MNI US MARKETS ANALYSIS - NZD Leads as Inflation Exp. Rise

Highlights:

- US President Donald Trump says he will meet with Russian President Vladimir Putin "as soon as we can set it up".

- NZD remains the strongest performer in G10 following the release of inflation expectations data which shifted higher.

- Import prices, building permits and preliminary UMich sentiment & inflation expectations highlight the US calendar. We may also hear from SNB President Schlegel.

US TSYS: Erasing Week's Drop to Mid-April Levels

- Treasuries gained with EGBs overnight, currently running near the top end of the range - as rates return to early Monday levels. As with EGBs, there doesn't appear to be any obvious headline driver as markets continue to digest Thursday's PPI.

- Treasury Jun'25 10Y contract trades +8.5 at 110-16.5 last vs. 110-20 high, initial technical resistance at 110-27 (20-day EMA). Key near-term resistance has been defined at 111-22, the May 7 high. A move above this level is required to signal a potential reversal.

- Curves mildly mixed, 2s10s -.517 at 46.134, 5s30s +.804 at 83.750, 10Y yield -.0255 at 4.4060%.

- Overnight volumes climbing as Jun/Sep quarterly futures roll continues. Percentage complete still low at approximately 5% with September futures taking lead on May 30.

- Cross asset roundup: Bbg US$ index softer/off lows at 1229.19 (-.84), Gold falling to 3176.0 - stilloff yesterday's3128.98 low (Apr 10 lvl), crude mildly higher (WTI +.26 at 61.88).

- Focus turns to Friday's data: Housing Starts, Building Permits, Import/Export Prices at 0830ET; U. of Mich. Sentiment at 1000ET followed by TIC Flow data at 1600ET.

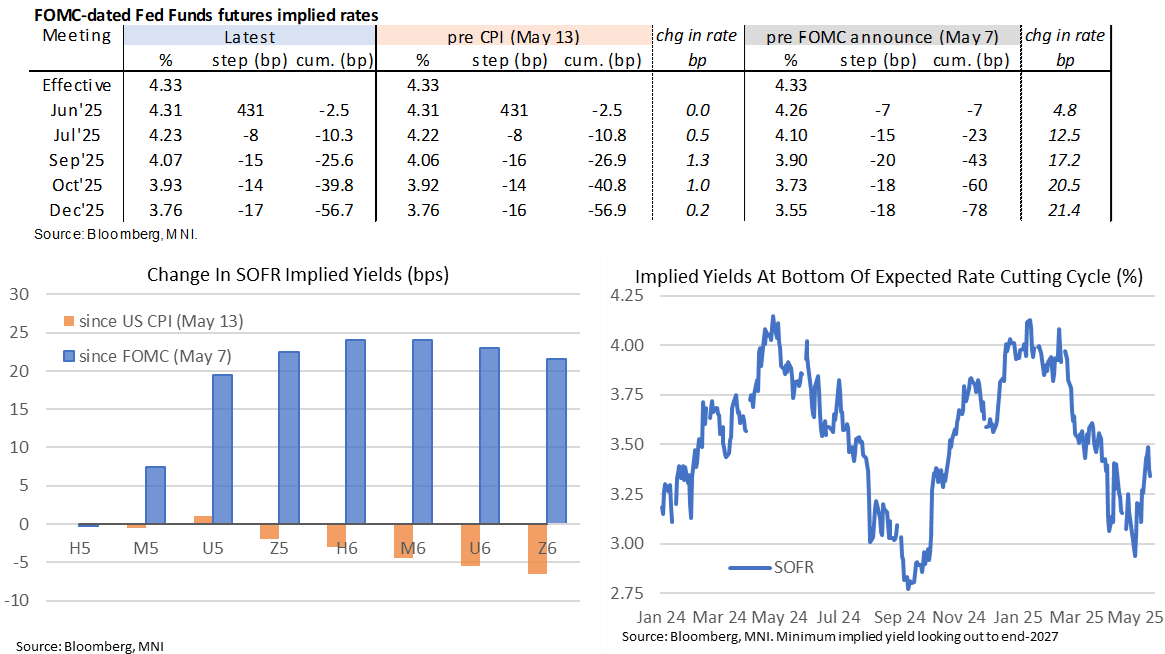

STIR: Next Fed Cut Seen in September, U.Mich and Import Prices Ahead

- Fed Funds implied rates have pared overnight dovish moves to leave them unchanged, consolidating yesterday’s shift away from hawkish extremes for the post-reciprocal tariff period.

- Cumulative cuts from 4.33% effective: 2.5bp Jun, 11bp Jul, 25.5bp Sep, 39bp Oct and 55bp Dec.

- Rates see larger rallies further out the curve though, with the SOFR implied terminal yield 3.5bp lower on the day at 3.34% (SFRZ6), i.e. circa 100bp of cuts from current effective levels.

- Today’s data focus is likely on import prices for April (0830ET) and the preliminary U.Mich consumer survey for May (1000ET).

- Import prices will as always have scope for some marginal tweaks to core PCE estimates, which look to be centering around 0.13% M/M after CPI and PPI.

- The preliminary U.Mich survey will have been collected Apr 22-May 13 leaving little time for the US-China de-escalation in trade tensions on May 12 to have filtered through. The full release for April showed that end-of-survey readings had fallen following the Apr 9 90-day tariff partial pause but were still higher than the month average, which could scope for 1Y inflation expectations higher than the 6.5% in April.

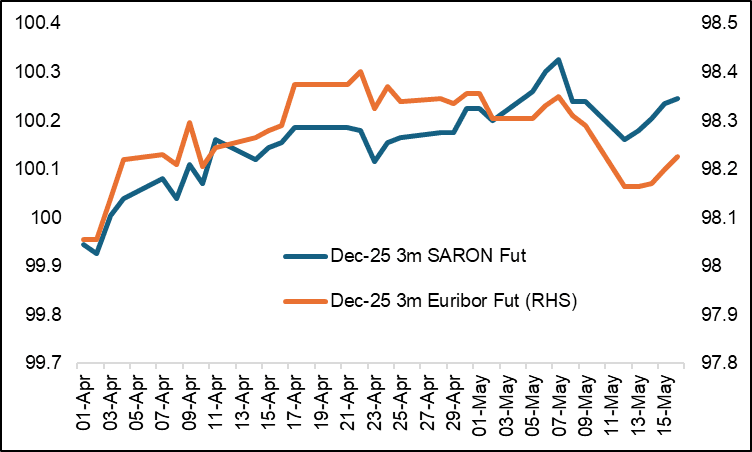

STIR: Markets Shrugged Off Strong GDP/IP Ahead of Schlegel

Dovish moves in EUR FI have filtered through to Franc-denominated markets over the last three days despite strong activity data in Switzerland - strengthening the narrative that markets view the SNB as more concerned with its inflation and FX outlook than immediate growth worries.

- CHF OIS markets currently price 48bp of easing through Dec - up from 37bp on Tuesday (hawkish extreme after Monday's US/China tariff reprieve). For the upcoming June SNB meeting, markets imply around a 1/5 chance of an outsized 50bp cut to -0.25%.

- While today's Q1 Swiss IP data underscored that the sector likely benefited strongly from US tariff-front running in the pharma sector, yesterday's Swiss Q1 flash GDP reading mentioned that the 0.7% Q/Q figure was "driven significantly by the services sector", limiting the threat for an outsized pharma-driven reversal in Q2.

- SNB Chairman Schlegel is scheduled to hold a speech at 1200BST titled "trade war and geopolitical upheaval: Monetary policy in times of uncertainty". Most interesting would be any update on his recent commentary that the Swiss Franc has "really appreciated a lot".

STIR: Net Long Setting Dominated After PPI Data

OI data suggests that net long setting dominated in most SOFR futures through the blues on Thursday, as softer-than-expected PPI data (and the readthrough for the Fed’s preferred PCE inflation gauge) promoted fresh dovish flows.

- A reminder that most contracts were trading just off the most hawkish levels seen since March/April ahead of the data, owing to the moderation in Sino-U.S. trade tensions seen over the weekend/early Monday.

| 15-May-25 | 14-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,032,945 | 1,032,716 | +229 | Whites | +39,537 |

SFRM5 | 1,212,783 | 1,214,375 | -1,592 | Reds | +15,285 |

SFRU5 | 1,084,372 | 1,049,704 | +34,668 | Greens | +17,963 |

SFRZ5 | 1,128,811 | 1,122,579 | +6,232 | Blues | +1,290 |

SFRH6 | 783,860 | 763,875 | +19,985 |

|

|

SFRM6 | 758,057 | 755,777 | +2,280 |

|

|

SFRU6 | 745,326 | 745,647 | -321 |

|

|

SFRZ6 | 860,654 | 867,313 | -6,659 |

|

|

SFRH7 | 686,078 | 679,175 | +6,903 |

|

|

SFRM7 | 584,834 | 581,445 | +3,389 |

|

|

SFRU7 | 376,289 | 371,858 | +4,431 |

|

|

SFRZ7 | 397,687 | 394,447 | +3,240 |

|

|

SFRH8 | 263,003 | 258,976 | +4,027 |

|

|

SFRM8 | 187,909 | 188,624 | -715 |

|

|

SFRU8 | 151,507 | 154,262 | -2,755 |

|

|

SFRZ8 | 164,219 | 163,486 | +733 |

|

|

RUSSIA: Delegations Meet in Istanbul in 1st Direct Diplomatic Contact Since 2022

Wires reporting that the Russian and Ukrainian delegations tasked with the first direct talks between the two warring nations since 2022 have met in Istanbul, Turkey. Before this, the Russian delegation met with officials from the US. Vladimir Medinsky, who is leading the relatively junior Russian delegation, has arrived at the talks venue according to wire reports. Ukraine, which has sent a much higher-ranking delegation led by Defence Minister Rustem Umerov, said ahead of the meeting that Kyiv is ready for “direct negotiations at the highest level” and a “complete and unconditional ceasefire.”

- Given the lack of high-level participation (on the Russian side at least) it remains to be seen how much progress will be possible in today's talks. There has been some hope from Ukraine and its European allies that Putin's failure to turn up in Turkey while Ukraine's Volodymyr Zelenskyy was present could draw the ire of the US, and raise the prospect of Washington, D.C., backing harsher sanctions. However, this is yet to materials.

- Earlier, Kremlin spox Dmitry Peskov talked to reporters. Regarding US President Donald Trump's comments, calling for a meeting with Russian President Vladimir Putin "as soon as we can set it up", Peskov says such a meeting "requires advance preparation and must yield results" adding "such a meeting is essential for US-Russia ties" but that the aforementioned preparation can be "lengthy". Says it is "hard to overestimate the importance of Trump-Putin contacts" in the context of Ukraine.

US: Summary of Trump's Comments in UAE

US President Donald Trump has delivered remarks to the press in Abu Dhabi, on a range of issues, to conclude his “incredible” four-day trip to the Middle East.

- Trump says he will go straight home after his stop in the UAE, nixing the possibility of an additional stop in Turkey to help facilitate peace talks between Ukraine and Russia. He says, “we’ll see what happens with Russia and Ukraine…”

- Trump later adds on a ceasefire, “we’re going to get it done” and says he will meet with Russian President Vladimir Putin "as soon as we can set it up".

- Trump hints at some foreign policy announcements in the coming 2 or 3 weeks, noting: “We’re looking at Gaza and we’re going to get that taken care of”. While discussion of Israel has been conspicuously absent from Trump's trip, Secretary of State Marco Rubio held a call with Prime Minister Netanyahu yesterday, affirming the US' 'ironclad' support for Israel's security.

- Trump says, “we have an Iran situation” adding that “one way or another we’ll take care of it”. He repeats an ultimatum to Tehran he delivered in Riyadh on Tuesday: “Either it’ll be done nicely or not nicely”.

- He adds that “we’re talking to [Iran] and I think they’ve come a long way” but declines to provide any new details on the status of talks following reports yesterday that the US had submitted a formal nuclear proposal for the first time since talks resumed in April.

- Trump notes a deal with the UAE to buy Boeing planes, following a similar deal with Qatar. Trump says details of a $1.4 trillion UAE investment in the US will be announced shortly.

- He says that the US and UAE agreed to “create a path” for the UAE to buy “some of the most advanced AI semiconductors” from American companies. The prospective deal has raised some concerns in Congress about China gaining access to US chip technology through the deal.

- Trump notes recent “trade deals” with the UK and China, says “we have 150 countries that want to make a deal… So over the next two-three weeks [Treasury Secretary Scott Bessent and Commerce Secretary Howard Lutnick] will be sending letters out telling people what they’ll be paying to do business in the US.”

- Trump adds: “I guess you could say they could appeal it, but for the most part I think we’ll be very fair.”

MNI POLITICAL RISK ANALYSIS: Portugal Election Preview

- Portugal holds a snap legislative election on 18 May following the successful parliamentary vote of no confidence against the minority government of Prime Minister Luís Montenegro in March. A fractured political landscape makes one party winning a majority in the Assembly of the Republic an unlikely scenario.

- As such, the formation of a coalition or minority government after the election is set to be required. There is significant focus on the post-election negotiations, given the prospect that the right-wing Chega is involved in supporting a minority administration for the first time.

- In this preview we include a brief background on why the snap election is taking place now, an explainer on the main political parties contesting the vote and how the electoral system works, analysis of post-election scenarios with assigned probabilities, an outlook for financial markets, and a chartpack of opinion polling and betting market data.

MNI POLITICAL RISK ANALYSIS: Poland Election Preview

- Poland will hold the first round of the presidential election on May 18, with the widely anticipated run-off between top two candidates expected on June 1. The head of state has many ceremonial functions, but is also equipped with a strong veto power, with the bar for its overruling by parliament set relatively high.

- Opinion polling and betting market data suggest that government ally Rafał Trzaskowski holds a lead over his closest rival Karol Nawrocki. Trzaskowski’s victory would give the government more leeway to implement its agenda, while Nawrocki’s win would prolong the existing political deadlock. Exit polls after the first round will be published once the election silence period expires alongside the closure of polling stations at 20:00BST/21:00CEST.

- In this election preview, we provide a briefing on how the election works and the broader political backdrop of this particular poll, a list of main candidates, a scenario analysis examining the probabilities and implications of various outcomes, alongside latest opinion polling and betting market data ahead of the vote.

RATINGS: Updates on Portugal & Greece Eyed After Close

Potential sovereign credit rating reviews of note scheduled for after hours on Friday include:

- Fitch on Greece (current rating: BBB-; Outlook Stable), Luxembourg (current rating: AAA; Outlook Stable) & Slovakia (current rating: A-; Outlook Stable)

- Moody’s on Malta (current rating: A2; Outlook Stable) & Portugal (current rating: A3; Outlook Stable)

- S&P on Cyprus (current rating: A-; Outlook Stable) & South Africa (current rating: BB-; Outlook Positive)

- Morningstar DBRS on the United Kingdom (current rating: AA, Stable Trend)

- Scope Ratings on Portugal (current rating: A; Outlook Stable) & Slovenia (current rating: A; Outlook Stable)

Most of the focus is likely to fall on the Greek and Portuguese updates from Fitch & Moody’s, respectively. We previously outlined the potential for positive action from Moody’s on Portugal in our political risk team’s election preview (vote due this weekend), click for that document. Please use this link to access the indicative sovereign rating review schedule covering the five most notable rating agencies for 2025. Note that this schedule is indicative only and ratings can be reviewed on an ad-hoc basis. Rating agencies may also adjust their schedules during the year.

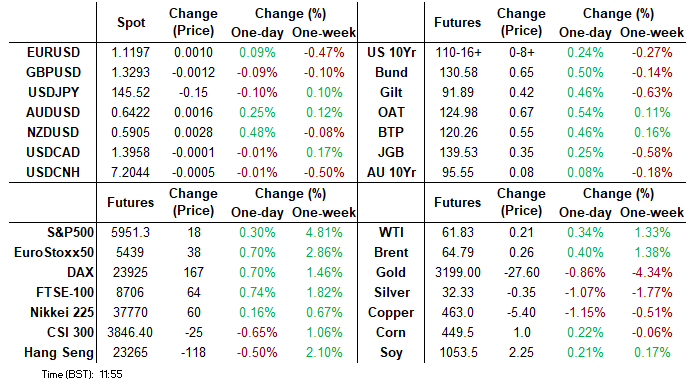

FOREX: NZD Remains Outperformer as Inflation Expectations Shift Higher

- The New Zealand dollar remains the strongest performer in G10, following the release of inflation expectations data which has shifted higher in the latest RBNZ survey. The 2yr ahead expectations rose to 2.29%, from 2.06% in Q1. Expectations had been near 2.0% (the mid-point of the RBNZ band) since Q3 last year. We are still well off late 2022 cycle highs of 3.62%, but at face value this isn't a welcome development from an RBNZ standpoint.

- NZDUSD (+0.53%) has regained the 0.5900 handle in sympathy, although remains well shy of the week’s high at 0.5969. Solid support for the pair is buildig around the 0.5850 mark.

- The other notable move in G10 was for USDJPY, which finally bridged the gap to last Friday’s close overnight. Some downside momentum picked up following the moves below 145.37, gravitating to a low print at 144.92 before stabilising. Thepair remains broadly unchanged on the week despite the volatile intra-day ranges. Overall, the latest USDJPY pullback underpins the view that gains since Apr 22 appear corrective.

- Elsewhere, ranges across global currency markets have remained contained, as markets continue to digest the plethora of data releases on Thursday, and the data calendar remains relatively calm to end the week.

- As such EURUSD is a tad firmer on the session, consolidating just above 1.12, while GBPUSD is doing the same above 1.33. For cable, Tuesday’s gains highlight a possible reversal pattern - a bullish engulfing candle. If correct, the pattern signals the end of the corrective cycle and a resumption of the uptrend. A continuation higher would refocus attention on the key resistance and a bull trigger, at 1.3444, the Apr 28 / 29 high.

- Import prices, building permits and preliminary UMich sentiment & inflation expectations highlight the US calendar. We may also hear from SNB President Schlegel.

EQUITIES: This Week's Gains Bolster Bullish Outlook for Eurostoxx Futures

- A bullish theme in Eurostoxx 50 futures remains intact. Gains this week reinforce current bullish conditions. The contract is extending the recent breach of 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. The continuation higher signals scope for a climb towards 5516.00, the Mar 3 high and the key bull trigger. Initial firm support to watch lies at 5171.52, the 50-day EMA. Clearance of this level would signal a possible reversal.

- A bullish trend condition in S&P E-Minis remains intact and this week’s appreciation reinforces current conditions. Price also continues to trade at its latest highs. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5669.26, the 50-day EMA.

COMMODITIES: Corrective Cycle in Gold Remains in Play

- A downtrend in WTI futures remains intact and recent gains are considered corrective. Key resistance to watch is $63.46, the 50-day EMA. It has recently been pierced, a clear break of it would highlight a stronger reversal. This would open $66.41, the Apr 4 high. For bears a reversal lower would refocus attention on $54.67, the Apr 9 low and bear trigger. Clearance of this support would confirm a resumption of the downtrend.

- A corrective cycle in Gold remains in play and the metal has traded lower this week. A key support at $3202.0, the May 1 low has been breached. The break of this level signals scope for a deeper retracement, towards $3085.0, 76.4% of the Apr 7 - Apr 22 upleg. Note that the 50-day EMA at $3168.0, has been breached, strengthening a bearish threat. Initial resistance is $3265.4, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 16/05/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 16/05/2025 | 1230/0830 | New York Fed's Roberto Perli | ||

| 16/05/2025 | 1230/0830 | *** | Housing Starts | |

| 16/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 16/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 16/05/2025 | 1500/1700 | ECB's Lane On Central Bank Communication Panel | ||

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 16/05/2025 | 2000/1600 | ** | TICS | |

| 16/05/2025 | 0140/2140 | San Francisco Fed's Mary Daly |