MNI US MARKETS ANALYSIS - ISM Manufacturing in Focus

Highlights:

- ISM Manufacturing in focus as government shutdown extends into a new week

- GBP consolidates weakness as Budget pessimism beds in ahead of BoE

- Treasury financing requirements and ample Fedspeak due, with Miran, Daly and Cook on the schedule

US TSYS: Key TY Support Still Exposed Despite Friday Rally

- Treasuries have pared losses that were seen with the late cash open (Japan holiday), trading back close to Friday’s close that appeared to be spurred by Fed Gov Waller but with a possible exaggeration by month-end factors.

- Crude oil futures rolling over have helped support intraday moves.

- Today’s docket is centered on the ISM manufacturing survey for October before the week’s data turns more firmly to the labor market. We also hear what should be broadly dovish Fedspeak after Friday’s hawkish start to post-FOMC appearances barring a more dovish Waller late on.

- With President Trump back from his Asia trip, focus increasingly turns to the ongoing government shutdown which is set to become the longest in US history.

- Cash yields are 0.5-1bp lower on the day.

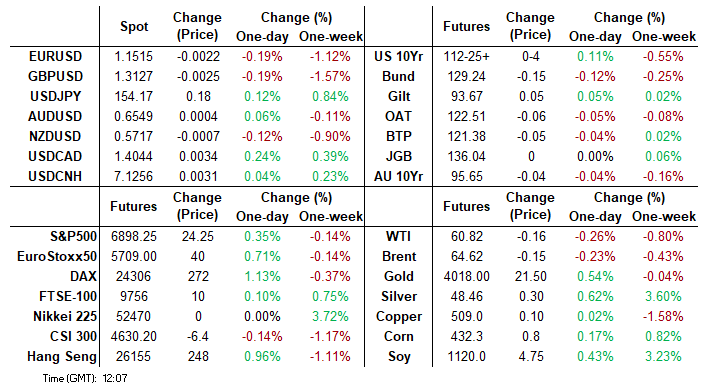

- TYZ5 trades at 112-25+ (+04) as it holds close to a high of 112-27+ seen late Friday, with thin volumes only just inching above 200k in part owing to the Japan holiday.

- Resistance is seen at 113-06 (20-day EMA) but a key support remains exposed at 112-06 (Sep 25 low). Before that though, 112-16 (Oct 30 low) and 112-14 (Oct 9 low).

- Treasury financing requirements released today at 1500ET. That's part of the U.S. Treasury’s first Refunding process of the 2026 fiscal year ahead of the full announcement on Wednesday at 0830ET. The QRA is likely to largely keep a steady approach to issuance policy, including leaving nominal Treasury coupon auction sizes unchanged for the 7th consecutive quarter. We also do not expect Treasury’s guidance on coupon issuance to change in this Refunding round.

- Data: S&P Global mfg PMI Oct F (0945ET), ISM mfg Oct (1000ET), Wards vehicle sales

- Fedspeak: Miran (~0715ET), Daly (1200ET), Cook (1400ET) – see FED bullet.

- Bill issuance: US Tsy $86B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump participates in Virginia Tele-Rally (1900ET), Trump participates in New Jersey Tele-Rally (1930ET)

STIR: US Rates Hold Late Friday Waller-Inspired Rally

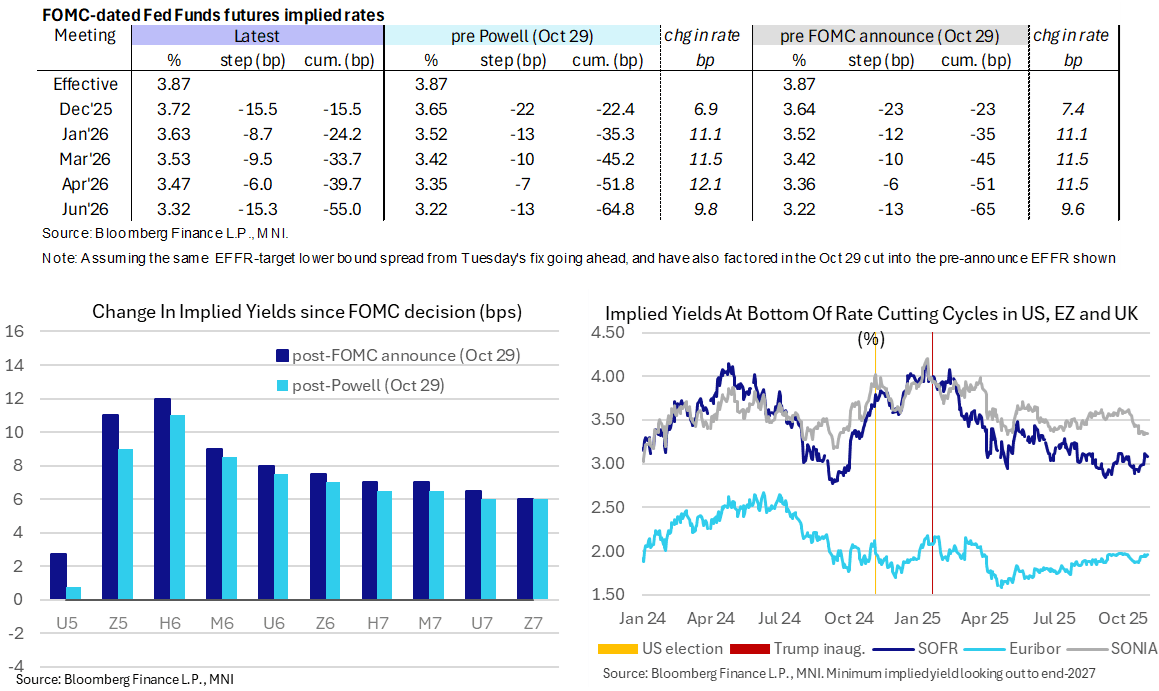

- Fed Funds implied rates are unchanged from Friday’s close, consolidating the dip seen late on seemingly following Fed Governor Waller eyeing another cut in December.

- Waller had sounded a little more cautious ahead of the October FOMC but he’s also clearly one of the most dovish FOMC members so it shouldn’t be a particular surprise.

- Month-end factors could also have been at play but the holding of the move suggests it was secondary, and broader context is needed after what was a sizeable hawkish repricing on Powell mid-week highlighting a particularly divided FOMC.

- Cumulative cuts from 3.87% effective: 15.5bp Dec, 24bp Jan, 33.5bp Mar, 39.5bp Apr and 55bp Jun.

- SOFR futures are currently led by a 3 tick increase in the M6, whilst the terminal yield has cooled a little further to 3.085% (H7, -2bp) after Thursday’s 3.11% marked the highest close since August.

FED: More Dovish Fedspeak Eyed After Friday’s Broad Rate Cut Pushback

Today’s Fedspeak sees more dovish/at most centrist FOMC members scheduled compared to Friday’s mostly more hawkish stance (before a typically dovish Waller late on). We’re set to hear from Miran, Daly and Cook, with our pick being Cook for her first monetary policy relevant remarks in nearly three months.

- ~0715ET – Gov. Miran (voter) on Bloomberg TV. He didn't publish a dissent statement on Friday, having also shied away from tradition after the September meeting, but his dovish stance is well-known. He has been advocating for 50bp cuts and noted after the mid-October deterioration in US-China trade relations that there was more urgency to get rates to neutral. It will be interesting to see whether this latest urgency is dialled back at the margin. Limited headlines from a NYT interview published Saturday morning noted that restrictive policy poses a risk to the labor market and is making the economy more brittle to shocks.

- 1200ET – SF Fed’s Daly (non-voter) in moderated conversation (no text). Recently towards the more dovish end of the FOMC spectrum, she said on Sep 24 that she "fully supported" the Fed's 25bp September cut, and suggested "Moving forward, it is likely that further policy adjustments will be needed as we work to restore price stability while providing needed support to the labor market." She notes that the latest Fed Dot Plot showed that further cuts were expected, "but these are projections, not promises, and making good decisions will require us to anchor on our objectives, assess the tradeoffs, and decide, again and again."

- 1400ET – Gov. Cook (voter) on economy and monetary policy (text + Q&A). We haven’t heard from Cook on monetary policy since the second half of August when President Trump tried to force her resignation and then fire her in what’s been a lengthy legal process. She noted back in early August that the jobs report at the time was concerning as big jobs revisions were somewhat typical of turning points and that the unemployment rate is still a good indicator of slack. We consider her to towards the center of the hawk/dove spectrum, albeit slightly on the dovish side.

- For a review of Friday’s post-FOMC Fedspeak, see the MNI US Macro Weekly here which captured remarks from Bostic, Hammack, Logan and Schmid. It was published before Waller said all the data suggest the Fed should cut rates again in December. He would say yes if President Trump asked him to be Fed Chair.

SOFR: Mix Of Positioning Swings Seen In Futures On Friday

OI data points to net short setting dominating in the SOFR whites on Friday, while net long setting was most prominent in the reds.

- Net positioning swings in the greens and blues were more modest.

| 31-Oct-25 | 30-Oct-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,406,744 | 1,394,619 | +12,125 | Whites | +43,024 |

SFRZ5 | 1,489,945 | 1,523,076 | -33,131 | Reds | +26,024 |

SFRH6 | 1,182,715 | 1,136,869 | +45,846 | Greens | -4,739 |

SFRM6 | 1,089,531 | 1,071,347 | +18,184 | Blues | +1,523 |

SFRU6 | 1,071,525 | 1,068,276 | +3,249 |

|

|

SFRZ6 | 1,149,998 | 1,151,313 | -1,315 |

|

|

SFRH7 | 823,220 | 798,156 | +25,064 |

|

|

SFRM7 | 757,777 | 758,751 | -974 |

|

|

SFRU7 | 736,537 | 736,225 | +312 |

|

|

SFRZ7 | 800,131 | 802,134 | -2,003 |

|

|

SFRH8 | 403,453 | 404,331 | -878 |

|

|

SFRM8 | 398,851 | 401,021 | -2,170 |

|

|

SFRU8 | 322,321 | 321,653 | +668 |

|

|

SFRZ8 | 316,348 | 314,315 | +2,033 |

|

|

SFRH9 | 210,487 | 210,994 | -507 |

|

|

SFRM9 | 182,161 | 182,832 | -671 |

|

|

US TSY FUTURES: Curve-Wide Positioning Little Changed On Friday

OI data points to a mix of net long cover (TY, UXY & WN) and short setting (US) further out the curve as long end futures settled lower on Friday.

- TU & FV futures were unchanged at settlement, so it is difficult to make any meaningful assertions when it comes to positioning swings in those contracts (outside of exposure being added in TU and trimmed in FV).

- Net curve-wide DV01 equivalent exposure was little changed on the day.

| 31-Oct-25 | 30-Oct-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,603,126 | 4,565,661 | +37,465 | +1,420,372 |

FV | 6,804,374 | 6,815,692 | -11,318 | -487,624 |

TY | 5,489,795 | 5,509,193 | -19,398 | -1,300,555 |

UXY | 2,486,249 | 2,489,353 | -3,104 | -279,552 |

US | 1,904,209 | 1,895,255 | +8,954 | +1,145,107 |

WN | 2,124,810 | 2,128,266 | -3,456 | -650,824 |

|

| Total | +9,143 | -153,076 |

EUROPEAN INFLATION: MNI Inflation Insight: Services Beat, Travel At Play?

- We have published and e-mailed to subscribers the MNI Eurozone Inflation Insight.

- Please find the full report here: https://media.marketnews.com/Oct2025_EZCPI_Review_a8c2d28cbb.pdf

- Eurozone HICP inflation was as expected in the flash October release but core HICP surprised a little stronger with a Y/Y rate showing no moderation from September.

- Services inflation ticked higher although country-level data hint at volatile travel-related categories at play.

- The full October release on Nov 19 will provide a more useful update on exact drivers.

- By major country, Germany, Spain and Netherlands were all stronger than expected, France was in line and Italy saw a sizeable downside miss.

- The ECB is still seen being unlikely to cut at the next meeting in December (1-2bp priced) but with some sources warning that it could see more a lively discussion than some are expecting.

FOREX: ISM Data in Focus as Shutdown Drags into Another Week

- The US ISM manufacturing print takes focus Monday, with the dearth of official US government data meaning private sector data takes precedent. The US government shutdown enters a new week, with Democrats appealing to Trump directly to intervene and pressure lawmakers into a sustainable compromise - but there remains little expectation of a near-term resolution. As a result, markets expect the shutdown to persist for at least a few more weeks.

- AUD trades a little firmer Monday, keeping a technical bull cycle in play for AUDUSD as Tuesday's RBA decision looms. The Q3 trimmed mean CPI print at 3.0% y/y was at the top of the 2-3% target band, a "material miss" for the RBA, which reinforces the likelihood of rates being held at 3.6% tomorrow. Indeed, RBA-dated OIS pricing implies almost no chance of a cut, with just a 2% probability assigned.

- UK fiscal developments as we approach the Nov 26 budget have been key in shaping the short-term trajectory for sterling, however, there might be greater focus this week on the Bank of England decision, which is far from certain. Indeed, we would categorise our own view of the outcome as 50/50 between a 25bp cut and a hold. If it wasn't for the upcoming budget we would have more certainty that a cut would be delivered given the downside surprises to inflation (particularly as this was driven by food) and the downside surprise to wage growth. Despite Friday’s GBPUSD close, last week’s breach of key 1.3142 support is a meaningful development for the pair, strengthening current bearish conditions. Last week’s low at 1.3097 represents the immediate level of note, however, more meaningful support is at 1.3041, the Apr 14 low. Below here, support appears scant until 1.2709, the April 07 low.

- Meanwhile, ongoing strength for the major equity benchmarks, alongside the domestic narrative in Japan, continue to underpin the AUDJPY rally. The cross traded to fresh 11-month highs last Thursday above the 101 mark, of which a sustained break would place the focus on the US election related highs at 102.41.

CHF: USDCHF Strength Will Hinge on US Private Data This Week

- Broad USD strength combined with firmer global equities has helped USDCHF clear the October high, prompting the pair to change hands at its highest level since August 22nd. This clears resistance up to 0.8104. Sustainability of the move higher here will depend on the suite of private US data releases set for this week, specifically: today's US ISM Manufacturing and S&P Global Manufacturing PMI, ISM Services and ADP Employment data on Wednesday ahead of prelim UMich sentiment data on Friday.

- Following the surprising division of the FOMC at last week's rate decision, a presumed December rate cut has been called into question - and absent official US government releases, these private sector numbers will take on greater importance, and should certainly play a part in policy-setting for the hawks into the final decision of the year (indeed, Powell has referenced the Michigan inflation expectations survey in press conferences previously).

- As a result, a strong turnout from the private sector numbers this week would pose upside risks to USDCHF, and clearance of 0.8104 would extend the upside of the range toward 0.8171, the late July rally top.

FOREX: GBP Selloff Consolidating, BOE Decision Due Thursday

- UK fiscal developments have been key in shaping the short-term trajectory for sterling, however, there might be greater focus this week on the BOE decision, of which the outcome is far from certain. Indeed, we would categorise our own view as 50/50 between a 25bp cut and a hold given the downside surprises to inflation and wage growth.

- Despite Friday’s GBPUSD close above, last week’s breach of key 1.3142 support is a meaningful development for the pair, strengthening current bearish conditions. Last week’s low at 1.3097 represents the immediate level of note, while more meaningful support is at 1.3041, the Apr 14 low. Below here, support appears scant until 1.2709, the April 07 low.

- EURGBP has weakened a touch to start the week, with the cross returning to the prior breakout point of 0.8769. Note that the overall trend is overbought, and this pullback is considered corrective at this juncture, with initial support coming in at 0.8751, the Sep 25 high. Topside targets for the broader rally include 0.8835 and 0.8875, the April 2023 high.

- Another cross that will remain in focus is GBPAUD, especially given the RBA decision on Tuesday. A break of the recent cycle lows at 2.0244 significantly boosted downside momentum, with the cross printing below 2.00 last week, the lowest level in 8 months. Consolidating weakness may signal scope for an extension lower towards the year’s lows around 1.96.

- Elsewhere this week, DMP data is scheduled after the BOE, which could hint at whether December is in play, while markets will also pay attention to final services PMI figures.

OPTIONS: Expiries for Nov3 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1400(E686mln), $1.1450(E772mln), $1.1600(E561mln), $1.1695(E614mln)

- USD/JPY: Y150.00($1.1bln)

- USD/CAD: C$1.3980-85($1.1bln)

EQUITIES: Trend Structure in Eurostoxx Bullish After Last Week's Cycle Highs

- The trend structure in Eurostoxx 50 futures remains bullish. Last week’s fresh cycle highs reinforces a bull theme and the move higher maintains the rising price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant medium-term uptrend. Sights are on 5777.41, a Fibonacci projection. First support lies at 5648.93, the 20-day EMA.

- The trend condition in S&P E-Minis is unchanged, it remains bullish and the latest pullback appears corrective. The fresh cycle high last week confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 6974.04 next, a Fibonacci projection point. Initial firm support to watch lies at 6795.74, the 20-day EMA. Key pivot support lies at 6690.58, the 50-day EMA.

COMMODITIES: Nearby WTI Future Resistance Levels Remain Exposed

- Recent gains in WTI futures appear corrective for now, however, note that price has recently traded through the 50-day EMA, currently at $61.05. The breach of this EMA signals scope for a stronger recovery. A resistance at $62.34, the Oct 8 high, has also been pierced. A clear move through it would expose key resistance at $65.77, the Sep 26 high. First key support and the bear trigger is unchanged at $55.96, the Oct 20 low.

- A fresh cycle low last week in Gold highlights an extension of the bear cycle that started Oct 20. The retracement since Oct 20 has allowed an overbought trend condition to unwind. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3859.1. Clearance of this EMA would strengthen a short-term bear theme. Initial resistance is at $4161.4, the Oct 22 high.

| Date | GMT/Local | Impact | Country | Event |

| 03/11/2025 | 1200/1300 | ECB Lane Lecture In Dublin | ||

| 03/11/2025 | - | *** | Domestic-Made Vehicle Sales | |

| 03/11/2025 | 1445/0945 | *** | S&P Global Manufacturing Index (final) | |

| 03/11/2025 | 1500/1000 | *** | ISM Manufacturing Index | |

| 03/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 03/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 03/11/2025 | 1700/1200 | San Francisco Fed's Mary Daly | ||

| 03/11/2025 | 1830/1330 | BOC Governor fireside chat at The Logic conference | ||

| 03/11/2025 | 1900/1400 | Federal Reserve Governor Lisa Cook | ||

| 04/11/2025 | 0030/0930 | ** | S&P Global Final Japan Manufacturing PMI | |

| 04/11/2025 | 0330/1430 | *** | RBA Rate Decision | |

| 04/11/2025 | 0740/0840 | ECB Lagarde Keynote Speech At Bulgarian National Bank | ||

| 04/11/2025 | 0745/0845 | Budget Balance | ||

| 04/11/2025 | 0945/1045 | ECB Lagarde At Bulgarian National Bank Press Conference | ||

| 04/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 04/11/2025 | 1135/0635 | Fed Vice Chair Michelle Bowman | ||

| 04/11/2025 | 1140/1140 | BOE Breeden at International Banking Conference | ||

| 04/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 04/11/2025 | 2100/1600 | Canada federal budget, release expected just after 4pm EST | ||

| 05/11/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 05/11/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI |