MNI US MARKETS ANALYSIS - On Watch for Scale of Iran Response

Highlights:

- Market on watch for broader Iranian response to Israeli strikes

- Enrichment sites targeted, Trump stresses Iran must make a deal

- Implications for inflation remain to be seen - central bank pricing errs hawkishly

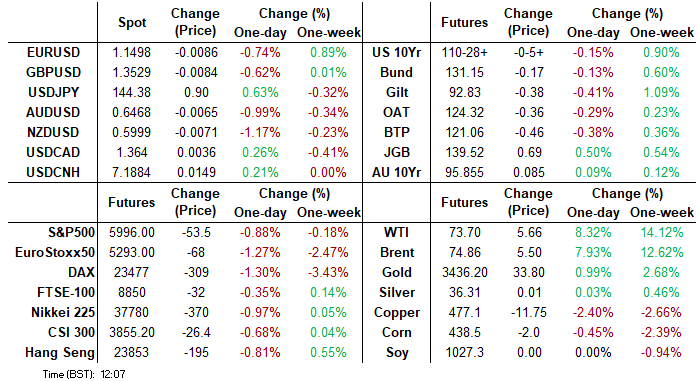

US TSYS: Sharper Sell-Off As US Filters In, TYA Away From Key Resistance

- Treasuries have seen pushes lower with US desks filtering in, for a sharper extension of the paring of early overnight sizeable gains seen initially on Israel strikes on Iran. Strikes are reportedly ongoing, including further strikes on nuclear facilities.

- WTI futures are off overnight highs but have climbed strongly for the past three hours, currently +9%.

- All major benchmarks are now a little lower on the day, with cash yields circa 1.5bp higher across the curve.

- Treasuries see relative outperformance to European FI: with 10Y yields +1.2bps vs +5bp for Gilts, +5-5.5bp for peripherals, +3.7bp for OATs and +2.1bp for Bunds. This relative haven flow is echoed in the USD index.

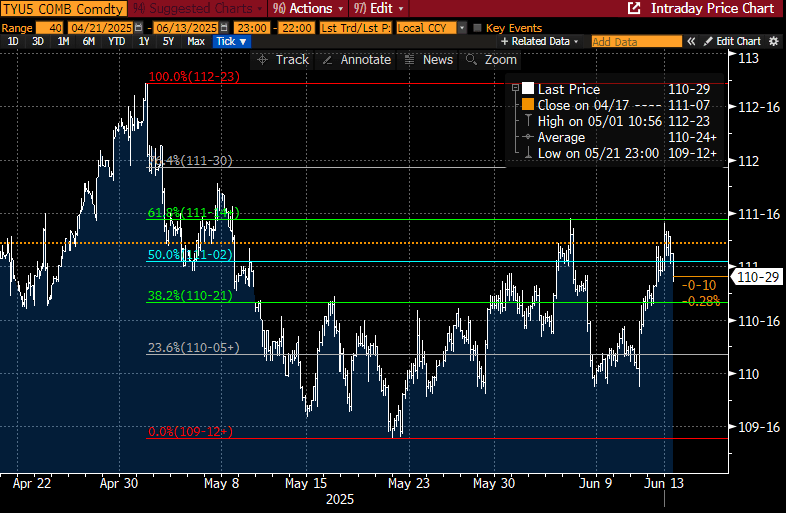

- 10Y yields are currently 4.371% (+1.2bp) having lifted firmly from an overnight low of 4.3082%. The 4.30% level equated to 111-14 for TYU5.

- TYU5 has recently hit session lows of 110-27+ (- 06+) before lifting a couple ticks, after an overnight high of 111-13. There have been large cumulative volumes of 710k.

- The earlier high stopped just short of a key short-term resistance at 111-14+ (Jun 5 high and 61.8% retrace of May 1-22 downleg). Clearance would be bullish with next resistance at 111-20 (1.0% 10-dma envelope). Support meanwhile is seen at 110-17+ (20-day EMA) before 109-28 (Jun 6/11 lows).

- Data: U.Mich consumer survey Jun prelim (1000ET)

- Trump attends a National Security Council Meeting at 1100ET - closed press.

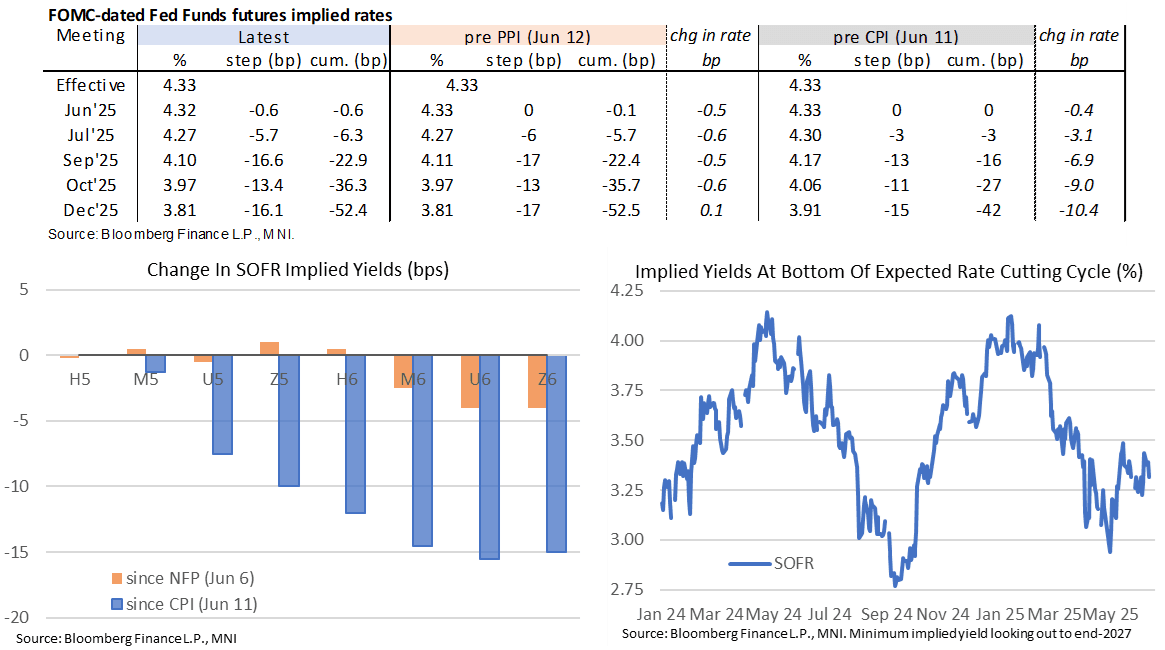

STIR: Fed Rates Fully Reverse Initial Dovish Reaction To Israel Strikes

- Fed Funds implied rates are back to near unchanged overnight for 2025 meetings, having reversed a 5bp push lower for the Dec’25 on Israel strikes in Iran.

- The reversal has been seen across US and European fixed income markets. WTI futures are off highs but currently +8.4%.

- It leaves a rate path back at pre-PPI levels although Wednesday’s soft CPI still sets the tone for the week, with a path firmly off what had been close to the most hawkish levels since February.

- Geopol headlines will likely dominate proceedings today before some data focus with the June preliminary U.Mich consumer survey at 1000ET.

- Cumulative cuts from 4.33% effective: 0.5bp Jun (next Wed), 6.5bp Jul, 23bp Sep, 36.5bp Oct and 52.5bp Dec.

- The SOFR implied terminal yield of 3.28% (SFRZ6) is +2bp on the day after a 7.5bp intraday lift.

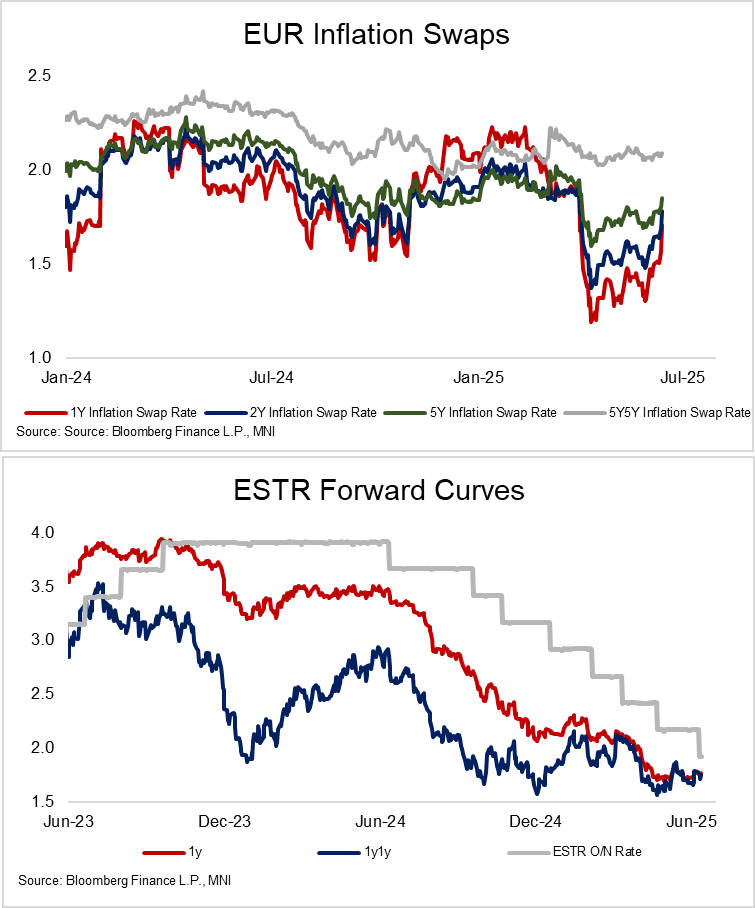

ECB: Modest Rise In EUR 5y5y Inflation Swaps On Middle East Tensions

Today’s spike higher in brent crude and natural gas futures has had a modest impact on long-term EUR inflation swaps. The 5y5y swap is up 2bps to 2.0950%, with the bulk of the upside move concentrated in shorter-dated swaps. That’s still contributed to a light hawkish move in ESTR forward rates though, with the 1y1y rate up 4bps to 1.75% on the session.

- For the Eurozone inflation outlook and therefore the ECB reaction function, the most important risk to monitor is whether the latest escalation of Middle East tensions impacts actual global oil/gas supply or disrupts key shipping routes in the region. It’s too early to make firm conclusions on that front right now.

- Energy price volatility can have a meaningful impact on the ECB’s headline inflation projections (most recently to the downside in the June forecast round), but the Governing Council is generally happy to look through such changes if they are short-term in nature.

- However, if increases in energy prices become more persistent and exhibit supply shock dynamics, the bar to a Governing Council response may be lower than in the previous decade (e.g. prior to Covid and the Russia-Ukraine invasion). ECB President Lagarde’s recent speech on the ECB’s ongoing strategy assessment discusses these trade-offs in more detail (see here).

- In its June macroeconomic projections (here), the ECB conducted its regular sensitivity analysis on the baseline projections to changes in energy price assumptions. The conclusion was that “alternative paths for oil and gas commodity prices suggest risks for inflation are overall tilted to the upside”. These upside risks were mostly related to gas prices, with the oil market risks more balanced.

MIDEAST: Iran Launches Retaliatory Drone Wave Following Israeli Strikes

Reuters reports that, according to the US State Department, the US Embassy (likely in Amman) has "indications there may be missiles, drones, or rockets flying over Jordanian airspace". There have been numerous reports over the past hour that Iran has launched at least a first wave of ~100 retaliatory drones/missiles against Israel following the overnight attacks on nuclear and political sites and key military commanders and scientists.

- AP reported that the Israeli military has said it has begun intercepting Iranian drones following Israel's strikes on Iran overnight. Israeli public broadcaster KAN reports that Israel has intercepted drones over Saudi Arabia, as does Channel 12. Jordanian state news reports that the country's military have intercepted drones and missiles in its airspace this morning.

- A response of this scale was always likely, and given the scope of Israel's Iron Dome air defences, as well as those of Jordan and Israeli allies with military deployments in the region, such as the US and UK, this wave is unlikely to cause significant trouble for Israel. Iranian Supreme Leader Ayatollah Ali Khamenei has said Israel will face a 'severe punishment' for the attacks.

SOFR: Net Long Setting Dominated In Futures On Thursday

OI data points to net long setting dominating through the SOFR greens on Thursday, with only 4 of the front 12 contracts seemingly subjected to some form of net cover.

- Net short cover was slightly more prominent in the blues.

| 12-Jun-25 | 11-Jun-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,068,294 | 1,062,905 | +5,389 | Whites | +7,098 |

SFRM5 | 1,412,211 | 1,425,597 | -13,386 | Reds | +42,666 |

SFRU5 | 1,151,529 | 1,164,539 | -13,010 | Greens | +11,049 |

SFRZ5 | 1,185,833 | 1,157,728 | +28,105 | Blues | -2,066 |

SFRH6 | 931,776 | 919,419 | +12,357 |

|

|

SFRM6 | 882,220 | 866,093 | +16,127 |

|

|

SFRU6 | 786,849 | 789,722 | -2,873 |

|

|

SFRZ6 | 871,017 | 853,962 | +17,055 |

|

|

SFRH7 | 664,755 | 655,427 | +9,328 |

|

|

SFRM7 | 598,053 | 596,249 | +1,804 |

|

|

SFRU7 | 432,539 | 430,124 | +2,415 |

|

|

SFRZ7 | 403,190 | 405,688 | -2,498 |

|

|

SFRH8 | 306,747 | 306,638 | +109 |

|

|

SFRM8 | 211,427 | 214,135 | -2,708 |

|

|

SFRU8 | 171,103 | 169,464 | +1,639 |

|

|

SFRZ8 | 166,669 | 167,775 | -1,106 |

|

|

US TSY FUTURES: Net Long Setting Dominates Again On Thursday

OI data points to a second consecutive day of meaningful net long setting across the curve on Thursday, with the curve-wide DV01 equivalent build in net longs rising by ~$5mln when compared to Wednesday levels, to $11.7mln.

- TY & UXY saw the most meaningful net long additions on the day.

| 12-Jun-25 | 11-Jun-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 3,985,761 | 3,965,750 | +20,011 | +786,515 |

FV | 6,861,317 | 6,820,251 | +41,066 | +1,794,063 |

TY | 4,803,528 | 4,741,625 | +61,903 | +4,116,498 |

UXY | 2,345,867 | 2,316,146 | +29,721 | +2,608,189 |

US | 1,737,042 | 1,721,915 | +15,127 | +2,146,498 |

WN | 1,895,172 | 1,893,634 | +1,538 | +283,950 |

|

| Total | +169,366 | +11,735,712 |

BONDS: /STIR: Markets Look To Inflationary Impact Of Higher Oil Prices

Note that EUR & GBP traded inflation metrics have moved higher today, providing a source of pressure for core global FI markets, as longer-term upside risks to oil pricing come to the fore and the initial risk-off impulse from the Israeli offensive against Iran fades from extremes

- Accordingly, year-end ECB pricing is ~2.5bp less dovish on the day, while end of year BoE pricing is ~5bp less dovish, at least partly reflecting the increased inflationary risk (there was also a flow element surrounding the higher Euribor fix to factor in as well).

FOREX: USD Further in Favour Through NY Crossover

- Dollar finding further support headed into the NY crossover, helping pressure EUR/USD through the overnight low and extend the backtrack from yesterday's high to over 125 pips.

- We note above that a broader bullish EUR theme remains intact, however a sharper sell-off from here could prompt a further liquidation of longs (data from June 3rd shows EUR net long holding close to 12-month highs) and a break of 1.1389, the 20-day EMA, could trigger momentum selling and a S/T correction. Today's price action suggests any material pick-up in geopolitical tensions via an official Iranian response, or via disruption of shipping through the Red Sea, would prove supportive of the USD again.

- While EUR was the key beneficiary to USD weakness yesterday, it is among today's poorest performers (after risk-led AUD, NZD), prompting EUR/GBP to fade off yesterday's June high despite backtracking ECB pricing for 2025.

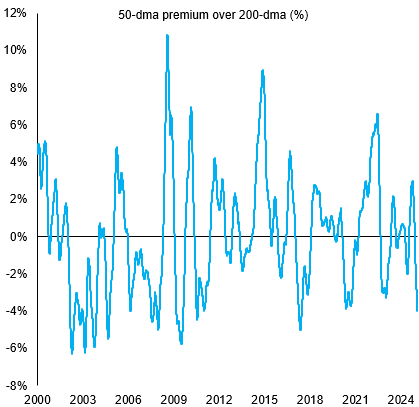

FOREX: USD Rally Poses Little Threat to Broader Downtrend

- Having underperformed all week - the dollar is benefiting from the risk-off, rally in oil prices and downtick in equities following the Israeli strikes on Iran. Resultantly, the USD Index is back above 98.00, but the bounce remains shallow: prices are already fading, and failed to top yesterday's high - let alone the levels of the first half of the week.

- As such, the broader downtrend holds firm, with the downtrendline drawn off the early February highs (today at 99.235) under very little threat from this dollar bounce.

- This leaves S/T momentum still pointed lower for the USD Index. The 50-dma premium over the 200-dma is now matching the most negative levels seen through COVID in 2020 - meaning the greenback is still trading through an acute phase of downward momentum only seen ~9 times since the year 2000 (see chart below).

- Today's bounce affirms the sell-on-rallies theme that's becoming evident in GBP/USD, however. The pair has pierced 1.36 on three occasions this month, and failed to materially build a base above.

Source: Bloomberg Finance L.P. / MNI

CROSS ASSET: Short USD Remains Most High Conviction Trade In Latest BofA Survey

Bank of America note that respondents to their latest FX & Rates Sentiment Survey “remain ambivalent on U.S. duration vs. Europe. But they do not hesitate to extend their USD shorts, even with short USD clearly perceived as the most crowded trade”.

- They go on to highlight that “USD positioning continues to lag bearish sentiment, with short USD remaining this year's highest conviction trade. This is consistent with survey respondents anticipating trade uncertainty to stabilize at high levels and U.S. exceptionalism to fade, and many preferring to lower their effectively unhedged U.S. asset exposure”.

- Looking ahead, the survey suggests that “growing U.S. fiscal concerns could add more pressure on USD, and so perhaps could - the not particularly high - fiscal hopes in Europe. However, U.S. data resilience could save the day for USD”.

- All in all, the survey generally underscores well-documented prevailing market themes.

OPTIONS: Expiries for Jun13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400-05(E1.7bln), $1.1485-00(E2.0bln)

- USD/JPY: Y144.00($1.3bln)

- EUR/GBP: Gbp0.8475(E902mln)

EQUITIES: E-Mini S&P Pierce Support at 20-Day EMA

- Today’s move down in the Eurostoxx 50 futures contract has resulted in a breach of the 50-day EMA at 5298.00. Price has also pierced 5255.00, the May 23 low. A clear break of both support points would highlight a short-term top and signal scope for a deeper retracement. This would open 5178.00, the May 6 low and 5081.16, a Fibonacci retracement. Initial resistance to watch is 5374.40, the 20-day EMA.

- The trend condition in S&P E-Minis remains bullish and the contract traded to a fresh cycle high on Wednesday, reinforcing current bullish conditions. For now, today’s pullback is considered corrective. The contract has pierced support at 5933.69, the 20-day EMA. A clear breach of this average would expose the 50-day EMA, at 5825.83. Key short-term resistance has been defined at 6074.75, the Jun 11 high.

COMMODITIES: WTI Futures Rally Sharply, Continuation Would Expose $80 Handle

- WTI futures have traded sharply higher this week and today's rally marks an acceleration of the current bull phase. Price action is likely to be volatile and from a technical standpoint, the trend is currently in an extreme overbought position. A continuation higher would expose the $80.00 handle. Initial support lies at $71.50, the Apr 2 high. A firmer support is noted at today’s intraday low - at $68.49.

- A bullish theme in Gold remains intact and this week’s gains reinforce bullish conditions. Medium-term trend signals are bullish too - moving average studies are in a bull-mode position, highlighting a dominant uptrend. Resistance at $3435.6, the May 7 high, has been pierced. A clear break of this level would strengthen bullish conditions and open $3500.1, the Apr 22 all-time high. Initial key support to monitor is $3255.2, the 50-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 13/06/2025 | 1230/0830 | ** | Monthly Survey of Manufacturing | |

| 13/06/2025 | 1230/0830 | ** | Wholesale Trade | |

| 13/06/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 13/06/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 13/06/2025 | 1500/1700 | ECB Elderson At Senior Supervisor's Conference | ||

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 13/06/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |