MNI US MARKETS ANALYSIS - Treasury Curve Flatter as FOMC Begin Meeting

May-03 11:11By: Edward Hardy and 1 more...

Newsletter - send to homepage

Highlights:

- Treasury curve flattens as FOMC meet

- AUD/NZD nears four year high on larger-than-exp RBA rate hike

- Equity price action reinforces bearish condition

US TSYS SUMMARY: Twist Flattening Into Start Of FOMC Meeting

- Cash Tsys see a modest twist flattening after yesterday’s bear steepening, as a re-firming of Fed hike expectations ahead of tomorrow’s FOMC decision supports the front-end whilst long-end yields dip slightly after rising sharply yesterday.

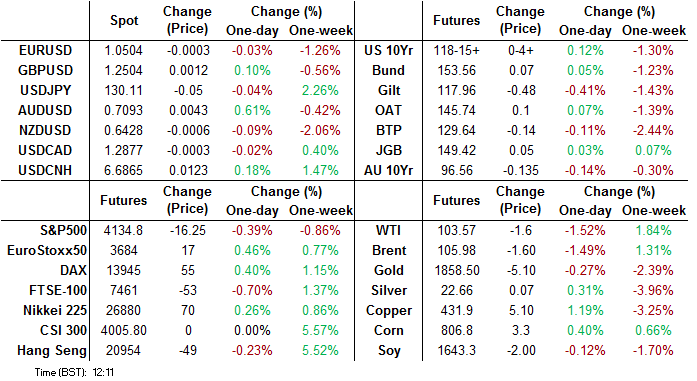

- 2YY +2.1bps at 2.754%, 5YY +0.0bps at 3.005%, 10YY -1.1bps at 2.967%, 30YY -1.8bps at 3.015%.

- TYM2 is up just 3 ticks at 118-14 as it largely consolidates yesterday’s move lower, with volumes back at average after a light session with London out. Initial support at the earlier low of 118-04+ whilst key resistance sits at 120-18+ (Apr 27 high).

- Data: Today’s pick is likely JOLTS for March for further signs of labour market tightness, but we also get finalised durable goods for March plus Wards vehicle sales for April.

- No issuance until Thu, kicked off by 4W and 8W bills.

STIR FUTURES: Fed Hike Expectations Get A RBA Boost

- Implied hikes early saw a boost from the RBA surprisingly hiking 25bps to 0.35% (cons 15bps).

- They remain off yesterday’s highs for near-term meetings (52bp May, 109bp June) but are back close to where they peaked for later in the year (202bp Sep, 253bp Dec).

- Data: finalised durable goods/factory orders and JOLTS for March both at 1000ET. Job openings are again seen dipping marginally on the month to 11.20M (after peaking at 11.45M in Dec) but the sharper decline in unemployment would see the number of unemployed to openings fall to a new low of 0.5.

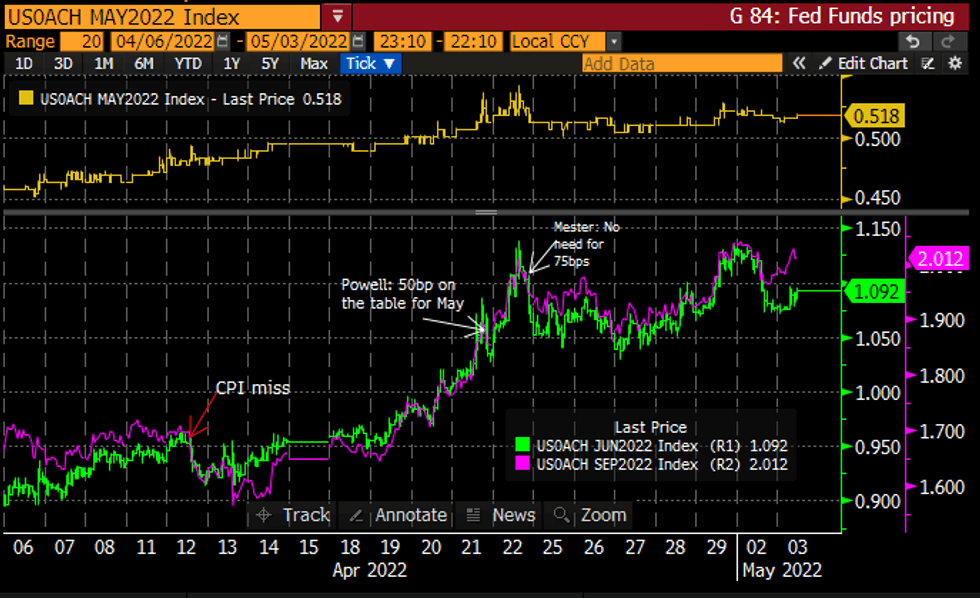

Source: Bloomberg

Source: Bloomberg

EGB/GILT SUMMARY: Curves Flatten

European government bond curves have flattened this morning on the back of the shorter end trading weaker with gilts underperforming EGBs.

- Focus is on this week's central bank policy meetings with the Federal Reserve and Bank of England expected to raise rates further amid intensifying inflationary pressure.

- Gilts have traded weaker across the curve with yields up 4-6bp.

- The bund curve has twist flattened with the 2s30s spread narrowing 5bp.

- The OAT curve has also twist flattened 4bp.

- BTPs have similarly traded weaker at the front and stronger at the back of the curve. The very long end of the curve is now 7bp flatter on the day.

- Supply this morning came from Germany (ILB, EUR560mn allotted), Belgium (TCs, EUR2.365bn) and the ESM (Bills, EUR1.085bn).

EUROPE ISSUANCE UPDATE:

- Germany allots E560mln 0.10% Apr-33 ILB, Avg yield -1.73% (Prev. -2.44%), Bid-to-cover 0.92x (Prev. 0.93x), Buba cover 1.23x (Prev. 1.76x)

FOREX: AUD on Top Following Chunkier Rate Hike

- AUD outperforms all others early Tuesday, with the RBA surprising markets overnight with a 25bps rate hike to 0.35% vs. Expectations of a 15bps tweak. In the subsequent press conference, governor Lowe flagged that the bank could raise rates as high as 1.5% by the end of 2022, and to 2.5% at a cyclical peak.

- In response, AUD/USD made light work of Monday's 0.7082, rallying to just shy of 0.7150 before the pair faded somewhat.

- NZD is softer in comparison, helping AUD/NZD surge well north of the 1.10 handle for the first time since August 2020. Strength north of 1.1065 would mark fresh four year highs.

- GBP is trading more solidly following the return of UK traders after Monday's bank holiday. GBP/USD is back above the 1.25 level for now, although the outlook remains bearish following last week's acceleration of the downtrend. Price has recently cleared 1.2974, Apr 13 low and 1.2676, last printed in September 2020. This has reinforced bearish conditions. The trend remains oversold, however, a reversal pattern is still required to signal a short-term base and a possible reversal.

- US factory orders and final March durables goods data cross alongside JOLTS at 1500BST/1000ET, with BoC's Rogers also on the docket. Members of both the Fed's FOMC and BoE's MPC remain in pre-meeting media blackout periods.

FX OPTIONS: Expiries for May03 NY cut 1000ET (Source DTCC)

- USD/JPY: Y127.00($860mln), Y129.75($550mln)

Price Signal Summary - S&P E-Minis Probes Key Support

- In the equity space, S&P E-Minis remain in a downtrend, despite the recovery from yesterday’s low. Fresh lows have reinforced underlying bearish conditions and yesterday’s move lower resulted in a probe of key support at 4094.25, the Feb 25 low. A clear break of this level would reinforce bearish conditions. 4056.00, Monday’s low, has also been defined as an important bear trigger. EUROSTOXX 50 futures are consolidating but remain vulnerable. The moving average set-up continues to highlight a bear mode condition. A resumption of weakness would open 3551.60, the 61.8% retracement of the Mar 7 - 29 rally. Key resistance is unchanged at 3883.00, Apr 21 high.

- In FX, EURUSD is trading near its recent lows and remains in a clear downtrend. The recent consolidation appears to be a bear flag. A resumption of the downtrend would open 1.0454, the Jan 1 2017 low. The GBPUSD outlook remains bearish, following the recent impulsive selling pressure. The focus is on 1.2375, the 2.382 projection of the Mar 23 - Apr 13 - 14 price swing. USDJPY bulls have paused for breath. Last week's resumption of the primary uptrend and the break of 130.00 suggests scope for further upside. The focus is on 131.96, the 1.00 projection of the Feb 24 - Mar 28 - 31 price swing. DXY remains in a clear uptrend and last week probed major resistance at 103.82, the Jan 3 2017 high. A clear break of this hurdle would strengthen bullish conditions. Note that the strong monthly close in the index for April is a bullish signal. In Japanese candle terms, April is a standard line pattern and this is a continuation signal.

- On the commodity front, Gold remains weak. The recent pullback from the $1998.4 high (Apr 18), and the breach last week of $1890.2, the Mar 29 low, continues to highlight a bearish threat. Attention is on $1848.8, 76.4% retracement of the Jan 28 - Mar 8 rally. On the upside, $1922.5 the 20-day EMA is seen as a firm short-term resistance. In the Oil space, WTI futures continue to trade inside a triangle formation that has appeared on the daily chart and is drawn from the Mar 15 low. The pattern is a bearish signal and suggests potential for a test and break of support at $95.28, Apr 25 low. Resistance is at $106.24/107.99, triangle resistance and the Apr 29 high.

- The broader trend condition in the FI space remains bearish. Bund futures have traded lower today and entered territory below 153.00. This reinforces bearish conditions and an extension lower would open 152.65, the Sep 1 2015 low (cont). The broader trend condition in Gilts remains bearish. Resistance has been defined at 119.79, the Apr 26 high. Attention is on the bear trigger at 117.22 bear trigger, Apr 22 low.

EQUITIES: Cyclical Stocks Lead Early European Gains

- European equities are mostly higher, led by Energy, Consumer Discretionary, and Financial stocks, with the German Dax up 80.61 pts or +0.58% at 14019.62, FTSE 100 down 24.21 pts or -0.32% at 7522.49, CAC 40 up 52.51 pts or +0.82% at 6485.26 and Euro Stoxx 50 up 25.71 pts or +0.69% at 3758.99.

- U.S. futures are flat, with the Dow Jones mini up 12 pts or +0.04% at 32994, S&P 500 mini up 2.75 pts or +0.07% at 4154, NASDAQ mini up 4.75 pts or +0.04% at 13077.75.

- Several Asian markets were closed for holidays.

EQUITIES: Earnings Season Begins to Wind Down

- Earnings season enters its final few weeks, with activity and reports declining markedly

- Pfizer, Moderna, AMD, S&P Global and CVS Health among the highlights

- Full schedule with timings, EPS & revenue expectations here: https://marketnews.com/mni-us-earnings-schedule-re...

COMMODITIES: Precious Metals Weaken As Rates Rise

- WTI Crude down $1.04 or -0.99% at $104.13

- Natural Gas up $0.2 or +2.72% at $7.678

- Gold spot down $8.84 or -0.47% at $1853.99

- Copper up $5.5 or +1.29% at $432.3

- Silver down $0.05 or -0.24% at $22.5858

- Platinum up $7.3 or +0.78% at $945.99

| Date | GMT/Local | Impact | Flag | Country | Event |

| 03/05/2022 | - | *** |  | US | Domestic-Made Vehicle Sales |

| 03/05/2022 | - |  | EU | ECB Lagarde & Panetta in Eurogroup Meeting | |

| 03/05/2022 | 1255/0855 | ** |  | US | Redbook Retail Sales Index |

| 03/05/2022 | 1300/1500 |  | EU | ECB Lagarde High School Q&A | |

| 03/05/2022 | 1400/1000 | ** |  | US | factory new orders |

| 03/05/2022 | 1400/1000 | ** |  | US | JOLTS jobs opening level |

| 03/05/2022 | 1400/1000 | ** |  | US | JOLTS quits Rate |

| 03/05/2022 | 1515/1615 |  | UK | BOE Mutton Panellist at Bankers Association | |

| 03/05/2022 | 1630/1230 |  | CA | BOC Sr Deputy Rogers speaks on operational independence | |

| 04/05/2022 | 2300/0900 | * |  | AU | IHS Markit Final Australia Services PMI |

| 04/05/2022 | 2301/0001 | * |  | UK | BRC Monthly Shop Price Index |

| 04/05/2022 | 0130/1130 | ** |  | AU | Retail Trade |

| 04/05/2022 | 0130/1130 | ** |  | AU | Lending Finance Details |

| 04/05/2022 | 0600/0800 | ** |  | DE | trade balance |

| 04/05/2022 | 0715/0915 | ** |  | ES | IHS Markit Services PMI (f) |

| 04/05/2022 | 0745/0945 | ** |  | IT | IHS Markit Services PMI (f) |

| 04/05/2022 | 0750/0950 | ** |  | FR | IHS Markit Services PMI (f) |

| 04/05/2022 | 0755/0955 | ** |  | DE | IHS Markit Services PMI (f) |

| 04/05/2022 | 0800/1000 | ** |  | EU | IHS Markit Services PMI (f) |

| 04/05/2022 | 0830/0930 | ** |  | UK | BOE M4 |

| 04/05/2022 | 0830/0930 | ** |  | UK | BOE Lending to Individuals |

| 04/05/2022 | 0900/1100 | ** |  | EU | retail sales |

| 04/05/2022 | 1100/0700 | ** |  | US | MBA Weekly Applications Index |

| 04/05/2022 | 1215/0815 | *** |  | US | ADP Employment Report |

| 04/05/2022 | 1230/0830 | ** |  | CA | International Merchandise Trade (Trade Balance) |

| 04/05/2022 | 1230/0830 | ** |  | US | Trade Balance |

| 04/05/2022 | 1345/0945 | *** |  | US | IHS Markit Services Index (final) |

| 04/05/2022 | 1400/1000 | *** |  | US | ISM Non-Manufacturing Index |

| 04/05/2022 | 1430/1030 | ** |  | US | DOE weekly crude oil stocks |

| 04/05/2022 | 1800/1400 | *** |  | US | FOMC Statement |