MNI US MARKETS ANALYSIS - Energy Costs Show in German CPI

Highlights:

- MNI projects German CPI at 2.7% Y/Y, with energy costs rising in the mid-7% range

- RBI's efforts to curb INR weakness prove shortlived as USDINR plumbs new record high

- USDJPY again tops Y160.00, but moire sanguine EURJPY market could keep lid on intervention speculation

US TSYS: Real Yields Driving Modest Decline In Treasury Yields

Treasuries are modestly firmer across the curve, extending Friday’s gains in cross-asset moves that were more typical of traditional risk-off periods, despite equity futures seeing a sizeable bounce off overnight lows. President Trump told the FT that the US could “take the oil in Iran” whilst the WSJ reports he is weighing a military operation to extract nearly 1,000lbs of uranium from Iran.

- Cash yields are 2.5-3.7bp lower from Friday’s close, with declines led by the belly.

- Declines in yields are led entirely in real terms, with the 5Y yield of -3.7bps for example driven by +0.2bp for the breakeven and -3.8bp for the real yield.

- TYM6 trades at 110-13+ (+08+) off an earlier high of 110-17+, on solid cumulative volumes of 445k.

- Friday’s equity pressure saw more traditional risk-off behavior with core fixed income firming, helping TYM6 lift off a fresh low of 109-24 early in the US session.

- Short-term gains have been corrective though, with resistance seen at 111-01+ (Mar 25 high), and a bear cycle remains in place with support at that 109-24 before 109-22+ (Fibo projection of Mar 10-13-18 price swing).

- Data: Dallas Fed mfg Mar (1030ET)

- Fedspeak: Fed Chair Powell in moderated discussion (1030ET, Q&A only), NY Fed’s Williams on economy (1600ET, text + Q&A) – see STIR bullet

- Bill issuance: US Tsy $89B 13W & $77B 26W bill auctions (1130ET)

- Politics: Trump in White House internship program photo (1015ET), Trump in policy meeting (1330ET), Trump in signing time (1600ET)

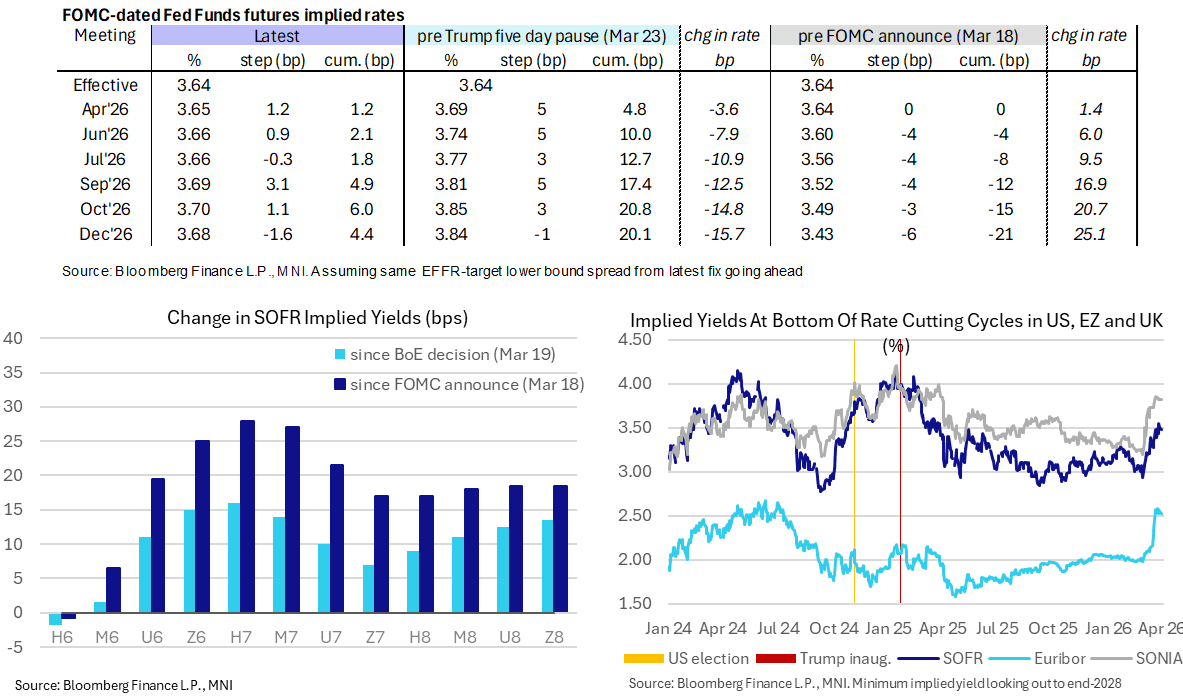

STIR: Higher Oil Prices Faded, Powell Update Headlines Calendar

- US rates are mildly firmer from Friday’s close as higher oil prices (WTI holding push above $100/bbl) appear to be seen increasingly seen in conjunction with downside growth risks per Friday's cross-asset price action. That's despite equity futures lifting notably off overnight lows.

- FF cumulative hikes from 3.64% effective: 1bp Apr, 2bp Jun, 2bp Jul, 5bp Sep, 6bp Oct and 4.5bp Dec.

- SOFR futures are up to 2.5 ticks firmer in 2027 contracts whilst the terminal implied yield at 3.48% (SFRZ7, -2.5bp) edges back below 3.50% after setting fresh highs since Mar 2025 last week.

- Today sees Fedspeak from two senior FOMC members, with Powell updating after the FOMC press conference less than two weeks ago and Williams with his first comments since Mar 3

- 1030ET - Fed Chair Powell (voter) in a moderated discussion at Harvard Principles of Economics Class (Q&A with moderator and audience). One of the surprises from the FOMC presser was that he addressed his future at the Fed after his Chairmanship is done in May, a subject he has been reluctant to speak about previously. He said he is prepared to continue to serve as Chair until his replacement (Kevin Warsh) is confirmed by the Senate (serving as Chair “pro tem” if his successor hasn’t yet been confirmed), and that he has “no intention of leaving the Board until the [Department of Justice] investigation [into the Fed] is well and truly over, with transparency and finality.” The bigger surprise was that “on the question of whether I will serve as a Governor after my term ends and the investigation is over, I have not made that decision yet.”

- 1600ET – NY Fed’s Williams (voter, leaning dove) speaks on the economy (text and Q&A, incl media availability). His Mar 3 speech reinforced that he is a dovish-leaning FOMC member, seeming to remain of the view that inflation is headed back to target - allowing for further rate cuts so that policy doesn't "inadvertently" become more restrictive. On the impact of the Middle East conflict on monetary policy: "We'll have to see how persistent this is and how long it is. It is early days to make the broader assessment”.

EUROPEAN INFLATION: MNI Projects 2.7% Y/Y German National CPI, Energy Mid-7%

From state-level data equating to 89.1% weighting of the national March flash German CPI print (due at 13:00 GMT / 14:00 CET), MNI estimates national CPI inflation of 1.1-1.2% M/M and around 2.7% Y/Y (1.9% prior). See the tables below for full calculations.

- Analyst consensus stands at 2.6% Y/Y (revised this morning from an earlier 2.7%, average currently 2.65%) and 1.1% M/M, with the uptick expectedly seen driven by energy inflation. Risks against these figures thus are skewed slightly to the upside.

- Current tracking of core CPI (ex-energy and food) implies a roughly unchanged print after the 2.5% Y/Y observed in February.

- Energy meanwhile is seen in the mid-7% range.

- Note: These estimates are in relation to the national CPI print, not the HICP print which feeds into the Eurozone HICP print that the ECB targets. The magnitude of surprises to consensus can sometimes be different due to the different methodologies and weights used in national CPI vs HICP (particularly since the change in HICP methodology this year). However, the direction of the surprise is generally the same.

| Y/Y | March (Reported) | February (Reported) | Difference |

| North Rhine Westphalia | 2.7 | 1.8 | 0.9 |

| Hesse | 2.9 | 2.2 | 0.7 |

| Bavaria | 2.8 | 1.9 | 0.9 |

| Brandenburg | 2.8 | 2.0 | 0.8 |

| Baden Wuert. | 2.5 | 1.8 | 0.7 |

| Berlin | 2.5 | 1.9 | 0.6 |

| Saxony | 2.8 | 2.3 | 0.5 |

| Rhineland-Palatinate | 2.9 | 1.9 | 1.0 |

| Lower Saxony | 2.6 | 1.9 | 0.7 |

| Saarland | 3.2 | 1.9 | 1.3 |

| Saxony-Anhalt | 2.6 | 2.0 | 0.6 |

| Weighted average: | 2.72% | for | 89.1% |

| M/M | March (Reported) | February (Reported) | Difference |

| North Rhine Westphalia | 1.2 | 0.2 | 1.0 |

| Hesse | 1.1 | 0.4 | 0.7 |

| Bavaria | 1.2 | 0.2 | 1.0 |

| Brandenburg | 1.1 | 0.4 | 0.7 |

| Baden Wuert. | 0.9 | 0.2 | 0.7 |

| Berlin | 1.1 | 0.4 | 0.7 |

| Saxony | 1.1 | 0.3 | 0.8 |

| Rhineland-Palatinate | 1.2 | 0.2 | 1.0 |

| Lower Saxony | 1.1 | 0.2 | 0.9 |

| Saarland | 1.4 | 0.3 | 1.1 |

| Saxony-Anhalt | 1.3 | 0.2 | 1.1 |

| Weighted average: | 1.14% | for | 89.1% |

STIR: ECB Pricing Just Below 80bp Of '26 Hikes

Growth concerns stemming from the elongation of the Iran conflict and spillover from slightly more guarded comments from the usually Hawkish ECB Executive Board member Schnabel have generated dovish moves in EUR STIRs since Friday’s Euribor settlement, outweighing the inflationary impact of the latest extension higher in crude oil. Note that the move has started to retrace, with bonds off highs.

- ECB-dated OIS pricing 78.5bp of tightening through year-end, with 15bp showing for April and 35.5bp priced through June. December pricing is ~2bp more dovish than pre-Schnabel levels, but ~5bp off this morning’s dovish extremes.

- Euribor futures 1.5-3.5bp firmer, with the front-end outperforming.

- As a reminder, Schnabel suggested that the Bank must "carefully weigh" its decisions and should not "overreact", but "if there is a more persistent impact on inflation, monetary policy will need to act, and it will act decisively".

- Over the weekend the centrist/dove Villeroy noted that the ECB is prepared to act to rein in inflation expectations but stressed that the Bank will be guided by data, with speculation surrounding specific dates for any movement “premature”.

- Today’s Eurozone sentiment survey data could get more interest than usual given the focus on Iran. Pay particularly attention to details surrounding pricing plans.

- Elsewhere, regional and national level German inflation data is due today. For the Eurozone-wide inflation reading, due tomorrow, core inflation is expected to be little changed or a touch lower than February’s 2.41% Y/Y. A handful of analysts note that the timing of Easter could add upside risks to some services, but that category is expected to be primarily driven by an unwind of Italian Olympic-related services pressures.

ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR (bp) |

Apr-26 | 2.078 | +14.8 |

Jun-26 | 2.285 | +35.5 |

Jul-26 | 2.443 | +51.3 |

Sep-26 | 2.592 | +66.2 |

Oct-26 | 2.671 | +74.1 |

Dec-26 | 2.715 | +78.5 |

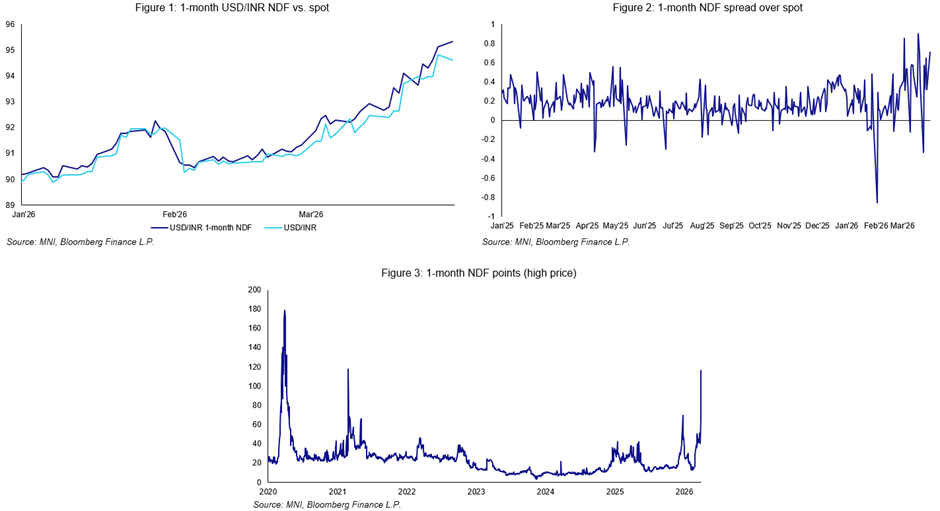

INDIA: RBI’s Position Limits Trigger Short Squeeze, But Rally Quickly Unwinds

The swift reversal of the INR spot move on the RBI's latest intervention points to growing market concern over the bank's options to combat currency weakness in the face of high oil prices and growing pressure from a swollen forward book, estimated to be nearing $100bn. INR rallied by as much as 1.4% at the open after the unexpected instruction to banks to cap net open INR positions at $100mn, replacing the previous limit of 25% of total capital and effectively forcing balance sheet compression. Banks have been given a tight deadline: compliance by April 10th.

- Complicating matters, the INR strength has almost fully reversed, highlighting the RBI’s increasingly constrained policy flexibility and, in particular, the pressure to preserve FX reserves. The surge in 1-month INR NDF points (hitting multi-year highs) indicates offshore markets are continuing to price sharp near-term weakness and tighter USD liquidity. The RBI therefore faces a trade-off: it can either roll over maturing forwards at a higher cost – tightening offshore USD liquidity further and potentially adding further upside pressure on USD/INR – or settle the contracts, which would further deplete FX reserves.

- The curbs announced Friday target basis-trade arbitrage, which had grown as offshore markets priced sharper INR weakness – partly due to the Iran war – relative to onshore markets. Banks were short INR offshore and long USD onshore, and since the RBI’s cap applies only to onshore positions, the measure forced an unwind, driving spot USD sales at Monday’s open. Reuters estimates these arbitrage positions at $25–35bn. Meanwhile, Bloomberg reports pushback from banks, warning that unwinding $30bn+ could generate substantial losses.

- The subsequent rebound in USD/INR – now approaching Friday’s record highs – highlights the dominance of underlying macro pressures on the rupee. In particular, the energy price shock constitutes a significant terms-of-trade shock for India, which imports around 90% of its oil consumption. Bloomberg also notes that oil importers took advantage of Monday’s dip to buy USD at more favourable levels, further accelerating the pair’s recovery.

FOREX: Bullish DXY Theme Intact, NZDUSD Approaching 2026 Lows (1/2)

- Mixed performance across the G10 to start the week, as broad dollar strength is offset by a pull lower for USDJPY, resulting in the USD index trading in moderate positive territory ahead of the NY crossover. The steady greenback ascent over the latter half of last week keeps the bullish DXY theme firmly intact, and hovering just below a key resistance cluster around the 100.50 mark.

- Despite the modest recovery for equities, higher crude futures continue to emphasise the uncertain geopolitical backdrop, and the likes of AUD and NZD are falling on Monday to reflect this. For AUDUSD, this will be the eighth consecutive session with lower highs as the pair extends its pullback from its cycle peak to 4.6%.

- Downside momentum accelerated on a close below the 50-day EMA, undermining the recent bull theme and signalling scope for a deeper retracement. Further out, important trendline (drawn from the Apr 9 ‘25 low) support lies at 0.6705.

- For NZDUSD, spot is now just 10 pips shy of the lowest levels of the year at 0.5711. Elsewhere, despite some two-way price action in the major pairs, EURUSD and GBPUSD have slipped back below 1.15 and 1.3250 respectively, as the trend structures for both pairs remain in bearish territory.

- Offsetting the underlying dollar strength to start the week has been a notable bounce for the Japanese yen, helping USDJPY reverse from its 160.46 cycle highs and trade back below the psychological 160.00 mark. Session lows of 159.57 remain well shy of initial firm support at 157.28, the 50-day EMA.

- Japan’s top currency diplomat Atsushi Mimura was back on the wires Monday, stating that "decisive action may soon be necessary" if speculative moves persist in the currency market. “We are prepared to respond on all fronts, and our focus is broad and comprehensive,” Mimura added.

- While newswires are attributing the move lower for USDJPY to the comments, it’s worth highlighting that Mimura struck a very similar tone last week, detailing that authorities are ready to act “on all fronts,” suggesting they might look beyond currencies to areas including crude oil futures.

- This rhetoric was reinforced by Finance Minister Katayama who stated that speculative trading of crude futures is affecting FX, and the government can take market measures on all fronts, while alluding to close coordination with foreign authorities.

- While the verbal jawboning may have contributed, it is more likely that fresh yen shorts on a break of 160.00 may have been squeezed, potentially exacerbating the price action, while market participants also remain aware of the waning risk/reward profile up here.

OPTIONS: Expiries for Mar30 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1450(E819mln), $1.1550(E913mln), $1.1650(E515mln), $1.1700(E1.0bln)

- GBP/USD: $1.3400(Gbp511mln)

- USD/CAD: C$1.3500($734mln)

EQUITIES: E-Mini S&P Falls to Fresh 7-Month Low, Before Rebounding

- The trend condition in EuroStoxx 50 futures remains bearish and recent gains appear to have been corrective. Note that the S/T trend condition is oversold and a stronger recovery would allow this set-up to unwind. Key pivot resistance is seen at 5750.42, the 50-day EMA. A fresh cycle low on Mar 20 and 23 confirmed a resumption of the bear cycle. The break lower signals potential for an extension towards 5277.64 next, a Fibonacci projection.

- A bear trend in S&P E-Minis remains intact and last week’s sell-off reinforces current conditions. A fresh cycle low confirms a resumption of the downtrend. Note that moving average studies remain in a bear-mode position, highlighting a dominant downtrend. This opens 6316.61 next, a Fibonacci projection. Initial firm resistance is at 6699.10, the 20-day EMA. Resistance at the 50-day EMA is at 6819.71.

EQUITIES: WTI Back Above $100/bbl, Sights on $104.50 Fibo Retracement

- A bull wave in WTI futures remains intact and the sharp pullback on Mar 23 has proved to be corrective. A key support zone to monitor is the area between $88.25 - $77.61, the 20- and 50-day EMA values. The 20-day average has been pierced, but remains intact for now. A clear break of this support zone is required to signal a possible trend reversal. On the upside, sights are on $104.50, a Fibonacci retracement.

- Short-term trend signals in Gold are unchanged, they remain bearish and the recovery from the Mar 23 low, is considered corrective. Note that the downtrend is in oversold territory and a stronger corrective bounce would allow this condition to unwind. Initial resistance is at $4655.7, the Feb 6 low. Key near-term resistance is at $4818.6, the 50-day EMA. For bears, a resumption of the bear leg would open $3945.2, a Fibonacci projection.

| Date | GMT/Local | Impact | Country | Event |

| 30/03/2026 | 1200/1400 | *** | Germany CPI (p) | |

| 30/03/2026 | 1200/1400 | *** | Germany CPI (p) | |

| 30/03/2026 | 1430/1030 | Fed Chair Jerome Powell | ||

| 30/03/2026 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 30/03/2026 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 30/03/2026 | 2000/1600 | New York Fed's John Williams | ||

| 31/03/2026 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 31/03/2026 | 2330/0830 | ** | Tokyo CPI | |

| 31/03/2026 | 2330/0830 | * | Labor Force Survey | |

| 31/03/2026 | 2350/0850 | ** | Industrial Production | |

| 31/03/2026 | 2350/0850 | * | Retail Sales (p) | |

| 31/03/2026 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/03/2026 | 0130/0930 | ** | CFLP Non-Manufacturing PMI | |

| 31/03/2026 | 0600/0700 | *** | GDP Second Estimate | |

| 31/03/2026 | 0600/0700 | * | Quarterly current account balance | |

| 31/03/2026 | 0600/0800 | ** | Retail Sales | |

| 31/03/2026 | 0600/0800 | ** | Import/Export Prices | |

| 31/03/2026 | 0645/0845 | *** | HICP (p) | |

| 31/03/2026 | 0645/0845 | ** | Consumer Spending | |

| 31/03/2026 | 0645/0845 | ** | PPI | |

| 31/03/2026 | 0755/0955 | ** | Unemployment | |

| 31/03/2026 | 0900/1100 | *** | EZ HICP Flash | |

| 31/03/2026 | 0900/1100 | *** | EZ HICP Flash | |

| 31/03/2026 | 0900/1100 | *** | EZ HICP Flash | |

| 31/03/2026 | 0900/1100 | *** | EZ HICP Flash (2dp) | |

| 31/03/2026 | 0900/1100 | *** | Italy Flash Inflation | |

| 31/03/2026 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/03/2026 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/03/2026 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 31/03/2026 | 1300/0900 | ** | FHFA Home Price Index | |

| 31/03/2026 | 1300/0900 | ** | FHFA Home Price Index | |

| 31/03/2026 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/03/2026 | 1400/1000 | *** | JOLTS | |

| 31/03/2026 | 1400/1000 | *** | JOLTS | |

| 31/03/2026 | 1400/1000 | *** | Conference Board Consumer Confidence | |

| 31/03/2026 | 1600/1200 | Chicago Fed's Austan Goolsbee | ||

| 31/03/2026 | 1710/1310 | Kansas City Fed's Jeff Schmid | ||

| 31/03/2026 | 1900/1500 | Fed Governor Michael Barr | ||

| 31/03/2026 | 2110/1710 | Fed Vice Chair for Supervision Michelle Bowman | ||

| 01/04/2026 | 2200/0900 | ** | S&P Global Manufacturing PMI (f) |