MNI US MARKETS ANALYSIS - BoE Seen Cutting 25, Comms in Focus

Highlights:

- Treasury curve sits bear flatter ahead of expected Trump announcement on UK trade deal

- BoE expected to trim 25bps off bank rate, with a focus on communications

- Norway, Sweden central banks keep rates unchanged

US TSYS: Bear Flatter On US-UK Trade Expectations

- Treasuries are bear flatter on the day reflecting advances in UK-U.S. trade talks ahead of an announcement today at 1000ET plus yesterday’s suggestions that the U.S. is set to relax export restrictions for chips.

- Aside from politics and trade policy in particular, today’s data is headlined by weekly jobless claims after upward surprises last week including continuing claims pushing above well-defined ranges. Productivity and ULCs for Q1 will appear particularly stale.

- There could also be some spillover from a BoE decision due shortly at 0700ET whilst the long end of the curve will see a latest test of duration demand with 30Y supply at 1300ET.

- Cash yields are 3-5bp higher across the curve, led by the belly.

- TYM5 trades at 111-09 (-08+) having pulled back off brief post-FOMC highs of 111-22 (seen prior to Powell’s press conference). It comes with another overnight session of very low volumes, currently at just 225k cumulative.

- Treasury futures are more stable off recent lows, however the latest pullback has undermined the recent bull cycle. Resistance is seen at 112-01+ (May 2 high) and support at 110-27+ (May 6 low).

- Data: Weekly jobless claims (0830ET), Productivity/ULCs Q1 prelim (0830ET), Wholesale trade sales/inventories Mar/Mar F (1000ET), NY 1Y inflation expectations Apr (1100ET)

- Fedspeak: Last day of media blackout – multiple speakers lined up for tomorrow

- Coupon issuance: US Tsy $25B 30Y Bond - 912810UK2 (1300ET)

- Bill issuance: US Tsy $85B 4W & $75B 8W bill auctions (1130ET), $25B 16-Day CMB auctions (1300ET)

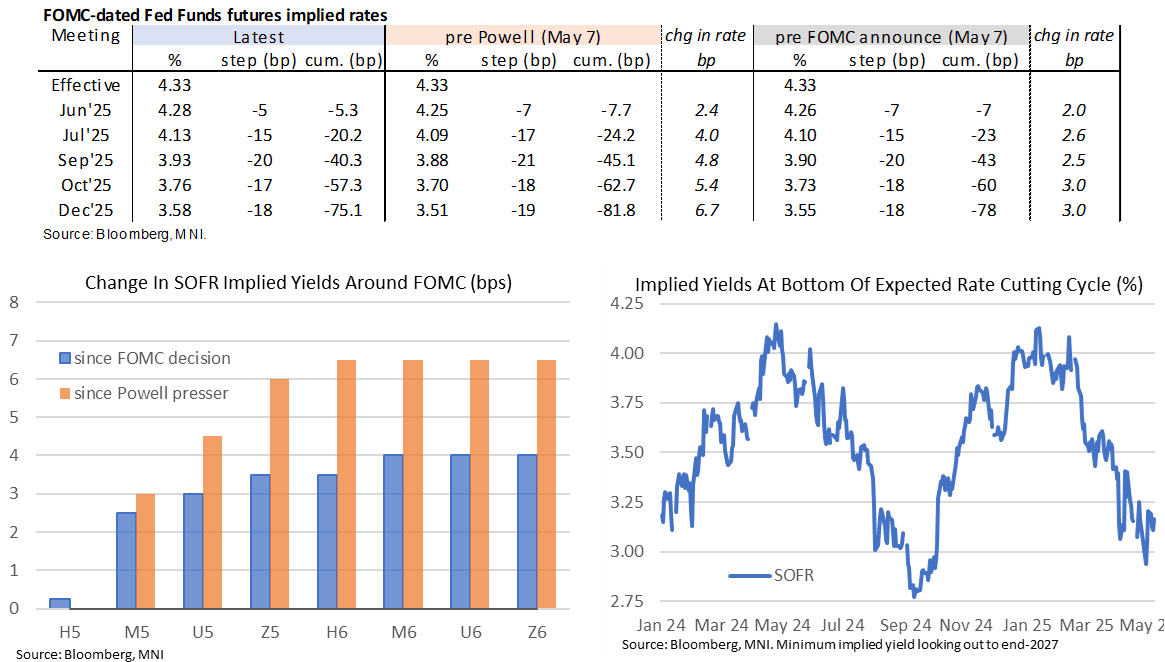

STIR: Fed Rate Path Climbs After FOMC On Trade Deal Prospects

- After relatively little net reaction immediately on yesterday’s FOMC announcement and Chair Powell’s press conference, Fed Funds implied rates have pushed solidly higher overnight with the Dec’25 rate +3.5bps on the day.

- Cumulative cuts from 4.33% effective: 5.5bp Jun, 20bp Jul, 40bp Sep, 57bp Oct and 75bp Dec.

- The main driving force appears to be advances in UK-U.S. trade talks ahead of an announcement today at 1000ET plus yesterday’s suggestions that the U.S. is set to relax export restrictions for chips. There could also be some extended reaction to Powell’s press conference from Asia and Europe participants but we expect that’s marginal.

- The FOMC as always remains in media blackout today with focus on weekly jobless claims after last week’s surprise increase for both initial and continuing, before the aforementioned US trade deal announcement.

- SOFR futures sees implied yields bottoming out at 3.165% (back in U6 and Z6 after just Z6 yesterday) although that would only be the highest close since Monday.

- MNI Fed Review here.

FED: MNI Fed Review - May 2025: Firmly In Wait And See Mode

- We have published and e-mailed to subscribers the MNI Fed Review from yesterday's meeting.

- Please find the full report including MNI analysis and a summary of rate views from 26 analysts here: https://media.marketnews.com/Fed_Review_May2025_b4e15db4cd.pdf

US TSY FUTURES: Cover Dominated On Wednesday

OI data points to a mix of net long cover (TU), short cover (FV, TY & USY) and long setting (US & WN) during Wednesday’s twist flattening of the curve.

- The curve-wide positioning bias was tilted comfortably towards cover of existing positions, with the short cover in the belly/intermediates most prominent.

| 07-May-25 | 06-May-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,085,950 | 4,097,367 | -11,417 | -418,270 |

FV | 6,872,658 | 6,912,252 | -39,594 | -1,695,768 |

TY | 4,933,604 | 4,956,188 | -22,584 | -1,456,211 |

UXY | 2,284,600 | 2,291,350 | -6,750 | -594,829 |

US | 1,799,369 | 1,794,267 | +5,102 | +648,472 |

WN | 1,888,661 | 1,888,335 | +326 | +59,900 |

|

| Total | -74,917 | -3,456,707 |

STIR: Mix Of Positioning Swings Seen Across SOFR Futures On Wednesday

OI data points to a mix of positioning swings during the twist flattening of the SOFR futures strip on Wednesday.

- A mix of net short setting and long cover was seen across the front 5 contracts, before net long setting and short cover were seen further out.

| 07-May-25 | 06-May-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRH5 | 1,076,531 | 1,081,653 | -5,122 | Whites | -17,347 |

SFRM5 | 1,234,292 | 1,249,662 | -15,370 | Reds | +6,658 |

SFRU5 | 1,005,202 | 1,008,902 | -3,700 | Greens | +14,930 |

SFRZ5 | 1,081,026 | 1,074,181 | +6,845 | Blues | +8,584 |

SFRH6 | 748,397 | 740,428 | +7,969 |

|

|

SFRM6 | 736,416 | 720,590 | +15,826 |

|

|

SFRU6 | 717,989 | 718,726 | -737 |

|

|

SFRZ6 | 838,864 | 855,264 | -16,400 |

|

|

SFRH7 | 665,569 | 665,749 | -180 |

|

|

SFRM7 | 564,282 | 555,148 | +9,134 |

|

|

SFRU7 | 365,160 | 364,756 | +404 |

|

|

SFRZ7 | 402,225 | 396,653 | +5,572 |

|

|

SFRH8 | 279,209 | 275,121 | +4,088 |

|

|

SFRM8 | 192,582 | 190,833 | +1,749 |

|

|

SFRU8 | 151,742 | 149,633 | +2,109 |

|

|

SFRZ8 | 159,189 | 158,551 | +638 |

|

|

RIKSBANK: Few Revelations In Monetary Policy Update; Focus On Press Conference

There aren't any huge revelations in the Riksbank's Monetary Policy Update that weren't outlined in the policy statement (some highlights below). For now, focus turns to Governor Thedeen's press conference at 1000BST/1100CET.

- "According to surveys, household confidence has fallen significantly, while business confidence is relatively unchanged so far. Anecdotal information, including interviews with businesses, suggests increased pessimism among businesses too. The generally increased uncertainty is also expected to contribute to lower exports and investment"

- "The weaker growth prospects risk leading to slightly higher unemployment in the period ahead than was in the March forecast"

- “In March, the Riksbank identified a number of factors that are expected to mean that inflation will be above 2 per cent this year before falling back”…” The inflation prospects for the rest of the year from the March report are largely expected to remain unchanged”.

- “New agreements suggest wage increases broadly in line with the previous assessment”…”This is not assessed to change the inflation outlook to any great extent compared with the forecast from March”.

RIKSBANK: Not Enough Of A Dovish Tilt To Prompt Repricing Of Cut Expectations

Limited reaction in SEK crosses to the slight dovish tilt in the Riksbank policy statement, with the overall tone still very non-committal and heavily caveated at this stage.

- Overall, there isn’t enough of a signal from the Riksbank to prompt a meaningful repricing in Riksbank rate cut expectations, even if the March MPR rate path was flat at 2.25% throughout the policy horizon.

- We continue to view a June cut as in play, but will need to be supported by the hard data between now and the June 18 decision.

- The key line in the statement is “even though uncertainty is significant, the Executive Board assesses that it is somewhat more probable that inflation will be lower than that it will be higher than in the March forecast. This could suggest a slight easing of monetary policy going forward”.

FOREX: Firmer USD Theme Plays Out, Threatening EUR, GBP Consolidation Phases

- The ripple effect of the hawkish Fed yesterday continues to be felt across G10 FX early Friday, with the dollar stronger against all others in G10. USD/JPY has made light work of yesterday's highs and is narrowing in on the next key upside levels at Y145.08 and the bull trigger of Y145.92. Powell's defence of the Fed's policy plans for 2025 reinforced to markets that the Fed won't be pressured or rushed into easing rates this year, adding some pressure to market pricing - ~75bps of easing are now priced for 2025, down from 80bps this time yesterday.

- USD gains are keeping EUR/USD tilted toward recent lows, and well within range of horizontal support at 1.1266. Clearance through here would be a bearish signal, opening levels last seen in early April and turning focus to 1.1110, the 38.2% retracement of the tariff upleg for direction.

- The White House and Downing Street are expected to unveil details of their tariff-reducing trade deal later today - which would be the first since the 90-day tariff delay outlined by Trump a few weeks ago. GBP has seen little reprieve despite local equities seeing early gains. GBP/USD is back below the $1.3300 handle, marking support at 1.3234, a break below which would end the two-week consolidative phase in the pair. Announcements on trade are expected from 1000ET/1500BST.

- The Bank of England are expected to cut rates by 25bps to 4.25% at today's 1202BST rate decision. Focus will be on the language used in the subsequent press conference with Bailey - and in particular whether the phrasing around "gradual" easing will be removed - signalling potential for a faster pace of rate cuts ahead.

- Weekly US jobless claims and the Bank of Canada's Financial Stability Report are then set to cross.

OPTIONS: Expiries for May08 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1200(E2.8bln), $1.1220-25(E1.2bln), $1.1250(E1.6bln), $1.1300(E1.0bln), $1.1350(E817mln), $1.1390-00(E3.6bln), $1.1420-25(E1.3bln)

- USD/JPY: Y140.00($4.1bln), Y142.00($1.2bln), Y143.00($1.7bln), Y145.00($1.5bln)

- GBP/USD: $1.3380-00(Gbp810mln)

- EUR/JPY: Y162.20-25(E520mln)

- NZD/USD: $0.6025(N$616mln)

- USD/CNY: Cny7.1500($954mln), Cny7.4500($1.5bln)

EQUITIES: Eurostoxx 50 Futures Maintain Bullish Tone, Close to Recent Highs

Eurostoxx 50 futures maintain a bullish tone and the contract is trading at its recent highs. Price has recently cleared both the 20- and 50-day EMAs, and attention is on 5263.01, 76.4% of the Mar 3 - Apr 7 bear leg. This hurdle has recently been pierced, a clear break of it would pave the way for a climb towards 5341.00, the Mar 27 high. Initial support to watch lies at 5093.95, the 20-day EMA. Clearance of this level would signal a possible reversal. Trend conditions in S&P E-Minis are unchanged, they remain bullish. The contract has breached the 50-day EMA, at 5624.12. A continuation higher would expose 5837.25 next, the Mar 25 high and a bull trigger. It is still possible that the entire rally since Apr 7 is a correction. A reversal lower would signal the end of this corrective phase and expose initially, support at 5127.25, the Apr 21 low. First support to watch is 5547.58, the 20-day EMA.

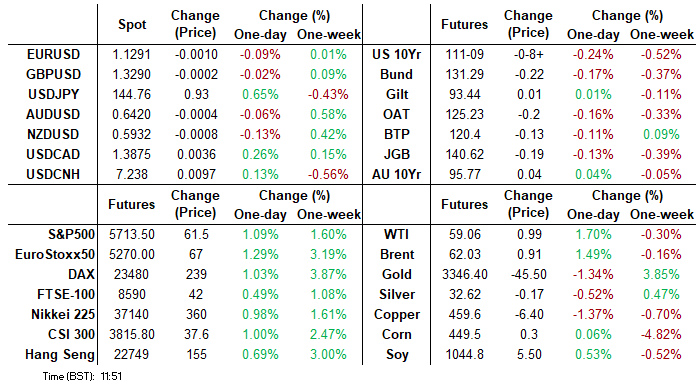

- Japan's NIKKEI closed higher by 148.97 pts or +0.41% at 36928.63 and the TOPIX ended 2.56 pts higher or +0.09% at 2698.72.

- Elsewhere, in China the SHANGHAI closed higher by 9.331 pts or +0.28% at 3351.996 and the HANG SENG ended 84.04 pts higher or +0.37% at 22775.92.

- Across Europe, Germany's DAX trades higher by 229.92 pts or +0.99% at 23345.01, FTSE 100 higher by 22.35 pts or +0.26% at 8581.84, CAC 40 up 65.3 pts or +0.86% at 7691.61 and Euro Stoxx 50 up 56.42 pts or +1.08% at 5285.96.

- Dow Jones mini up 266 pts or +0.65% at 41483, S&P 500 mini up 51 pts or +0.9% at 5703, NASDAQ mini up 256 pts or +1.28% at 20217.25.

COMMODITIES: Short-Term WTI Future Gains Still Considered Corrective

A downtrend in WTI futures remains intact and short-term gains are considered corrective. The move down that started Apr 23 signals the end of the correction between Apr 9 - 23. That cycle higher allowed an oversold condition to unwind. Attention is on $54.67, the Apr 9 low and a bear trigger. Clearance of this level would resume the downtrend and open $53.72, a Fibonacci projection. Key resistance to watch is $63.88, the 50-day EMA. Gold has recovered from its recent lows. The rally suggests the correction between Apr 22 - May 1, is over. A continuation higher would refocus attention on key resistance and the bull trigger at $3500.1, the Apr 22 high. Clearance of this level would confirm a resumption of the primary uptrend. Key short-term support has been defined at $3202.0, the May 1 low. A break of this level is required to signal scope for a deeper retracement.

- WTI Crude up $0.49 or +0.84% at $58.54

- Natural Gas up $0.04 or +0.99% at $3.656

- Gold spot down $26.21 or -0.78% at $3338.74

- Copper down $6.85 or -1.47% at $458.9

- Silver down $0.13 or -0.41% at $32.327

- Platinum down $2.32 or -0.24% at $976.61

| Date | GMT/Local | Impact | Country | Event |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1130/1230 | BOE Press Conference | ||

| 08/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 08/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 08/05/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/05/2025 | 1300/1400 | Decision Maker Panel data | ||

| 08/05/2025 | 1400/1000 | BOC Financial Stability Report and Financial System Survey | ||

| 08/05/2025 | 1400/1000 | ** | Wholesale Trade | |

| 08/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 08/05/2025 | 1500/1100 | BOC Governor Macklem press conference on Financial System Review | ||

| 08/05/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 08/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 08/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 08/05/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 08/05/2025 | 1700/1300 | * | US Treasury Auction Result for Cash Management Bill | |

| 09/05/2025 | 2330/0830 | ** | average wages (p) | |

| 09/05/2025 | 2330/0830 | ** | Household spending | |

| 09/05/2025 | 0600/0800 | *** | CPI Norway | |

| 09/05/2025 | 0800/1000 | * | Industrial Production | |

| 09/05/2025 | 0840/0940 | BOE Bailey Keynote Address at Reykjavik Economic Conference | ||

| 09/05/2025 | 0955/0555 | Fed Governor Michael Barr | ||

| 09/05/2025 | 1045/0645 | Fed Governor Adriana Kugler | ||

| 09/05/2025 | 1115/1215 | BOE's Pill At National MPC Agency Briefing | ||

| 09/05/2025 | - | *** | Trade | |

| 09/05/2025 | 1230/0830 | *** | Labour Force Survey | |

| 09/05/2025 | 1230/0830 | New York Fed's John Williams | ||

| 09/05/2025 | 1230/0830 | *** | Labour Force Survey | |

| 09/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin | ||

| 09/05/2025 | 1235/0835 | New York Fed's Roberto Perli | ||

| 09/05/2025 | 1530/1130 | Fed Governor Christopher Waller | ||

| 09/05/2025 | 1530/1130 | New York Fed's John Williams | ||

| 09/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 09/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |