MNI US MARKETS ANALYSIS - Mixed Market Response to Venezuela

Highlights:

- Treasuries see support on Venezuela incursion

- European equities hit fresh highs on APAC outperformance, tech strength

- December ISM manufacturing starts busy data week, culminating in December payrolls on Friday

US TSYS: Supported By US-Venezuela Developments, ISM Mfg In Focus

Treasuries have been increasingly supported overnight following the US capturing Venezuela’s Maduro on Saturday, with FI markets gaining but US equity futures also supported by strong gains for oil names rather than a more typical risk-off play. Today’s calendar is highlighted by ISM manufacturing.

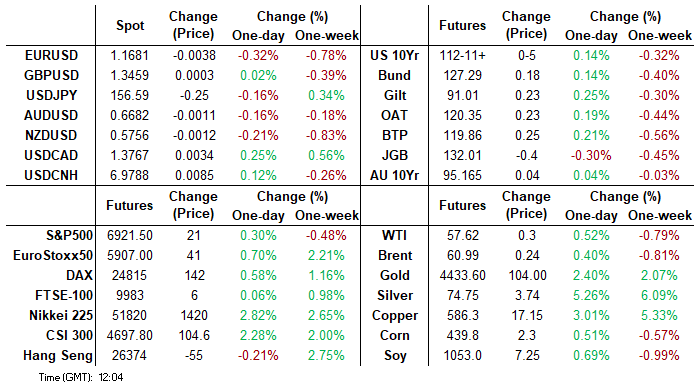

- Cash yields are 1.5-2.5bp lower, with the belly leading declines.

- 2s10s consolidate at 71.4bp (-0.5bp) after 72.3bp on late Friday marked a fresh high since early 2022.

- TYH6 trades at 112-11+ (+05) on modest cumulative volumes of 300k.

- A bear threat remains present with support at 112-01+ (Dec 23 low) before the bear trigger at 111-29 (Dec 10 low) whilst resistance is seen at 112-20 (50-day EMA) before 112-25+ (Dec 30/31 high).

- Data: ISM mfg Dec (1000ET), Wards vehicle sales

- Bill issuance: US Tsy $86B 13W, $77B 26W bill auctions (1130ET)

- Politics: Trump participates in policy meeting w/ closed press (1530ET)

STIR: US Rates Fade Recovery In Oil Futures, Two Horse Fed Chair Race

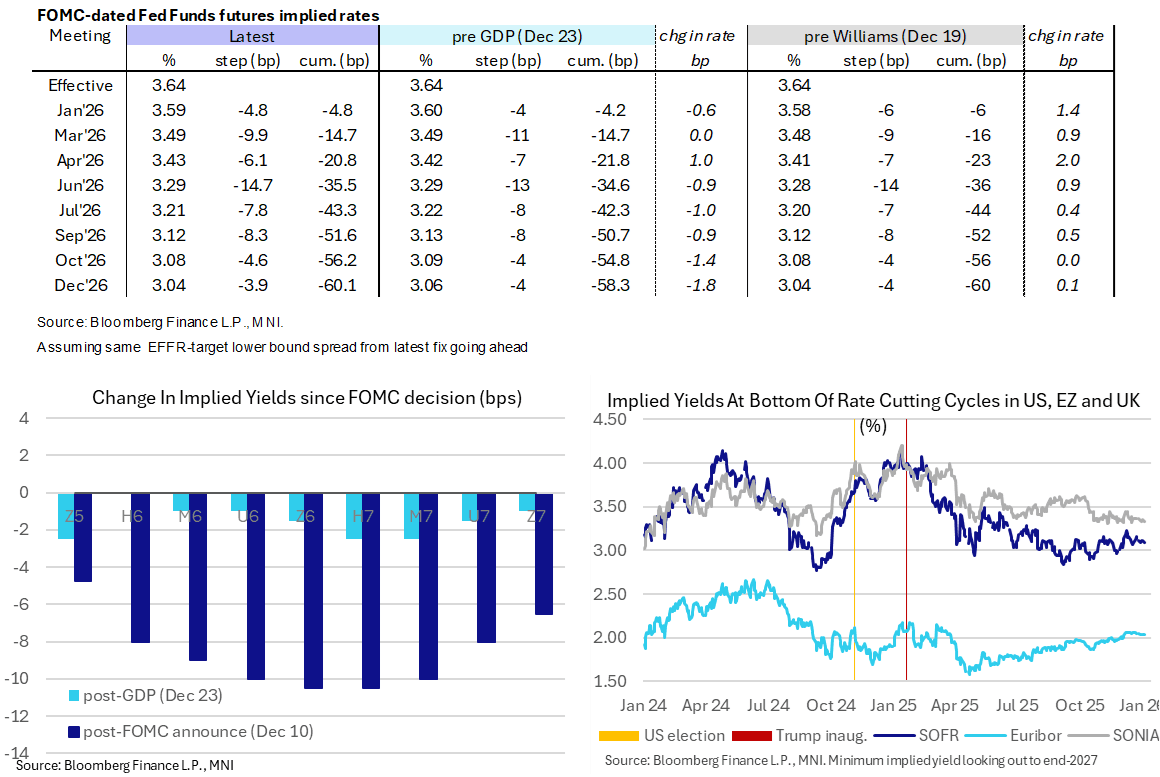

- Fed Funds implied rates hold overnight declines despite crude futures having reversed a large drop in continued fallout from the US capturing Venezuela’s Maduro.

- It leaves a rate path 1bp lower for Mar and ~1.5bp for other quarterly FOMC meetings vs Friday levels, but still only fully prices a next cut in June under a new Fed Chair (announcement could be soon - Hassett 40% and Warsh 37% seen in a two-way battle on Polymarket).

- Cumulative cuts from 3.64% effective: 5bp Jan, 14.5bp Mar, 21bp Apr, 35.5bp Jun, 51.5bp Sep and 60bp Dec.

- SOFR futures are up to 3.5 ticks firmer looking out to end-2027, with a terminal implied yield of 3.095% (Z6, -2bp) within ranges of recent months.

- Philly Fed’s Paulson (’26 voter) on Saturday said modest additional rate cuts could be appropriate later this year if the economy has a benign outlook. The labor market is “clearly bending, it is not breaking”.

- It’s unsurprisingly been a slow start to Fedspeak in the new year. Next up, Barkin (’27 voter) on the economic outlook at 0800ET tomorrow.

- Today’s data docket is instead firmly focused on ISM manufacturing at 1000ET.

MNI POLITICAL RISK ANALYSIS: Political Event Calendar 2026

In our Political Risk calendar for 2026, we include details on the major political events scheduled to take place in developed and emerging markets over the course of the next 12 months. We only include those events that have a set date or period in which they will take place. The known dates outlined in the table below, combined with unconfirmed but expected events and the ever-present prospect of ‘black swan’ shocks, will ensure that political risks continue to have a significant impact on financial, commodity and credit markets through 2026.

MNI SOVEREIGN RATING REVIEW CALENDAR 2026

Please use the above link to access the indicative 2026 sovereign rating review schedules across the five most prominent rating agencies (Fitch, Moody's, S&P, Morningstar DBRS & Scope Ratings). Note that the schedules are indicative only and ratings can be reviewed on an ad-hoc basis. Rating agencies may also adjust their schedules during the year.

US TSY FUTURES: Short Setting Across The Curve On Friday

OI data points to net short setting across the curve on Friday, with the most pronounced moves coming in TU, TY, UXY & US futures.

- The curve saw over $10mln DV01 of fresh net short exposure added.

| 02-Jan-26 | 31-Dec-26 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,589,831 | 4,530,950 | +58,881 | +2,280,913 |

FV | 6,697,936 | 6,696,715 | +1,221 | +53,482 |

TY | 5,498,255 | 5,461,347 | +36,908 | +2,463,029 |

UXY | 2,573,262 | 2,543,105 | +30,157 | +2,716,584 |

US | 1,871,803 | 1,853,697 | +18,106 | +2,504,451 |

WN | 2,095,929 | 2,093,461 | +2,468 | +451,566 |

|

| Total | +147,741 | +10,470,025 |

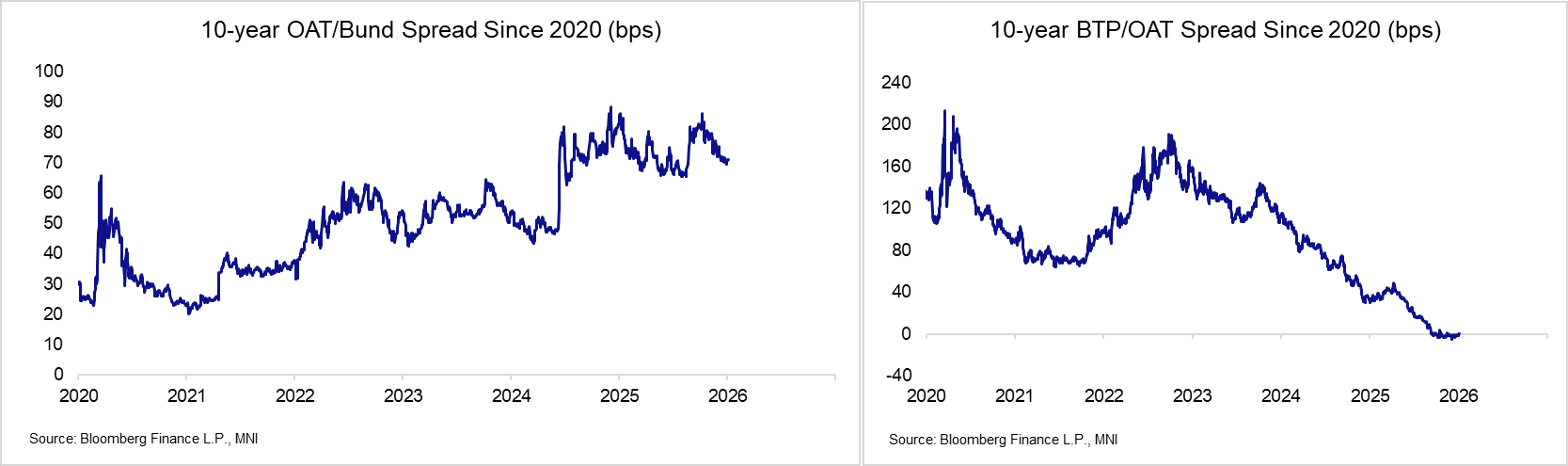

EGBS: French Political Risks Still A Focus For OAT Investors

- French political risks remain a focus in January, with the Government set to restart 2026 budget negotiations on Thursday. PM Lecornu will have to walk a fine line between ensuring enough fiscal restraint to get the conservative Les Republicains on board, while ensuring that the budget is not so austere that the centre-left Socialists cannot abstain (the only path for a majority in the National Assembly).

- Accordingly, the 10-year OAT/Bund spread has continued to struggle pushing below the 70bp handle in recent weeks.

- A reminder that before Christmas, the Government passed a “special law” to ensure that taxes can continue to be levied, gov't debt can be issued, and public sector workers can be paid in the absence of a state budget for 2026. This is a stop-gap solution, with the budget rollover doing little to improve France’s concerning fiscal position.

- Elsewhere, the BTP/OAT spread has struggled to deviate meaningfully from the 0bp level since October. Although relative fiscal and political backdrops may argue for lower yields in Italy compared to France, there still seems to be some hesitance amongst participants to endorse this fully. That may reflect acknowledgement that Italy is still the largest bond issuer in the Eurozone, alongside historical biases of Italy as a source of volatility and instability in the region (e.g. during the sovereign debt crisis).

HUNGARY: Orban Says He Doesn't Plan Switch to Presidential System

"ORBAN SAYS HE DOESN'T PLAN SWITCH TO PRESIDENTIAL SYSTEM" - BBG

- Slight bounce for HUF on that headline, with EURHUF now almost back to flat on the session. Bloomberg had reported in December that "Orban is toying with the idea of assuming the presidency and rewriting laws to make it into the most powerful office in the country."

- We noted then that the possibility of pushing through the reform to a more dominant presidential system could be politically damaging – as the Bloomberg piece noted: “That path would be risky, though, if it was seen as going against the popular will.” Furthermore, Orban would have had to used Fidesz’s current supermajority in parliament before April's election to push through the change. Nonetheless, the report weighed heavily on the forint at the time of release, despite the low likelihood of Orban pushing through the reform.

CHINA: MoFA: Chinese Interests In Venezuela Protected By Law

(MNI) London - China's Xinhua reports comments from Ministry of Foreign Affairs spox Lin Jian in a press conference earlier today, stressing that Beijing views existing contracts between the Chinese and Venezuelan gov'ts as still operational and subject to international law: "No matter how the political situation in Venezuela changes, China's willingness to deepen pragmatic cooperation in various fields will not change, and China's legitimate interests in Venezuela will be protected in accordance with the law." The comments come in the context of the US military operation that removed Venezuelan President Nicolas Maduro from power and detained him on drug trafficking charges.

- The spox added that China views the US action as a violation of "international law and the basic norms governing international relations, as well as the purposes and principles of the UN Charter."

- Lin said that "no matter how the international situation changes, China will always be a good friend and partner of Latin American and Caribbean countries, and China's policy toward Latin America will maintain continuity and stability."

- Lin: "China is willing to work with Latin American countries to continue to unite and cooperate in responding to the changing international situation, and to seek common development and prosperity through mutually beneficial cooperation".

FOREX: USD Tilts Higher Amid Venezuela Uncertainty, Oil Tied FX Pressured

- The fallout from Venezuela remains difficult to parse for G10 FX, which are instead following cross-market cues via higher precious metals and rallying equities (IT and industrials outperform thanks to tech strength in Asia as well as ASML's 3.5% rally on a Bernstein upgrade).

- The USD's continued recovery off the late December lows nicely coincides with the formation of a golden cross (50-dma > 200-dma), pointing to potential corrective activity in the USD Index's 1% rally since Christmas.

- We noted the distinct pressure on front-end implied vols across G10 FX in the lead-up to Christmas (even when seasonals were accounted for), and little has changed. EUR 3m vols remain trending lower, with JPY the sole standout in vol space.

- Oil-sensitive FX is underperforming as crude softens despite the significant uncertainty over Venezuela’s oil production capability after the capture of Maduro.

- As such, USDCAD upward pressure comes via both legs of the trade, making light work of its 20-day EMA, narrowing the gap to the 1.3806 December 19 high. From a technical perspective, a bear theme remains intact for now, with key short term support at 1.3643 but short-term the corrective bounce may extend.

- USDNOK expectedly also sees gains this morning but remains within its December range, with resistance at 10.2429, the December 18 high.

- Key focus is on any cues if the US will be able to secure power over Venezuela and if further intervention may be needed to achieve that given some question marks on now acting president Delcy Rodriguez.

- Elsewhere, ISM Manufacturing highlights the data calendar for today while markets await Friday's December employment report. This will be the last NFP release before the FOMC's end-January meeting, at which participants would probably require substantially weaker-than-expected figures to spur even consideration of a another 25bp cut.

JPY: USDJPY Whipsaws amid Venezuela Developments, Key Resistance Remains Intact

- Safe haven demand following the uptick in geopolitical uncertainty re Venezuela has mainly been viewed through a precious metals lens, with a significant bump higher for the likes of gold and silver being offset by stronger risk appetite in markets/equities generally.

- A firmer dollar prompted a break of 157.00 for USDJPY overnight, a level that had held in the post-holiday period. Momentum demand took spot to session highs of 157.30, however, the lack of clarity surrounding the outlook for Venezuela & global market repercussions quickly saw momentum stall. Furthermore, the yen’s historical safe haven status may have assisted the reversal back to session lows of 156.66.

- Moving average studies highlight a dominant uptrend, with attention remaining on key resistance at 157.89, the Nov 20 high and the bull trigger. Initial support to watch lies at 155.00, the 50-day EMA.

- As a reminder, Finance Minister Katayama recently intensified her warnings against rapid JPY weakening, stating the MOF has a “free hand” to take bold action. This will likely remain the company line for now, barring a sustained move above 158.00.

- At his Dec 25 speech, BOJ Governor Ueda said that the achievement of the 2% stable inflation target accompanied by wage increases is “steadily approaching”, and that the board will continue to raise rates in line with the improvement of the economy and inflation. There remains a lack of detail regarding the hiking timeline, and Ueda’s latest remarks have done little to move the needle as the market broadly expects another two hikes across 2026.

EQUITIES: Fresh Cycle Highs for Eurostoxx Futures Reinforce Bullish Theme

A bull cycle in Eurostoxx 50 futures remains intact and a fresh cycle high today, reinforces the bull theme and confirms a resumption of the primary uptrend. Note that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 5935.01 next, a Fibonacci projection. On the downside, initial firm support is seen at 5762.47, the 20-day EMA. Short-term weakness in S&P E-Minis appears corrective. A key short-term support has been defined at 6771.50, the Dec 18 low. Clearance of this level is required to signal scope for a deeper retracement and would also highlight a possible short-term reversal. For bulls, sights are on key resistance at 7014.00, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the primary uptrend.

- Japan's NIKKEI closed higher by 1493.32 pts or +2.97% at 51832.8 and the TOPIX ended 68.55 pts higher or +2.01% at 3477.52.

- Elsewhere, in China the SHANGHAI closed higher by 54.577 pts or +1.38% at 4023.417 and the HANG SENG ended 8.77 pts higher or +0.03% at 26347.24.

- Across Europe, Germany's DAX trades higher by 213.64 pts or +0.87% at 24748.4, FTSE 100 higher by 29.32 pts or +0.29% at 9976.06, CAC 40 up 26.18 pts or +0.32% at 8220.53 and Euro Stoxx 50 up 48.89 pts or +0.84% at 5899.12.

- Dow Jones mini up 24 pts or +0.05% at 48643, S&P 500 mini up 14.25 pts or +0.21% at 6915.75, NASDAQ mini up 128 pts or +0.5% at 25519.

COMMODITIES: Gold Continues to Reverse Late-December Sell-Off

The trend condition in WTI futures remains bearish and recent gains are considered corrective. Moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the downtrend would signal scope for a move towards $53.77, a Fibonacci projection. Key short-term resistance is $61.25, the Oct 24 high. First resistance is at $58.47, the 50- day EMA. The trend structure in Gold is unchanged, it remains bullish and a sharp sell-off late December appears corrective - for now. The trend is overbought and a deeper retracement would allow this condition to unwind. First support at $4325.1, the 20-day EMA, has been pierced. A clear break of the average would expose the 50-day EMA at $4194.5. For bulls, a resumption of gains would open $4578.3, a Fibonacci projection.

- WTI Crude down $0.06 or -0.1% at $57.22

- Natural Gas down $0.12 or -3.32% at $3.495

- Gold spot up $102.57 or +2.37% at $4435.24

- Copper up $17.5 or +3.07% at $587.2

- Silver up $3.47 or +4.76% at $76.278

- Platinum up $83.79 or +3.91% at $2230.24

| Date | GMT/Local | Impact | Country | Event |

| 05/01/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/01/2026 | 1500/1000 | *** | ISM Manufacturing Index | |

| 05/01/2026 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/01/2026 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 06/01/2026 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 06/01/2026 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 06/01/2026 | 0001/0001 | * | BRC Monthly Shop Price Index | |

| 06/01/2026 | 0745/0845 | *** | HICP (p) | |

| 06/01/2026 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0815/0915 | ECB Cipollone Chairs Intl Monetary System Panel | ||

| 06/01/2026 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 06/01/2026 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 06/01/2026 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 06/01/2026 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 06/01/2026 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 06/01/2026 | 1300/1400 | *** | Germany CPI (p) | |

| 06/01/2026 | 1300/1400 | *** | Germany CPI (p) | |

| 06/01/2026 | 1300/0800 | Richmond Fed's Tom Barkin | ||

| 06/01/2026 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 06/01/2026 | 1445/0945 | *** | S&P Global Services Index (final) | |

| 06/01/2026 | 1445/0945 | *** | S&P Global US Final Composite PMI |