MNI US OPEN - China GDP Growth Slows to 4.8% as Headwinds Grow

EXECUTIVE SUMMARY

- TRUMP LISTS TOP DEMANDS ON CHINA BEFORE TRADE TALKS RESUME

- INDIA SAYS IT’S NARROWING GAP WITH US ON TRADE DEAL DISPUTE

- S&P CASTS DOUBT OVER BUDGET CONSOLIDATION; MOODY'S DUE FRIDAY

- JAPAN’S LDP REACHES COALITION DEAL TO SET UP TAKAICHI AS PREMIER

- CHINA'S Q3 GDP SLOWS TO 4.8% ON INCREASED HEADWINDS

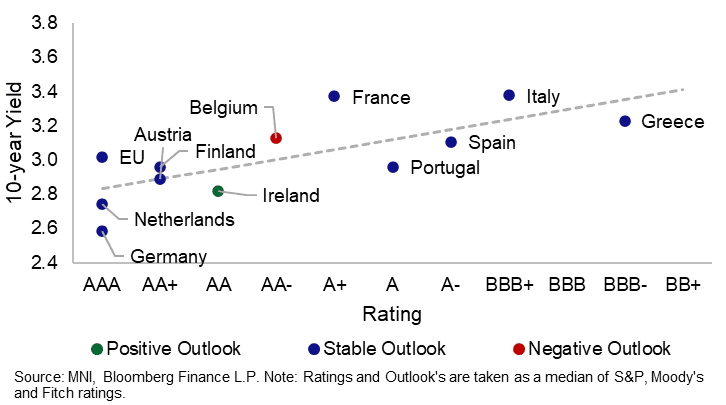

Figure 1: EGBs ratings curve (10-year)

NEWS

GLOBAL (BBG): AWS Service Disruption Hits Perplexity, Robinhood Sites

Amazon Web Services, the world’s largest cloud provider, suffered a widespread disruption on Monday morning that degraded services for several companies, including artificial intelligence company Perplexity and the Coinbase and Robinhood financial platforms. “We can confirm increased error rates and latencies for multiple AWS Services in the US-EAST-1 Region.” Amazon.com Inc. said on the AWS health dashboard. User complaints began spiking just after 7:30 a.m. London time, with data from data from Down Detector showing thousands of user reports.

US/CHINA (BBG): Trump Lists Top Demands on China Before Trade Talks Resume

President Donald Trump listed rare earths, fentanyl and soybeans as the US’s top issues with China just before the two sides return to the negotiating table and as a fragile trade truce nears expiration. “I don’t want them to play the rare earth game with us,” Trump said on Air Force One on Sunday, as he headed back to Washington from Florida. Days earlier, the US leader threatened a 100% tariff on Chinese shipments after Beijing vowed to exert broad controls on the minerals.

US/INDIA (BBG): India Says It’s Narrowing Gap With US on Trade Deal Dispute

India said it’s making solid progress in trade negotiations with the US as it looks to clinch a trade deal and bring down punitive tariffs. The two sides have narrowed their differences on trade-related matters, an Indian official told reporters in New Delhi on Saturday, asking not to be identified as the discussions are private. There are no major differences between India and the US on trade issues, the person said. A team of negotiators from India had positive meetings with officials in Washington last week, the person said.

US/S.KOREA (BBG): Korea Says ‘Substantial Progress’ Made in US Tariff Talks

South Korea’s top policy chief said the country made “substantial progress” on most key issues in tariff talks with the US, following a weekend of meetings that also saw Seoul’s top tycoons attend a golf event with Donald Trump at his Mar-a-Lago estate. The two countries reached broad agreement on many issues, though several points still require further negotiation, Kim Yong-beom, the presidential policy chief, said in a televised briefing Sunday. He added the chances of finalizing a deal at the upcoming Asia-Pacific Economic Cooperation summit had increased.

US/AUSTRALIA (BBG): Australia Pitches to Be US Fix for China’s Rare Earths Curbs

Australia’s prime minister is set to pitch his nation’s vast resource holdings as a solution to China’s rare earth curbs at a meeting Monday with President Donald Trump, as the US and other countries scramble to diversify supply of critical minerals. Anthony Albanese is due to meet with Trump at around 11 a.m. in Washington and will aim to use the sit down to secure an agreement with the US on critical minerals.

US/COLOMBIA (NYT): Colombia’s Leader Accuses U.S. of Murder, Prompting Trump to Halt Aid

President Gustavo Petro of Colombia accused the United States of murdering an innocent fisherman in an attack on a boat that the American authorities claimed had been carrying illicit drugs, prompting President Trump to declare on Sunday that he would slash assistance to Colombia, one of Washington’s top aid recipients in Latin America, and impose new tariffs on the country’s goods. The feuding between the two leaders reflected rising tensions in the region over the huge U.S. military deployment in the Caribbean targeting Colombia’s neighbor, Venezuela. U.S. forces have killed dozens of people in recent weeks aboard vessels that the Trump administration says were ferrying drugs from Venezuela.

ISRAEL/MIDEAST (BBG): Israel Says Gaza Truce Resumes After Deadly Clashes With Hamas

Israel said it had resumed a truce with Hamas in Gaza after heavy fighting over the weekend, with the sides accusing each other of breaching a deal brokered by US President Donald Trump. Around 9:30 p.m. Israel time on Sunday, the Israel Defense Forces said it had “begun renewed enforcement of the ceasefire” and warned it would “respond firmly to any violation.” Israel launched strikes against Hamas in Gaza and suspended aid shipments on Sunday after blaming the Iran-backed militant group for an ambush that killed two soldiers in the southern part of the strip.

FRANCE (MNI): S&P Casts Doubt Over Budget Consolidation; Moody's Due Friday

While the timing of S&P's decision came as a surprise, the outcome was in line with our expectations. S&P wrote that "reflecting the likelihood of modifications to the 2026

draft budget, we expect deficits to remain elevated over the next three years" S&P's 2026 deficit forecast of 5.3% is well above Lecornu's target of 4.7% (which is expected to move closer to 5.0% through the budget negotiation phase). Moody's are scheduled to review France's sovereign rating on Friday (Current rating Aa3, Outlook Stable). An outlook downgrade to Negative is likely (and probably in the price for OATs), but a downgrade to A1 remains a risk.

EQUITIES (MNI): BNP Paribas Losses Lead French Underperformance

European cash equities are higher across the board, however France are the exception. Banks were trading heavy through the open on the S&P downgrade on Friday, however losses have accelerated for BNP Paribas (shares halted for volatility, last lower by near 8%) as last week's jury ruling against BNP Paribas could set a large legal precedent and sizeable settlement costs for the bank. A New York Jury on Friday found the bank "complicit in Sudan atrocities", leading to the award of $21mln for 3 plaintiffs. While the fine size is insignificant at this stage, a Bloomberg intelligence article has extrapolated the fine to a potential class action bill of $150bln, although a settlement of nearer to $10bn is more likely.

UK (MNI): Weekend Headlines Focus On Energy VAT Removal: Costs and CPI Impacts

The main fiscal headlines from the weekend have suggested that VAT may be removed from energy bills (which was in line with rhetoric last week from Reeves). This was "hinted" at by Energy Secretary Milliband when he refused to rule it out in an interview. This would cost somewhere in the region of around GBP1.75-2.0bln (although this is dependent upon wholesale prices). In terms of an impact on CPI, "electricity, gas and misc energy" has a 3.2642% weighting. So removing VAT from energy bills would reduce CPI by about 0.16ppt.

ECB (MNI): MonPol May Work Faster in Shocks - Schnabel

Monetary policy appears to work faster and more forcefully than previous estimates implied once shocks are properly identified, European Central Bank executive board member Isabel Schnabel said on Monday. In welcoming remarks to the WE_ARE_IN conference in Frankfurt, Schnabel said the ECB needs to constantly rethink its monetary toolkit as recent research has challenged conventional wisdom, citing more powerful interactions of fiscal and monetary policy than traditional models and less weight of household differences in aggregate demand.

ESTONIA (MNI INTERVIEW): Estonia Likely to Favour Longer Maturities

The Head of Estonia's State Treasury Janno Luurmees discusses the outlook for that country's debt issuance.

UKRAINE (MNI): Zelenskyy to Attend EUCO After Unsuccessful White House Visit

Reuters reporting comments from President Volodymyr Zelenskyy following his high-profile meeting with US President Donald Trump on 17 Oct. In the wake of Trump continuing to delay the provision of Tomahawk missiles (capable of striking deep into Russia), Zelenskyy claims that Ukraine is preparing a contract for the purchase of 25 Patriot missile systems (which have defensive rather than offensive capabilities). On Trump's continued delay to Tomahawk provision, Zelenskyy says, 'In my view, Trump does not want escalation with Russia until he has had a chance to have another meeting with Moscow'.

EU/RUSSIA (BBG): EU Nations Close In on Deal to Ban Russian Gas by End of 2027

European Union energy ministers aim to agree a joint position on plans to ban all gas supplies from Russia by the end of 2027, as the bloc looks to definitively end its reliance on energy from Moscow. Officials are meeting in Luxembourg Monday to hash out their stance for further talks on the law, which starts by prohibiting Russian supplies under existing short-term contracts by mid-June, with an exemption for landlocked countries such as Hungary and Slovakia. A prohibition on long-term deals follows 18 months later.

BOJ (MNI): BOJ’s Takata Sees Price Target in Sight

Bank of Japan board member Hajime Takata said on Monday that Japan’s economy is at a stage where the price stability target is nearly achieved, signaling his continued support for raising the policy interest rate, though he did not elaborate on timing. “Firmness in the U.S. economy has been maintained since then. As U.S. long-term interest rates have bottomed out and the yen's appreciation has been avoided even after the Federal Reserve's September rate cut, I believe that this rate cut, unlike cases seen repeatedly in the past, will not act to constrain rate hikes in Japan,” Takata told business leaders in Hiroshima City.

BOJ (RTRS): BOJ May Slightly Revise Up This Year's Growth Forecast, Sources Say

The Bank of Japan may slightly revise up this year's growth forecast next week and maintain its view the economy was on course for a moderate recovery, despite headwinds from U.S. tariffs, said three sources familiar with its thinking. At the next policy meeting on October 29-30, the BOJ will conduct a quarterly review of its growth and price forecasts.

JAPAN (BBG): Japan’s LDP Reaches Coalition Deal to Set Up Takaichi as Premier

Japan’s ruling Liberal Democratic Party will sign a coalition deal with the Japan Innovation Party later Monday, according to the smaller party’s leader, a move that would set up Sanae Takaichi to become the country’s first female prime minister. The LDP and the JIP, also known as Ishin, have broadly reached an agreement and will announce the deal at 6 p.m., Hirofumi Yoshimura, Ishin’s co-leader told reporters, after speaking with Takaichi earlier in the day.

CHINA (MNI): Oct LPR Remains Unchanged

MNI (Beijing) China's Loan Prime Rate held steady on Monday, in line with expectations while the central bank holds the easing pace amid uncertainties from the economic slowdown and escalating China-U.S. trade tensions. According to a statement on the website of People’s Bank of China, LPR remained unchanged at 3.0% for the one-year maturity and 3.5% for the five-year tenor and over. Both rates fell in May by 10bp after the PBOC lowered the 7-day reverse repo rate – its benchmark policy rate – 10bp to 1.4% on May 8, followed by a 50bp reduction to the reserve requirement ratio on May 15.

VIETNAM (BBG): Vietnam Stocks Fall By Most Since April on Bond Violation Woes

Vietnamese stocks plunged by the most in six months amid a reemergence of concerns over corporate bond issuance violations following the release of inspection results from regulators. The VN Index tumbled as much as 5.6%, the most since April 22. Vingroup, Vinhomes and Bank for Foreign Trade of Vietnam were among the biggest drags on the measure. The Government Inspectorate of Vietnam on Friday released findings from inspection of 67 bond issuers, including 5 banks that highlighted “various violations”, according to local media reports.

DATA

EUROZONE FINAL Q2 GDP +0.1% Q/Q, +1.5% Y/Y (VS +0.6% Q/Q, +1.6% Y/Y Q1) (MNI)

EUROZONE AUG CONSTRUCTION OUTPUT -0.1% M/M, +0.1% Y/Y (VS +0.5% M/M, +0.7% Y/Y JUL) (MNI)

GERMANY DATA (MNI): Energy Main Driver in September PPI

- GERMANY SEP PPI -0.1% M/M, -1.7% Y/Y

German September PPI was slightly softer-than-expected at -1.7% Y/Y, below the -1.5% consensus but above the -2.2% prior reading. The pullback was driven by the energy component, with PPI ex-energy rising marginally to 0.9% Y/Y (0.8% prior according to the Destatis database, note that the press statement mentions an unchanged rate at 0.9%). Moves were limited across the main categories, with all of investment, intermediate, consumption, durable and non-durable goods seeing deviations of +-0.1pp maximum vs their August rates.

CHINA DATA (MNI): China's Q3 GDP Slows to 4.8% on Increased Headwinds

- CHINA Q3 2025 REAL GDP +4.8% Y/Y VS MEDIAN +4.7% Y/Y

- CHINA Q3 2025 REAL GDP +1.1% Q/Q VS MEDIAN +0.8% Q/Q

- CHINA SEP INDUSTRIAL OUTPUT +6.5% Y/Y VS MEDIAN +5.0% Y/Y

- CHINA SEP RETAIL SALES +3.0% Y/Y VS MEDIAN +3.0% Y/Y

- CHINA SEP UNEMPLOYMENT RATE +5.2% VS AUG +5.3%

MNI (Beijing) The Chinese economy grew by 4.8% year-on-year in Q3, slowing by 0.4 percentage points from Q2 and bringing the accumulated GDP for the first three quarters to 5.2%, National Bureau of Statistics data showed Monday, citing external tariff disruption and the great pressure of domestic economic restructuring. China’s fixed-asset investment growth fell by 0.5% y/y in the Jan–Sep period from the previous 0.5% gain, marking the slowest pace since Jul 2020 and missing the median forecast of 0.1%.

NEW ZEALAND DATA (MNI): Q3 CPI Consistent With RBNZ Thinking

Q3 CPI printed very close to consensus and the RBNZ's August projections with a couple of quarterly increases a bit higher. Thus, this outcomes is unlikely to derail any further easing in November. Headline rose 1.0% q/q to 3% y/y after 0.5% & 2.7% in Q2, the top of the target band, with tradeables up 0.8% q/q and domestically-driven non-tradeables +1.1%. While headline CPI inflation hit the top of the RBNZ's 1-3% target band in Q3, underlying inflation remained within it but at the upper end. The RBNZ's own measure of core from its sector factor model was stable at 2.7% y/y in Q3, remaining at the lowest since Q1 2021, while Statistics NZ's CPI ex food, energy and vehicle fuel moderated 0.2pp to 2.5% y/y.

FOREX: USDJPY Has Volatile Session, NZD Firmer Post Q3 CPI

- The USD index holds close to Friday’s closing levels, having traded within a tight 18 pip range to start the week. China third quarter GDP slowed to 4.7% Y/y, however the print came in marginally above expectations, prompting minimal impact on broader risk sentiment and the greenback. President Trump expressed optimism around US-China trade talks (albeit with clear focus points), keeping major equity benchmarks in the green Monday.

- Despite the limited price adjustments across G10 FX, the Japanese yen has had a volatile session overnight. Developments regarding Japan's LDP and Ishin parties forming a coalition, which should pave the way for Takaichi to become the new PM, initially boosted USDJPY to 151.20, extending its bounce from the Friday lows to 1.22%.

- Howver, the pair has traded notably lower since since, weighed by hawkish remarks from BoJ board member Takata, BOJ headlines on revising the economic growth forecast up and pressure off the highs for major equity benchmarks. Short-term USDJPY support at the 20-day EMA was pierced last week, and further weakness would signal scope for a deeper retracement towards 50-day EMA, at 148.86. Markets will remain attentive to the gap to the October 03 close, located at 147.47.

- Elsewhere, New Zealand Q3 CPI came in at 1.0% Q/q, one tenth above market expectations. While the data overall was close to RBNZ expectations as well, NZD does stand 0.25% higher on the session, while AUDNZD is comfortably off session highs to trade closer to 1.13. For NZDUSD, bearish conditions remain firmly intact, with the pair remaining within 1% of cycle lows at 0.5683, 6-month lows for the pair.

- Looking ahead, the ECB's Nagel and Vujcic speak later today after Canada's Q3 BoC business survey print. Tomorrow, UK fiscal data will be published ahead of Canada CPI.

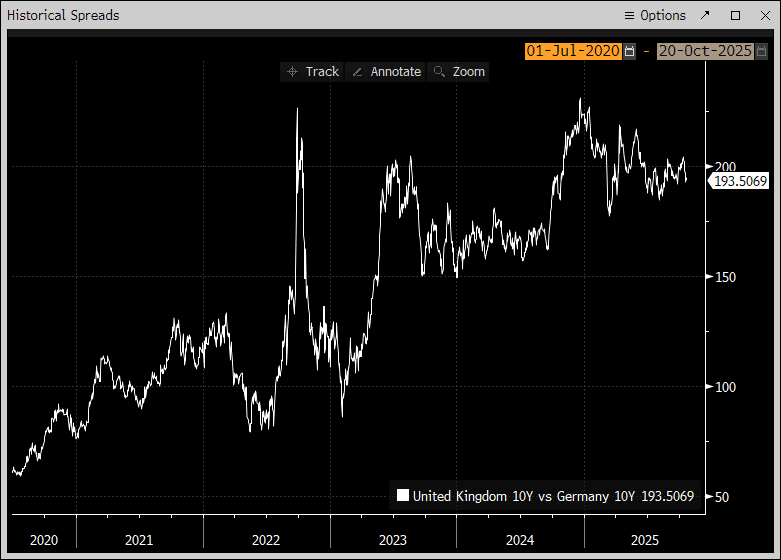

BONDS: 10-Year Gilt/Bund Spread Narrows 1.5bps, Sep 24 Support in View

The 10-year Gilt/Bund spread is 1.5bps narrower at ~193.5bps. Initial support is the Sep 24 close around 192bps, clearance of which would bring the spread to its tightest since mid-August and expose the August 1 close at 184.5bps. Aggregate moves have been relatively contained this morning, with the UK and Eurozone data calendar picking up later in the week.

- There are a few drivers of Gilt outperformance versus Bunds over the past week:

- On the monetary policy/data side, last week’s UK labour market data was soft, while Governor Bailey retained optionality for a Q4 rate cut.

- On the fiscal side, there are some expectations that the UK’s "fiscal black hole" won’t be quite as large as was previously feared, alongside speculation that Chancellor Reeves may increase fiscal headroom above the c. GBP10bln seen in the last two fiscal events.

- Fiscal policy remains a key focus for the Gilt market ahead of the Nov 26th budget. The main fiscal headlines from the weekend have suggested that VAT may be removed from energy bills.

- UK yields are little changed across the curve, while German yields are up to 1.5bps higher with a light bear steepening bias noted.

- In futures, Bunds are -14 ticks at 129.83, while Gilts are +1 at 92.47.

- Slovakia and the EU have sold bonds this morning, while books for Italy’s latest retail offering have opened. Estonia has issued a mandate for a 2034 bond tap.

- This week’s calendar includes UK public sector finance (Tues), CPI (Weds) and flash PMI (Fri) data. In the Eurozone, Friday’s flash PMIs highlight.

Figure 1: 10-year Gilt/Bund Spread (Source; Bloomberg Finance L.P)

EQUITIES: Recent Weakness in E-Mini S&P Appears Corrective For Now

The trend direction in Eurostoxx 50 futures remains up and the latest pullback appears to have been a correction. The contract remains above key support at 5498.73, the 50-day EMA. A clear break of the 50-day average is required to highlight a stronger reversal. On the upside, the bull trigger is unchanged at 5689.00, the Oct 2 high. Clearance of this hurdle would confirm a resumption of the uptrend. Recent weakness in S&P E-Minis appears corrective - for now. Price has pierced support at the 50-day EMA, currently at 6615.80, but this support area remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. Clearance of this level would undermine a bull theme. Moving average studies continue to remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high.

- Japan's NIKKEI closed higher by 1603.35 pts or +3.37% at 49185.5 and the TOPIX ended 78.01 pts higher or +2.46% at 3248.45.

- Elsewhere, in China the SHANGHAI closed higher by 24.138 pts or +0.63% at 3863.893 and the HANG SENG ended 611.73 pts higher or +2.42% at 25858.83.

- Across Europe, Germany's DAX trades higher by 204.2 pts or +0.86% at 24031.19, FTSE 100 higher by 32.62 pts or +0.35% at 9386.89, CAC 40 down 4.96 pts or -0.06% at 8165.61 and Euro Stoxx 50 up 30.47 pts or +0.54% at 5635.82.

- Dow Jones mini up 86 pts or +0.19% at 46471, S&P 500 mini up 18.5 pts or +0.28% at 6720.75, NASDAQ mini up 93.25 pts or +0.37% at 25079.5.

Time: 10:00 BST

COMMODITIES: Next Support for WTI Futures at $54.89, the May 5 Low

A bearish theme in WTI futures remains intact and the move down last week reinforces current condition. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. Sights are on $54.89 next, the May 5 low, where a break would open $54.10, the Apr 9 low and a key support. Initial firm resistance is seen at $61.93, the 50-day EMA. Key resistance has been defined at $66.42, the Sep 26 high. A bull cycle in Gold remains intact and last week’s extension reinforces current conditions. The move higher maintains the price sequence of higher highs and higher lows. Sights are on the $4400.00 handle next, and $4404.9, a Fibonacci projection point. Note that the trend is in overbought territory. A move down - a correction - and would allow the overbought set-up to unwind. Support to watch lies at $3986.3, 20-day EMA.

- WTI Crude down $0.27 or -0.47% at $57.28

- Natural Gas up $0.18 or +6.02% at $3.188

- Gold spot up $3.73 or +0.09% at $4255.55

- Copper up $2.4 or +0.48% at $499.4

- Silver down $0.01 or -0.02% at $51.9313

- Platinum down $38.74 or -2.39% at $1580.81

Time: 10:00 BST

| Date | GMT/Local | Impact | Country | Event |

| 20/10/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 20/10/2025 | 1400/1600 | ECB Schnabel Panel at Macroeconomics and Finance Conference | ||

| 20/10/2025 | 1430/1030 | ** | BOC Business Outlook Survey | |

| 20/10/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 20/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 21/10/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/10/2025 | 0700/0900 | ECB Lane at Macroeconomics and Finance Conference | ||

| 21/10/2025 | 0900/1100 | * | Government Debt | |

| 21/10/2025 | 0900/1100 | * | Government Deficit | |

| 21/10/2025 | 0900/1000 | BOE Saporta Fireside Chat at Islamic Development Bank | ||

| 21/10/2025 | 1030/1130 | BOE Bailey & Breeden on Private Markets at Financial Services Regulation Committee | ||

| 21/10/2025 | 1100/1300 | ECB Lagarde Keynote at Norges Bank Climate Conference | ||

| 21/10/2025 | 1230/0830 | *** | CPI | |

| 21/10/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 21/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 21/10/2025 | 1915/2015 | BOE Mann Fireside Chat at Lazard |

Note: Due to U.S. government shutdown, some data may be unavailable.