MNI US OPEN: Global Pains As Dollar Gains

EXECUTIVE SUMMARY:

- UK RETAIL SALES SLUMP, SENDING POUND TO LOWEST SINCE 1985

- YEN AT 150 WOULD PUT PRESSURE ON BOJ

- PBOC RESPONSE MAY BE NEEDED AS YUAN BREACHES 7: ANALYSTS

- ECB'S REHN, DE GUINDOS EYE GROWTH DOWNSIDE AS RATES RISE

- RBA's LOWE SAYS 25BPS AND 50BPS ON TABLE IN OCTOBER

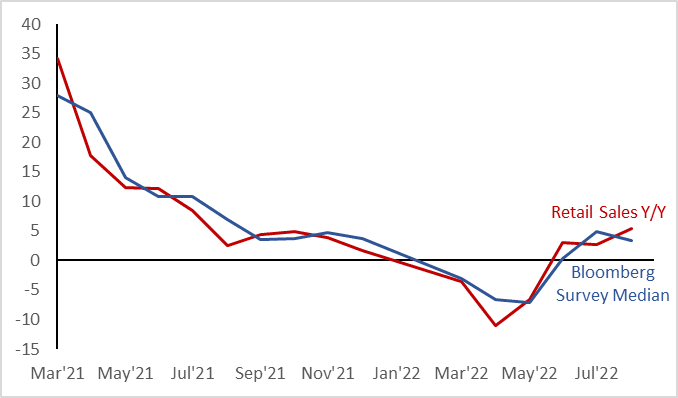

Figure 1: Chinese Retail Sales Y/Y Beat Expectations

NEWS

EU (BBG): ECB’s Rehn Says Growing Recession Risk May Keep Wages in Check

“The growing risk of recession in the euro area and the steadily increasing labor participation rate might also be factors that have kept wages in check,” European Central Bank Governing Council member Olli Rehn said in Helsinki. “De-globalisation as well as the war in Ukraine are putting further pressure on real incomes, and so wage-price dynamics could become a concern. Yet, we have not seen strong signals of such dynamics so far”

EU (MNI): EUCO Pres-EU Must Limit Energy Consumption, Increase Supply

Comments from President of the European Council Charles Michel hitting wires. In line with proposals from the Commission, Michel states that the EU must limit its energy consumption while at the same time increasing supply.

States that the EU needs to engaged with Algeria, Saudi Arabia, Qatar, and the UAE to deal with the current energy crisis. Says that for most of these four countries it is possible to increase supply, and that the conditions for this must be determined. Michel says that there are 'good proposals' on energy prices on the table but that 'more will be needed'. Adds that investment in renewables must be sped up.

EU (MNI): ECB Policy May Cause Short-term Pain - De Guindos

European households and businesses may be set for a "painful" period as policymakers attempt to keep inflation under control at the same time as the euro area economy slows, European Central Bank vice president Luis De Guindos said in an interview Friday

JAPAN (MNI): Yen At 150 Would Put Pressure On BOJ

The Bank of Japan fears it may come under increasing political pressure to shift its policy bias to neutral from easing should the yen fall to 150 to the dollar, given the government's lack of an effective tool to support the currency, MNI understands.

JAPAN (MNI): Jiji Survey Shows Kishida Cabinet's Approval Rating at Record Lows

Approval of Prime Minister Kishida's Cabinet fell to an all-time low in the latest Jiji poll, corroborating the findings of recent surveys from other outlets. The approval rating was 32.3%, down 12.0pp from the previous month, reaching worst levels since the inauguration of the Kishida administration last October. The disapproval rate rose 11.5pp to 40.0%, exceeding the approval rate for the first time.

CHINA (MNI): PBOC Response May Be Needed as Yuan Breaches 7 - Analysts

The People's Bank of China could officially reintroduce the counter-cyclical factor into its yuan pricing model as one tool to slow any sharp slide in the currency after it breached 7 against the U.S. dollar for the first time since mid-2020 despite recent efforts to stem the selling momentum.

The PBOC has plenty of tools to curb "abnormal" volatility in the yuan should it diverge too much from the rising U.S. Dollar Index, said Wang Qing, chief macroeconomic researcher at Golden Credit Rating.

CHINA (MNI): China's Economy Expected to Continue Recovery

The Chinese economy is expected to recover and grow within a reasonable range following the improvements in August economic indicators, said Fu Linghui, spokesman of the National Bureau of Statistics at a briefing on Friday.

China will continue to promote investment by making good use of policy bank-backed infrastructure funds and tapping into the remaining quota of project-backed local government special bonds, said Fu. He noted that the CNY300 billion funds previously approved for policy banks have supported more than 900 projects with a total investment exceeding CNY3 trillion.

AUSTRALIA (MNI): RBA's Lowe Says 25bps and 50bps On Table in October

The Reserve Bank of Australia will consider hikes of 25bps or 50bps at its Oct 4 meeting as it looks for rates to eventually "cycle" between 2.5%-3.5%, Governor Philip Lowe told a parliamentary committee. The RBA is approaching more normal monetary settings and the case for large adjustments in rates has "diminished", Lowe said. "I think at our next board meeting we'll be considering whether it's a 25bps or 50bps increase.

DATA

EUROZONE AUG FINAL HICP +0.6% M/M, +9.1% Y/Y (MNI)

The final euro area CPI figures were largely unchanged in August, with a small 0.1pp uptick on the headline month-on-month figure largely due to higher energy prices recorded at the end of the month. This confirms a 0.2pp uptick in headline CPI and a more-concerning 0.3pp acceleration in core year-on-year inflation.

UK (MNI): Retail Sales Slump Sending Pound Lower

UK AUG RETAIL SALES -1.6% M/M, -5.4% Y/Y

UK AUG RETAIL SALES EX-FUEL -1.6% M/M, -5% Y/Y

UK retail sales fell sharply in August, underlining the struggle consumers are having with rising prices and falling real incomes. By volume, sales fell 1.6% month-on-month with sales lower in all sub-sectors of the data for the first time since July 2021, the Office for National Statistics said.

With energy prices continuing to put pressure on the consumer, an ONS spokesperson said sales by volume would need to rise by 3.1% in September for the sector to have a flat contribution to overall GDP in Q3. That, going into a Bank of England policy meeting, will show the Monetary Policy Committee just how difficult conditions are on the UK high streets.

CHINA AUG INDUSTRIAL OUTPUT +4.2% Y/Y VS MEDIAN +3.8% Y/Y (MNI)

CHINA JAN-AUG INDUSTRIAL OUTPUT +3.6% Y/Y VS JAN-JUL +3.5% Y/Y (MNI)

CHINA AUG RETAIL SALES +5.4% Y/Y VS MEDIAN +3.1% Y/Y (MNI)

CHINA AUG UNEMPLOYMENT RATE +5.3% VS JUL +5.4% (MNI)

FOREX: The Pound falls across the board

- The Pound fell across the board following a poor UK retail sales data, as rising inflation impact consumer's purchasing powers.

- Sales in the UK declined in all sectors.

- Cable plummeted to its lowest level since 1985, through the 1.1400 handle, and printed a 1.1351 low, now at 1.1378 at the time of typing.

- Currencies are under renewed pressure against the Dollar, with the latter taking its cue from further falls in Equities.

- Equities have extended their losses on Global recession concerns and rate hike outlook.

- Today, also sees option expiry for single stocks and indices, with large notional equivalent set to expire, so expect some volatility at and after the US Cash Equity open.

- NOK is the worst performer in G10 against the USD, down 1.04%.

- The USD is in the green against all the majors, besides KRW and JPY.

- Resistance in the USDNOK is now seen at the 2022 peak 10.3552.

- This was also the highest print since 12/05/20.

- USDSEK sees 10.8540, followed by the September high at 10.8854, which was also the highest print since December 2001.

- Looking ahead, focus will be on the US prelim Michigan and its inflation component.

BOND SUMMARY: Schatz the biggest movers again

- Schatz are the biggest movers in core FI space again with yields up 4.6bp, with the Euribor strip under pressure this morning - up to 8.5 ticks lower. No real data drivers again - more continued momentum from the past few days amid focus on ECB expectations (71bp now priced for October and a terminal rate of 2.75% by June 2023).

- The German curve has bear flattened with 10y Bund yields closer to flat on the day.

- Treasuries following Bunds (to some extent albeit with smaller moves). Michigan confidence data along with the inflation expectations component is the highlight for the remainder of the day.

- Gilt yields are a little lower - but with the curve bull flattening through 10-year yields moving lower as the terminal rate moves lower following this morning's disappointing retail sales data.

- TY1 futures are down -0-0+ today at 114-15+ with 10y UST yields up 0.8bp at 3.459% and 2y yields up 3.1bp at 3.898%.

- Bund futures are down -0.48 today at 142.74 with 10y Bund yields up 0.3bp at 1.769% and Schatz yields up 4.6bp at 1.566%.

- Gilt futures are down -0.07 today at 105.26 with 10y yields down -1.3bp at 3.149% and 2y yields down -0.5bp at 3.098%.

EQUITIES: Bearish Retracement Continues

- Japan's NIKKEI closed lower by 308.26 pts or -1.11% at 27567.65 and the TOPIX ended 11.87 pts lower or -0.61% at 1938.56.

- Elsewhere, in China the SHANGHAI closed lower by 73.521 pts or -2.3% at 3126.398 and the HANG SENG ended 168.69 pts lower or -0.89% at 18761.69.

- Across Europe, Germany's DAX trades lower by 252.82 pts or -1.95% at 12732.17, FTSE 100 lower by 17.5 pts or -0.24% at 7272.81, CAC 40 down 103.27 pts or -1.68% at 6073.57 and Euro Stoxx 50 down 58.09 pts or -1.64% at 3491.38.

- Dow Jones mini down 272 pts or -0.88% at 30717, S&P 500 mini down 37.75 pts or -0.97% at 3866, NASDAQ mini down 138 pts or -1.16% at 11808.75.

COMMODITIES: Gold Remains In Clear Downtrend

- WTI Crude up $0.19 or +0.22% at $84.48

- Natural Gas down $0.23 or -2.78% at $8.098

- Gold spot down $2.71 or -0.16% at $1656.26

- Copper down $4.45 or -1.28% at $344

- Silver down $0.23 or -1.2% at $18.8407

- Platinum down $13.9 or -1.53% at $891.11

| Date | GMT/Local | Impact | Flag | Country | Event |

| 16/09/2022 | 1215/0815 | ** |  | CA | CMHC Housing Starts |

| 16/09/2022 | 1400/1000 | *** |  | US | University of Michigan Sentiment Index (p) |

| 16/09/2022 | 2000/1600 | ** |  | US | TICS |

| 17/09/2022 | 1645/1845 |  | EU | ECB Chief Economist Lane Cantillon Lecture | |

| 19/09/2022 | 0900/1100 | ** |  | EU | Construction Production |

| 19/09/2022 | 1230/0830 | * |  | CA | Industrial Product and Raw Material Price Index |

| 19/09/2022 | 1400/1000 | ** |  | US | NAHB Home Builder Index |