MNI US MARKETS ANALYSIS - New Phase of Govt Shutdown Risk

Highlights:

- Markets enter new phase of shutdown risks, House could vote on funding package as soon as today

- Metals sell-off slows, but second order risks remain with price 30% off last week's high

- Manufacturing ISM in focus ahead of labor market data at end of the week

US TSYS: TYH6 Corrective Bounce Has Extended, Tsy Borrowing Estimates Ahead

Treasuries are firmer across the curve, with a tailwind from heavy declines in crude futures (1st WTI -5.2%) after President Trump said Iran was "seriously talking" with Washington while the underlying market narrative remains bearish due to a projected surplus. Volumes have been elevated overnight in what also likely reflects reaction to Friday’s precious metals rout, a sector that remains under pressure today.

- Cash yields are 0.2-1.5bp lower, with declines led by 20s.

- Curves have pulled back from recent steeps, with 5s30s at 108.1bp (-0.6bp) after hitting 110.3bp overnight for its highest since Jan 13.

- TYH6 trades at 111-30+ (+04) on heavy overnight volumes of 605k, extending a corrective bounce.

- An earlier high of 112-02 cleared resistance at 111-31 (20-day EMA) to open 112-08+ (50-day EMA). Support is seen at 111-15+ (Jan 28 low) before the bear trigger at 111-09 (Jan 20 low).

- Data: S&P Global US mfg PMI Jan f (0945ET), ISM mfg Jan (1000ET)

- Fedspeak: Bostic moderated discussion at Atlanta Rotary Club (1230ET)

- Refunding: Borrowing estimates (1500ET) before Wednesday’s full QRA (0830ET). The prevailing expectation is that there will be no change to the guidance, but that was also the overwhelming expectation in the last refunding round which surprised with a tweak. MNI Refunding Preview: https://mni.marketnews.com/4tdj67E

- Bill issuance: US Tsy $89B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump participates in signing time (1530ET), House could vote on Senate funding package today or tomorrow in a move needed to end the partial government shutdown that started on Saturday

STIR: Close To Pricing Next Fed Cut In June, Mfg Surveys In Focus Today

- US rates have slightly extended Friday’s steady rally seen after President Trump announced Kevin Warsh as his pick for Fed chair.

- Trump joked during a speech Saturday night that he would sue Warsh if he didn't lower interest rates.

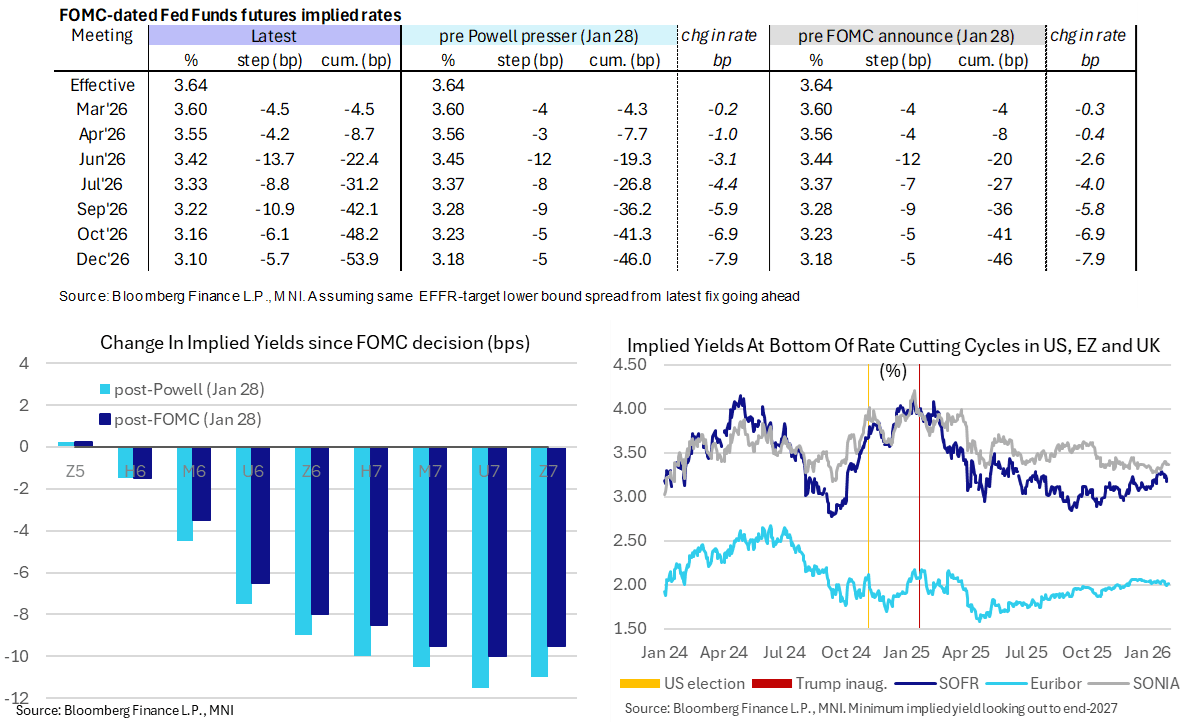

- Fed Funds implied rates for 2026 meetings are mostly only 0.5bp lower from Friday’s close, close to but not fully pricing a next cut in June under the new Fed chair.

- FF cumulative cuts from 3.64% effective: 4.5bp Mar, 8.5bp Apr, 22.5bp Jun, 31bp Jul, 42bp Sep, 48bp Oct and 54bp Dec.

- SOFR futures are 1.5 ticks firmer through 2027 contracts, with the terminal implied yield another 1bp lower at 3.165% (SFRZ6) for a fresh low since mid-Jan.

- Today’s macro focus is likely on manufacturing business surveys, with the final January PMI at 0945ET before the ISM release at 1000ET.

- The Fedspeak schedule is light with only Atlanta Fed’s Bostic (retiring Feb) in a moderated discussion at 1230ET (no text)

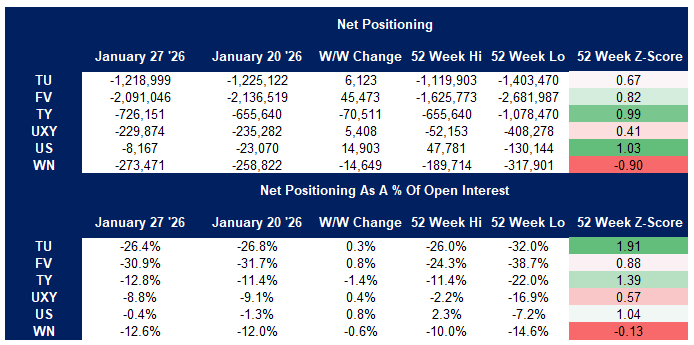

US TSY FUTURES: CFTC Shows Asset Managers Adding To Long, Funds Trim Short

The latest CFTC CoT report showed asset managers adding to their overall net long, as net long building in FV, TY & WN futures comfortably outweighed net long cover in TU, UXY & US futures. The cohort remains net long across the curve, with curve-wide DV01 exposure climbing by $16.4mln.

- Meanwhile, leveraged funds added to net shorts in TY & WN futures, while they lightened their net shorts in TU, FV, UXY & US futures. The cohort remains net short across the curve but lightened its curve-wide net short DV01 exposure by ~$3.1mln.

- The broader non-commercial cohort trimmed net shorts in TU, FV, UXY & US futures, while adding to net shorts across TY & WN futures. The cohort remains net short across all contracts, adding DV01 of $2.6mln net shorts across the curve (See table below for more details).

- A reminder that the survey covered the week ending January 27.

Source: MNI - Market News/CFTC/Bloomberg Finance L.P.

US TSY FUTURES: Long Cover In TY-US Zone Dominated On Friday

OI data points to a mix of net short cover (TU), long setting (FV), long cover (TY, UXY & US) and short setting (WN), with the net long cover in the TY-US zone providing the most meaningful adjustment (US futures saw a ~$6.6mln DV01 reduction in exposure).

- Markets had to adjust for risk-off flows stemming from a meaningful pullback in precious metals and news that President Trump had chosen Kevin Warsh as the next Fed Chair.

- While Warsh was deemed to be the most hawkish of the final candidates that were in the race for the role, his apparent credibility and wider risk aversion stemming from the move in metals allowed Tsys to recover from lows (leaving TU & FV higher on the day, even with PPI on the firm side), while his balance sheet preferences promoted curve steepening.

| 30-Jan-26 | 29-Jan-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,629,335 | 4,651,073 | -21,738 | -808,675 |

FV | 6,876,956 | 6,791,567 | +85,389 | +3,671,032 |

TY | 5,566,963 | 5,601,696 | -34,733 | -2,285,814 |

UXY | 2,624,601 | 2,632,594 | -7,993 | -711,902 |

US | 1,744,275 | 1,792,326 | -48,051 | -6,632,322 |

WN | 2,185,650 | 2,179,903 | +5,747 | +1,053,424 |

|

| Total | -21,379 | -5,714,256 |

SOFR: Net Long Setting Dominated In Futures On Friday

OI data points to net long setting dominating through the blue SOFR futures pack as most contracts ticked higher on Friday.

- Markets had to adjust for risk-off flows stemming from a meaningful pullback in precious metals and news that President Trump had chosen Kevin Warsh as the next Fed Chair.

- While Warsh was deemed to be the most hawkish of the final candidates that were in the race for the role, his apparent credibility and wider risk aversion stemming from the move in metals allowed Tsys and SOFR futures to recover from lows (even with PPI on the firm side), while his balance sheet preferences promoted Tsy curve steepening.

EUROPE ISSUANCE UPDATE

[ESM ISSUANCE] 10-year mandate:

- "The European Stability Mechanism has mandated BofA Securities, Natixis and Santander to joint lead manage a new EUR 10-year benchmark, maturing on the 25th February 2036. No further group." From market source

- MNI looks for a E2-3bln and we note the timing is not a surprise given an RFP was issued last week. We had thought a transaction today was slightly more likely than tomorrow, but now assume this will be tomorrow's business.

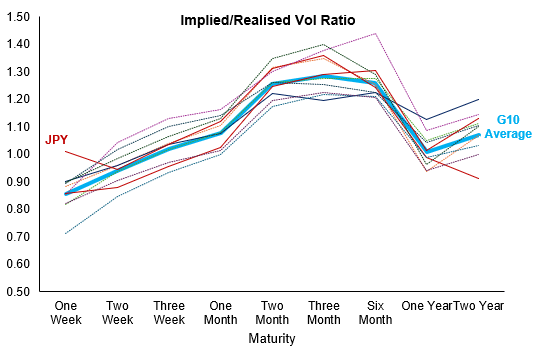

FOREX: JPY Vols Target Election as Metals Prices Stabilise

While spot gold and silver recovers off intraday lows (although still lower by 5% and 7% respectively) markets are generally steadier: the USD Index is holding the entirety of Friday’s rally, while USDJPY rallies continue to be sold. Even as Takaichi talked up the virtue of a weaker currency to stimulate exports, the overnight high of 155.51 was short-lived, keeping spot comfortably below the 50-dma of 156.32.

- Steadier spot metals markets are containing the record-setting run higher in implied vols in the space – although one-month silver vols still remain either side of 95 points (96.7 printed Friday, previous record high was 90.8 during the onset of COVID).

- Even as spot markets are more muted early Monday, the net result of has been a steepening of the front-end of the G10 FX vol curve (see below), with particular pressure seen across two- and three-month maturities.

- At the very front-end, JPY vol stands out: the one-week maturity now captures the lower house elections on February 8th, keeping implied vol well supported above 11 points to price a break-even on a one-week straddle of near 200 pips.

Figure 1: Very front-end of the implied curve isolates JPY into next week's elections

Source: MNI / Bloomberg Finance L.P.

FOREX: DXY Consolidates Recovery as Precious Metals Fragility Remains Focus

- The most recent action for G10 currencies has remained a sideshow to the aggressive moves seen in the precious metals space. Price action this morning saw spot silver extend its decline from last Thursday’s peak to as much as 41%, while gold followed suit in plummeting 20% at its worst point as positional dynamics have exacerbated sentiment.

- Key questions surrounding how Fed Chair appointee Warsh is planning to square a smaller balance sheet with lower rates, and expectations for the government shutdown to resolve this week, are helping the DXY consolidate around 1.7% off last week’s cycle lows.

- This is further dampening the recent enthusiasm for EURUSD, which after spiking to 1.2080 early last week, now finds itself trading in a more stable manner around 1.1850. The latest strengthening of the Euro (particularly against the dollar) has reignited downside inflation concerns amongst more dovish GC members, of interest ahead of this Thursday’s ECB.

- The weaker commodity complex, with oil also down 5%, did weigh on the likes of AUD and NZD to start the week, although both have stabilised across the European morning. Positioning dynamics will also be a consideration for AUD as we approach the RBA decision tomorrow, where surveyed analysts lean towards a 25bp hike.

- Elsewhere, markets pounced on latest remarks from PM Takaichi regarding the yen as we approach the Japanese election, where she stated a weak currency can be a major opportunity for export industries. USDJPY rose to 155.51 recovery highs before the weaker risk sentiment and a walking back of the rhetoric assisted a reversal back below 155.

- ISM Manufacturing will show if Friday's outperformance in the MNI Chicago PMI can be seen across the US. The February Refunding round starts today with the Treasury’s update on financing requirements; the full refunding will follow Wednesday.

OPTIONS: Clear of Sizeable Strikes Monday, But Decent Expiries Later This Week

With major pairs fading fast off last week's highs, EUR has quickly edged well back below some of the more sizeable strikes set to roll off at today's cut - possibly leaving markets less anchored into today's ISM Manufacturing print. Beyond today's NY cut, EUR sees solid interest into 1.1850 rolling off tomorrow, Wednesday and Thursday, while AUDUSD currently sits on a sizeable strike at 0.6950 expiring on Wednesday.

Today's expiries:

- EUR/USD: $1.1925(1.2bln), $1.2000(E3.6bln)

- USD/JPY: Y150.95-00($1.5bln), Y152.40-50($705mln), Y155.70($531mln)

- USD/CAD: C$1.3500($838mln)

- USD/CNY: Cny6.8700($1.8bln), Cny6.9700($1.1bln)

This week's highlights:

- EUR/USD: Feb03 $1.1850(E3.4bln), $1.1935-40(E2.4bln); Feb04 $1.1850(E1.2bln); Feb05 $1.1800(E2.1bln), $1.1825-35(E1.5bln)

- USD/JPY: Feb04 Y151.50($1.1bln); Feb05 Y153.00($1.1bln), Y154.00($1.0bln)

- AUD/USD: Feb04 $0.6950(A$1.8bln)

EQUITIES: Short-Term Weakness for Eurostoxx 50 Futures Considered Corrective

- A bull cycle in Eurostoxx 50 futures remains intact and S/T weakness is - for now - considered corrective. The next important support to monitor lies at the 50-day EMA at 5851.01. A clear breach of this average would signal scope for a deeper retracement. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. A resumption of gains would open the key resistance and bull trigger at 6072.00, the Jan 14 / 15 high.

- The trend in S&P E-Minis is bullish and the pullback from last week’s high is considered corrective. However, note that a doji candle pattern on Jan 28 and a hammer candle on Jan 29, continues to signal scope for a deeper retracement near-term. Today’s move down reinforces the importance of these two patterns. A continuation lower would expose key S/T support at 6814.50, the Jan 21 low. The bull trigger is at 7043.00, the Jan 28 high.

COMMODITIES: Gold Continues to Unwind Extreme Overbought Condition

- A bull cycle in WTI futures remains intact. However, today’s strong bearish start to this week’s session highlights the beginning of a corrective phase. Attention is on support at the 20-day EMA, at $60.89. The 50-day EMA lies at $59.64. A clear breach of the 50-day average would highlight a stronger reversal and open $58.53, the Jan 20 low. Key resistance and the bull trigger has been defined at $66.48, the Jan 30 high.

- A sharp sell-off in Gold confirms a top in the long-term trend - for now - and from a short-term perspective, marks an unwinding of the recent extreme overbought condition. The metal has traded through the 20-day EMA, and has pierced the 50-day EMA, at $4546.7. A break of this average would signal scope for a deeper retracement and open $4274.7, the Dec 31 ‘25 low. Initial firm resistance is at 4885.1, today’s intraday high so far.

| Date | GMT/Local | Impact | Country | Event |

| 02/02/2026 | 1145/1145 | BOE Breeden on Payments | ||

| 02/02/2026 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 02/02/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 02/02/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 02/02/2026 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 03/02/2026 | 0030/1130 | * | Building Approvals | |

| 03/02/2026 | 0330/1430 | *** | RBA Rate Decision | |

| 03/02/2026 | 0700/0200 | * | Turkey CPI | |

| 03/02/2026 | 0745/0845 | *** | HICP (p) | |

| 03/02/2026 | 0745/0845 | Budget Balance | ||

| 03/02/2026 | 0900/1000 | ** | ECB Bank Lending Survey | |

| 03/02/2026 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 03/02/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 03/02/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 03/02/2026 | 1500/1000 | *** | JOLTS jobs opening level | |

| 04/02/2026 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 04/02/2026 | 2200/0900 | ** | S&P Global Final Australia Composite PMI |