +5.1% Y/Y VS MEDIAN +5.9% Y/Y

- CHINA APR UNEMPLOYMENT RATE +5.1% VS MAR +5.2%

- CHINA YTD FIXED-ASSET INVESTMENT +4.0% Y/Y VS MEDIAN +4.2% Y/Y

April data releases showed limited impact from the trade war. April retail sales did decline to +5.1% (from +5.9% in March) yet remains above the 1 year average of +3.6% and the 5 year average of +4.5%. In what could be front running tariffs, industrial production beat expectations rising +6.1%, ahead of forecasts of +5.7%. Investments in Fixed Assets (excluding rural households) rose +4.0%, moderately lower than March's result of +4.2%. The ongoing malaise in the property sector shows limited signs of improving (as witnessed by the release of home prices earlier today) with the April. Property Investment YTD YoY printing at -10.3% where it has remained since 2023. China's surveyed jobless rate was steady at +5.1%.

CHINA DATA (MNI): House Prices Down, Shanghai a Brightspot

April's house price data continued to highlight the challenges for authorities in achieving a recovery in the multi-year downturn in house prices. April's new house prices decline increased from March to -0.12%, representing 23 consecutive months of contracting. April's used house prices decline increased from March to -0.41%, representing a contraction in every month since the last expansion in April 2023. New home prices did rise in 22 cities MoM compared to March and 3 cities saw growth YoY. Used home prices in 5 cities rose MoM. Beijing saw a rise in new home prices of +0.01% MoM yet declined -5% YoY. Shanghai saw a rise in new home prices of +0.5% MoM whilst delivering a +5.9% YoY increase.

RATINGS: U.S. Lost Aaa Status at Moody’s on Friday, Some Tweaks Elsewhere

Sovereign rating reviews of note from after hours on Friday include:

- Fitch affirmed Greece at BBB-, Outlook revised to Positive

- Fitch affirmed Slovakia at A-; Outlook Stable

- Moody's downgraded the United States of America to Aa1 from Aaa, outlook changed to stable

- S&P affirmed South Africa at BB-; Outlook Positive

- Morningstar DBRS confirmed the United Kingdom at AA, Stable Trend

- Scope upgraded Slovenia to A+, Outlook Stable

FOREX: USD Sold in Several Phases on Moody's Downgrade

- Several phases of dollar sales accompanied the European open Monday, helping boost EUR/USD and GBP/USD through the overnight highs as well as the Friday highs in both pairs. The Moody's US downgrade remains the primary driver here, which spills over into Treasury yields and equities through the European cash open.

- JPY trades similarly well and outperformed in Asia-Pac trade, although gains have faded slightly into the NY crossover. GBP/JPY bounced well ahead of the intraday support at the Y192.58 200-dma.

- The overall size of these greenback moves are telling: a net of ~100 pips in EUR/USD on the sovereign downgrade signals that the deterioration in US credit worthiness was partially priced in through the recent tax bill headlines and tariff volatility - both of which remain a primary concern as they filter into hard economic data. US Treasury Secretary Bessent played down the ratings action over the weekend, noting Moody's - and ratings agencies more generally - were a "lagging indicator" of US fiscal health.

- A heavy session for Fedspeak dominates the calendar Monday, with the Atlanta Fed's Financial Markets Conference (set to continue until Wednesday) top of the agenda. Fed's Bostic, Jefferson, Williams, Logan and Kashkari are all set to make appearances.

- President Trump is set to hold a call with Russian President Putin later today, headed into which Putin reportedly believes he holds the upper hand in negotiations, meaning Russia are unlikely to offer any meaningful concessions as part of a peace deal. Market sensitivity to peace talks in Ukraine remains high, but no progress is expected in the very short-term.

EGBS: UST Spillover and Heavy Issuance Weighs on Major EGB Futures

Spillover from US Treasuries and a heavy morning of corporate/sovereign supply has weighed on major EGB futures, with Bunds down 61 ticks at 129.81. Key support remains at 129.13, the May 15 low.

- Reaction to Moody’s US sovereign rating downgrade late Friday has set the tone across global markets. with USD FX and rates under notable pressure.

- In Europe, today’s new 7-year E3bln WNG EFSF syndication comes alongside auctions from Slovakia and the EU (1030BST), as well as several corporate deals.

- The German 5s30s curve is up 2bps on the sesion to ~90bps, seeing a more modest intraday steepening than UST counterparts (+4.2bps to 89bps).

- 10-year EGB spreads to Bunds have generally widened, with the US downgrade dampening global equity sentiment. The BTP/Bund spread has widened 1.5bps to 102bps, after hovering around the psychological 100bp handle through last week.

- Rounded Eurozone HICP headline / core inflation was unrevised in the final April release at 2.2% Y/Y and 2.7% Y/ respectively. Services inflation was upwardly revised by 5 hundredths to 3.98% Y/Y (highest since August 2024), bringing the rounded rate to 4.0%.

- The European Commission has significantly downgraded its Euro Area's growth and inflation outlook due to the weaker global trade environment as well as the continuing uncertainty surrounding US tariff policy.

GILTS: Sell Off & Steepening Extends

Gilts remain under pressure as Tsys soften in the wake of the U.S. sovereign rating downgrade from Moody’s late on Friday.

- Futures are through next support and the bear trigger (90.96) and have pierced Fibonacci support (90.92), with bears now eying the April 11 low (90.47). lows of 90.86 so far.

- Yields are 3-9bp higher, curve steeper.

- 10-Year yields register the highest level of the month 4.726%, with the next upside level of note at the April high (4.800%).

- 30-Year yields also hit the highest level of the month (5.492%), with the April 11 high (5.546%) presenting the next area of upside interest.

- 10s spread vs. Bunds 1bp wider at 206.5bp, set for the highest close since April 22.

- GBP STIRs move in a hawkish direction given the sell off further out the curve.

- SONIA futures little changed to -7.5.

- BoE-dated OIS little changed to 1.5bp more hawkish across ’25 meetings showing ~41bp of cuts through year-end.

- Wednesday’s CPI data headlines the UK calendar this week. We have written a little on that in our global week ahead/late Friday bullets, expect more in our full preview.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Jun-25 | 4.200 | -1.0 |

Aug-25 | 4.055 | -15.5 |

Sep-25 | 3.994 | -21.6 |

Nov-25 | 3.867 | -34.3 |

Dec-25 | 3.803 | -40.7 |

Feb-26 | 3.718 | -49.2 |

Mar-26 | 3.703 | -50.7 |

EQUITIES: Bullish Theme in Eurostoxx Futures Intact With Price at Recent Highs

A bullish theme in Eurostoxx 50 futures remains intact and price is trading at its recent highs. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. The continuation higher signals scope for a climb towards 5516.00, the Mar 3 high and the key bull trigger. Initial firm support to watch lies at 5181.06, the 50-day EMA. Clearance of this level would signal a possible reversal. A bullish trend condition in S&P E-Minis remains intact and last week’s appreciation reinforces current conditions. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5681.27, the 50-day EMA.

- Japan's NIKKEI closed lower by 255.09 pts or -0.68% at 37498.63 and the TOPIX ended 2.06 pts lower or -0.08% at 2738.39.

- Elsewhere, in China the SHANGHAI closed higher by 0.121 pts or +0% at 3367.583 and the HANG SENG ended 12.33 pts lower or -0.05% at 23332.72.

- Across Europe, Germany's DAX trades lower by 68.04 pts or -0.29% at 23706.66, FTSE 100 lower by 50.3 pts or -0.58% at 8634.86, CAC 40 down 53.2 pts or -0.67% at 7835.14 and Euro Stoxx 50 down 36.12 pts or -0.67% at 5392.3.

- Dow Jones mini down 369 pts or -0.86% at 42367, S&P 500 mini down 78 pts or -1.31% at 5897.5, NASDAQ mini down 369.75 pts or -1.72% at 21135.

Time: 10:00 BST

COMMODITIES: WTI Future Downtrend Intact Despite Recent Test of Key Resistance

A downtrend in WTI futures remains intact and recent gains are considered corrective. Key resistance to watch is $62.93, the 50-day EMA. It has recently been pierced, a clear break of it would highlight a stronger reversal. This would open $65.82, the Apr 4 high. For bears a reversal lower would refocus attention on $54.33, the Apr 9 low and bear trigger. Clearance of this support would confirm a resumption of the downtrend. A corrective cycle in Gold remains in play and the metal traded lower last week. A key support at $3202.0, the May 1, low has been breached. The break of this level signals scope for a deeper retracement, towards $3085.0, 76.4% of the Apr 7 - Apr 22 upleg. Note that the 50-day EMA at $3169.4, has also been breached, strengthening a bearish threat. Initial resistance is $3259.5, the 20-day EMA.

- WTI Crude down $0.44 or -0.7% at $62.04

- Natural Gas down $0.08 or -2.43% at $3.253

- Gold spot up $41.01 or +1.28% at $3244.62

- Copper up $1.65 or +0.36% at $461.05

- Silver up $0.3 or +0.92% at $32.6029

- Platinum up $6.8 or +0.69% at $998.33

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 19/05/2025 | 1245/0845 | New York Fed's John Williams | ||

| 19/05/2025 | 1245/0845 | Fed Vice Chair Philip Jefferson | ||

| 19/05/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 19/05/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 19/05/2025 | 1715/1315 | Dallas Fed's Lorie Logan | ||

| 19/05/2025 | 1730/1330 | Minneapolis Fed's Neel Kashkari | ||

| 20/05/2025 | 0430/1430 | *** | RBA Rate Decision | |

| 20/05/2025 | 0600/0800 | ** | PPI | |

| 20/05/2025 | 0800/1000 | ** | EZ Current Account | |

| 20/05/2025 | 0800/0900 | BOE's Pill At Barclays Briefing | ||

| 20/05/2025 | 0900/1100 | ** | Construction Production | |

| 20/05/2025 | 1000/1200 | ECB's Cipollone pre-rec video at Sustainability Festival | ||

| 20/05/2025 | - | ECB's Lagarde and Cipollone at G7 Meeting | ||

| 20/05/2025 | 1230/0830 | *** | CPI | |

| 20/05/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 20/05/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 20/05/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 20/05/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 20/05/2025 | 2100/1700 | Fed Governor Adriana Kugler |