MNI US MARKETS ANALYSIS - Fed Minutes Watched for July Clues

Highlights:

- Fed minutes watched for any tangible discussion of July rate cut

- EUR/JPY bull streak extends, hits new cycle high in APAC hours

- EU-US trade deal could be nearing, ambassadors prepped for announcement as early as today

US TSYS: Sights on June FOMC Minutes, Projected Rate Cuts Near 50Bp by Year End

- Treasuries are trading firmer, inside narrow overnight ranges - setting sites on this afternoon's FOMC minutes for the June meeting - on an otherwise light data schedule: MBA Mortgage Applications at 0700ET, Wholesale Trade Sales/Inventories at 1000ET. No scheduled Fed speakers today.

- The minutes should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end.

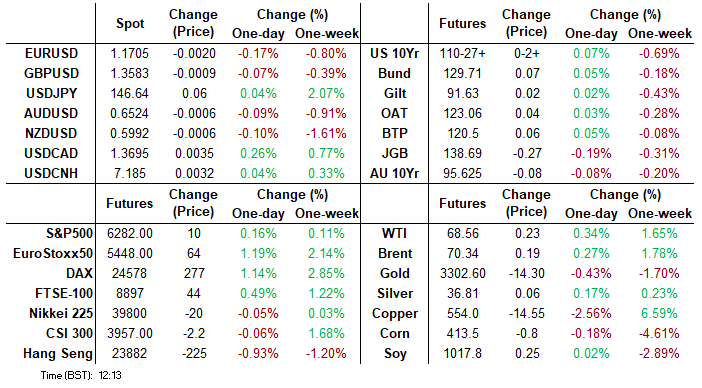

- Tsy Sep'25 10Y futures are currently +2 at 110-27, inside a narrow 5.5 tick range on modest volume (TYU5 under 285k). Futures maintain a softer short-term tone following the retracement that started Jul 1. Sights are on 110-17 next, a Fibonacci retracement point. A break would strengthen a bearish threat. Resistance to watch is at 111-28, the Jul 3 high.

- Projected rate cut pricing largely steady vs late Tuesday (*) levels: Jul'25 steady at -1.2bp, Sep'25 steady at -17.3bp, Oct'25 steady at -31.7bp, Dec'25 at -49.3bp (-48.6bp).

- Cross asset roundup: Bbg US$ index mildly higher (BBDXY +.84 at 1197.47), Gold softer (-7.15 at 3294.77), crude mildly higher (WTI +0.25 at 68.58), stocks mildly higher (SPX eminis +8.25 at 6280.25).

MNI FOMC MINUTES PREVIEW - JUNE 2025: Lack of Support for a July Cut

The minutes of the June 17-18 FOMC meeting (released at 2pm ET) should underline the Committee's patience in making its next rate move amid heightened tariff-related economic uncertainty, as encapsulated in the meeting's Dot Plot which showed participants largely divided between no cuts and 2 cuts by year-end. We have heard significant dovishness on the rate front from Board members Bowman and Waller since June's meeting, and while they appear to be outliers, it could be interesting to see whether any other members tend to agree with the view that the incoming tariff inflation will be largely transitory.

SOFR: Mix Of Short Setting & Long Cover Seen In Futures On Tuesday

OI data suggests that net short setting dominated in 3/4 white and green SOFR futures on Tuesday, while net long cover was more prominent in 3/4 reds and blues.

| 08-Jul-25 | 07-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,305,751 | 1,307,623 | -1,872 | Whites | +31,642 |

SFRU5 | 1,188,133 | 1,183,517 | +4,616 | Reds | -24,686 |

SFRZ5 | 1,290,015 | 1,275,002 | +15,013 | Greens | +4,879 |

SFRH6 | 990,099 | 976,214 | +13,885 | Blues | -5,316 |

SFRM6 | 856,321 | 845,067 | +11,254 |

|

|

SFRU6 | 819,116 | 837,275 | -18,159 |

|

|

SFRZ6 | 899,903 | 912,413 | -12,510 |

|

|

SFRH7 | 720,269 | 725,540 | -5,271 |

|

|

SFRM7 | 668,280 | 664,476 | +3,804 |

|

|

SFRU7 | 471,348 | 467,194 | +4,154 |

|

|

SFRZ7 | 414,134 | 412,914 | +1,220 |

|

|

SFRH8 | 314,802 | 319,101 | -4,299 |

|

|

SFRM8 | 230,689 | 228,191 | +2,498 |

|

|

SFRU8 | 199,237 | 204,307 | -5,070 |

|

|

SFRZ8 | 185,482 | 187,455 | -1,973 |

|

|

SFRH9 | 141,082 | 141,853 | -771 |

|

|

US TSY FUTURES: Mix Of Short Setting & Long Cover Seen On Tuesday

OI data points to a mix of net short setting and long cover during Tuesday’s downtick in futures, with the most meaningful net positioning swings coming via net short setting in TU futures and net long cover in FV futures.

| 08-Jul-25 | 07-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,354,026 | 4,285,962 | +68,064 | +2,590,500 |

FV | 7,007,587 | 7,034,656 | -27,069 | -1,166,321 |

TY | 4,920,369 | 4,933,087 | -12,718 | -837,542 |

UXY | 2,416,310 | 2,420,925 | -4,615 | -401,207 |

US | 1,830,260 | 1,835,915 | -5,655 | -777,081 |

WN | 1,960,908 | 1,957,874 | +3,034 | +551,120 |

|

| Total | +21,041 | -40,530 |

US-EU: EU on Standby for Potential Trade Announcement Tonight

Guardian correspondent on state of EU-US trade: "EU is on standby for an announcement tonight (or maybe not) with ambassadors meeting again this afternoon Trade commissioner Maros Sefcovic spoke to commerce secretary Howard Lutnick today and will speak to Jamieson Greer this afternoon"

EUROPE ISSUANCE UPDATE:

UK auction results

- Decent 4.50% Mar-35 Gilt Auction: The yield tail of 0.2bp was tighter than all four previous re-openings (range 0.3-0.5bps), while the bid-to-cover ratio was in line with last month’s outing at 2.89x.

- Lowest accepted price of 98.936 above the 98.8985 pre-auction mid price.

- Limited reaction in the secondary price of the Gilt briefly after the results were published.

- Similarly limited reaction in Gilt futures.

- GBP4.5bln of the 4.50% Mar-35 Gilt. Avg yield 4.635% (bid-to-cover 2.89x, tail 0.2bp).

Germany auction results

- E1.5bln (E1.135bln allotted) of the 2.60% May-41 Bund. Avg yield 3% (bid-to-offer 1.15x; bid-to-cover 1.52x).

- E1bln (E794mln allotted) of the 2.50% Jul-44 Bund. Avg yield 3.04% (bid-to-offer 3.52x; bid-to-cover 4.43x).

Portugal auction results

- E650mln of the 0.30% Oct-31 OT. Avg yield 2.57% (bid-to-cover 2.09x).

- E610mln of the 1.00% Apr-52 OT. Avg yield 3.78% (bid-to-cover 1.93x).

SWITZERLAND: Potential 200% US Pharma Tariffs - Impact on Switzerland [1/2]

President Donald Trump on Tuesday threatened to impose up to 200% tariffs on pharma products “very soon”. However, the administration would “give people about a year, year and a half” to incentivize production relocalisation into the US, and Switzerland might get proprietary assurances on the sector in a US/SZ trade deal, limiting the potential impact of measures imposed by the US more generally. Swiss pharma equities saw some volatility this morning but remained within recent ranges - supporting the view of a limited impact.

- Remember that on July 4, Bloomberg wrote: "The draft of a trade accord between the US and Switzerland contains a provision that the European country will receive preferred treatment in the ongoing national-security investigations to avoid tariffs on pharma exports, according to people familiar with the matter" but "the clause doesn't constitute a guarantee that Washington will hold off on putting tariffs on the industry".

- The Swiss government has agreed to that draft accord according to local news. There are "positive signs" but no agreement yet from the US, according to the reports.

- Swiss "pharmaceuticals, vitamins, diagnostics" exports were CHF122.1bln in the 12 months to May 2025 in nominal terms - that is around 43% of total Swiss exports during that time, or around 6.8% of GDP, while Swiss exports to the US (across products) were CHF58.4bln.

SWITZERLAND: Potential 200% US Pharma Tariffs - Impact on Switzerland [2/2]

- JP Morgan note generally that "for branded drugs, production had in the past shifted to Europe for tax reasons, but this is no longer so relevant. Such a high tariff [referring to the 200% figure] would be more of an issue for generic drugs though, where production is overseas for traditional cost of manufacturing reasons" - domestic Swiss production tends to be centred in the branded segment, which would then arguably be more akin to relocation to the US.

- In that context, our credit team does view recent US investment projects by Swiss pharmaceutical firms as significant.

- Leerink Partners meanwhile believe Tuesday's announcement by the US administration is net positive for the pharma industry “because tariffs will not be implemented immediately…and it is unclear if the administration will follow through in the future”, according to a note seen by CNBC.

- Details on the measures “will come at the end of the month,” Commerce Secretary Howard Lutnick said after the cabinet meeting (also via CNBC).

FOREX: USD Index Consolidates Break Above Downtrendline

- Tariffs and trade remain the primary drivers of near-term sentiment, and the President surprised markets again late yesterday in announcing a 50% tariff on copper imports – triggering a near 20% rally in US-listed futures and reminding markets that the White House is not concerned with triggering intraday market vol.

- As such, trade deals and tariffs remain the focus for markets, particularly as even countries that were seen to have sealed agreements with the US – namely the UK – are still subject to tariff risk on August 1st.

- The USD Index is consolidating after the break back above downtrendline resistance drawn off the early February highs earlier in the week. CAD is the poorest performer on the day, while GBP is marginally stronger – but both currencies remain contained inside the recent range.

- The rip higher for EUR/JPY continued apace in APAC trade, with the cross rallying again to touch Y175.43 and the highest level since mid-July last year. This tips the 14-day RSI further into overbought territory, hitting 75 and signalling a further pick-up in upside momentum could be harder to come by without fresh external catalysts in the very near-term.

- Prices are fading somewhat into the NY crossover, however, tipping EUR/JPY off the overnight high and into minor negative territory.

- Final US wholesale inventories and trade sales data for May are the primary data releases Wednesday, however it’s the FOMC meeting minutes due at 1900BST/1400ET that should draw more focus – particularly concerning any discussion among the committee about a possible July rate cut.

TWD: Seasonality in Greater focus as TWD off Year’s Highs

- Spot USD/TWD is set to close higher again Wednesday, marking four consecutive positive closes for the first time since the bounce off lows after the 7% rout in early April. Perhaps more importantly, implied vols are fading further: 1m implied slipped back below 10 points today and, while still above the YTD average, is well off the elevated levels seen through the June, May spikes.

- August is historically the best performing calendar month of the year for USD/TWD, returning 0.42% on average over the past 25 years. This is closely tied to the pick-up in corporate activity via dividend payments (mentioned here: https://www.mnimarkets.com/articles/fx-inflows-remain-key-driver-could-heighten-importance-of-dividends-1750845150205 )

- SocGen write that the upcoming dividend season sees significant payouts ahead, and while they don’t anticipate a significant rebound in USD/TWD, they see the 42% foreign ownership of equities as a key driver for repatriation of dividends, which may weaken the TWD. As such, they have recommended holding a 3m 25-delta USD/TWD risk reversal, which profits on spot above 29.40.

- Beyond dividend payments season, SocGen see more appreciation pressure on TWD via strong AI demand and export momentum ahead (we wrote yesterday that Taiwanese exports to the US exhibited strong growth in June, with Chinese transshipments and tariff front-running a likely factor): https://www.mnimarkets.com/articles/vietnam-and-taiwan-exports-to-us-continue-to-grow-strongly-1751983932683

EQUITIES: E-Mini S&P Holding Onto Bulk of Recent Gains

- Recent gains in Eurostoxx 50 futures from the Jun 23 low still appear to be a potential bull reversal and the contract is holding on to its most recent gains. Price has traded through both the 20- and 50-day EMAs. The clear break of both averages strengthens a reversal theme. This opens 5486.00, the May 20 high and a bull trigger. On the downside, a break of 5194.00, the Jun 23 low, would reinstate a bearish theme.

- The trend condition in S&P E-Minis remains bullish and the contract is holding on to the bulk of its recent gains. Resistance at 6128.75, the Jun 11 high, has recently been breached. The break confirmed a resumption of the uptrend that started Apr 7. This was followed by a breach of key resistance and a bull trigger at 6277.50, the Feb 21 high. Sights are on 6356.12, a Fibonacci projection. Key support is at the 50-day EMA, at 6021.70.

COMMODITIES: Recent Weakness in Gold Results in Breach of Support at 50-Day EMA

- WTI futures maintain a softer tone following the reversal from the Jun 23 high, and recent gains still appear corrective. Support to watch is the 50-day EMA, at $65.09. The average has been pierced, a clear break of it would signal scope for a deeper retracement. This would expose $58.87, the May 30 low. Initial resistance to watch is $71.20, the 50.0% retracement of the Jun 23 - 24 high-low range. Key resistance is at $78.40, the Jun 23 high.

- Recent weakness in Gold resulted in a breach of the 50-day EMA, and a trendline drawn from the Dec 30 ‘24 low and connected to the Feb 28 low. A clear break of both trend tools would signal scope for a deeper correction, and open $3245.5, May 29 low. Note, the recovery from the Jun 30 low also highlights a possible false t-line break. A resumption of gains would refocus attention on $3451.3, Jun 16 high. The bear trigger is $3248.7, Jun 30 low.

| Date | GMT/Local | Impact | Country | Event |

| 09/07/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 09/07/2025 | 1100/1300 | EC De Guindos Closing Remarks At Conference | ||

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/07/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 09/07/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 09/07/2025 | 1800/1400 | *** | FOMC Minutes | |

| 10/07/2025 | 0600/0800 | *** | CPI Norway | |

| 10/07/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/07/2025 | 0600/0800 | *** | HICP (f) | |

| 10/07/2025 | 0700/0900 | ECB Cipollone Digital Euro Lecture | ||

| 10/07/2025 | 0800/1000 | * | Industrial Production | |

| 10/07/2025 | - | *** | Money Supply | |

| 10/07/2025 | - | *** | New Loans | |

| 10/07/2025 | - | *** | Social Financing | |

| 10/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 10/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 10/07/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 10/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 10/07/2025 | 1500/1600 | BOE Breeden On Climate Change | ||

| 10/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 10/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 10/07/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 10/07/2025 | 1715/1315 | Fed Governor Christopher Waller | ||

| 10/07/2025 | 1830/1430 | Fed's Mary Daly at MNI |