ECB: Modest Rise In EUR 5y5y Inflation Swaps On Middle East Tensions

Jun-13 11:02

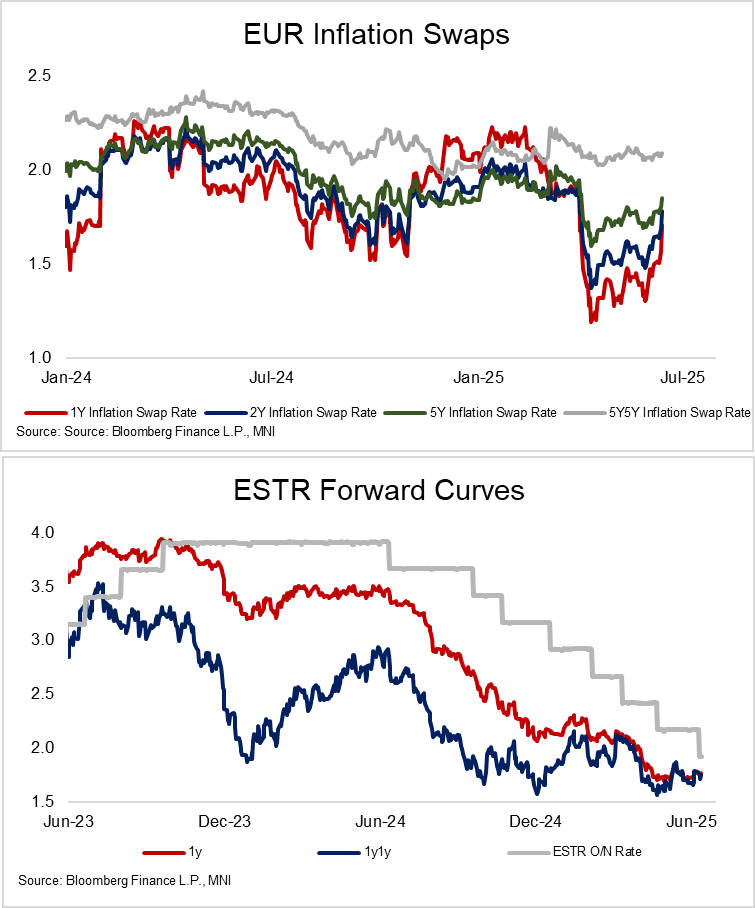

Today’s spike higher in brent crude and natural gas futures has had a modest impact on long-term EUR inflation swaps. The 5y5y swap is up 2bps to 2.0950%, with the bulk of the upside move concentrated in shorter-dated swaps. That’s still contributed to a light hawkish move in ESTR forward rates though, with the 1y1y rate up 4bps to 1.75% on the session.

- For the Eurozone inflation outlook and therefore the ECB reaction function, the most important risk to monitor is whether the latest escalation of Middle East tensions impacts actual global oil/gas supply or disrupts key shipping routes in the region. It’s too early to make firm conclusions on that front right now.

- Energy price volatility can have a meaningful impact on the ECB’s headline inflation projections (most recently to the downside in the June forecast round), but the Governing Council is generally happy to look through such changes if they are short-term in nature.

- However, if increases in energy prices become more persistent and exhibit supply shock dynamics, the bar to a Governing Council response may be lower than in the previous decade (e.g. prior to Covid and the Russia-Ukraine invasion). ECB President Lagarde’s recent speech on the ECB’s ongoing strategy assessment discusses these trade-offs in more detail (see here).

- In its June macroeconomic projections (here), the ECB conducted its regular sensitivity analysis on the baseline projections to changes in energy price assumptions. The conclusion was that “alternative paths for oil and gas commodity prices suggest risks for inflation are overall tilted to the upside”. These upside risks were mostly related to gas prices, with the oil market risks more balanced.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US MBA: MARKET COMPOSITE +1.1% SA THRU MAY 09 WK

May-14 11:00

- MNI: US MBA: MARKET COMPOSITE +1.1% SA THRU MAY 09 WK

EQUITIES: Credit Agricole Put Option

May-14 10:56

XCA (20th June) 14p, sold at 0.03 and 0.06 in 6.5k.

US TSYS: Modestly Firmer In A Thin Docket Before A Busy Thursday

May-14 10:50

- Treasuries are slightly firmer overnight, more comfortably back in the middle of yesterday’s range awaiting fresh drivers.

- It’s a thin data docket today (just weekly mortgage data) which sees Fed Vice Chair Jefferson in a little more focus at 0910ET, and with an eye on tomorrow’s April reports for US PPI and retail sales amongst others.

- US President Trump flies from Saudi Arabia to Qatar today.

- Cash yields are 0.5-1.5bp lower on the day, with declines led by the belly.

- TYM5 sits at 110-06+ (+ 07+) as it lifts a little more off yesterday’s latest lows of 109-30, on modest cumulative volumes of 280k.

- Technicals point to a bear mode condition, having most recently cleared support at 110-01+ (76.4% retrace of Apr 11 – May 1 bull leg) in a step closer to key support at 109-08 (Apr 11 low).

- Data: MBA mortgage applications (0700ET)

- Fedspeak: Jefferson (0910ET), Daly (1740ET) – see STIR bullet

- Bill issuance: US Tsy to sell $60bn 17-w bills (1130ET)

Related bullets

Related by topic

EUR/USD

Bunds

Germany

Euribor

European Central Bank

Schatz

Bobl