MACRO ANALYSIS: MNI US Macro Weekly: The Fog Of Warsh

Jan-30 22:00

We've just published our US Macro Weekly - Download Full Report Here

- The largest rate moves of the week surrounded President Trump’s selection of former Fed Governor Kevin Warsh as the next Fed chair when Powell’s term in the position ends in May.

- A next Fed cut is close to being fully priced for the June meeting again (22bp, the first meeting under the new Fed chair) whilst there are two 25bp cuts fully priced by year-end.

- While historically more hawkish than most of the other contenders but also favoring economic productivity arguments for expecting inflation to remain in check amid solid growth, there remains high uncertainty on what the Fed might look like under Warsh’s leadership. (More from our Policy Team on page 18.)

- That includes policy on the balance sheet (preferring a smaller one) and communications, the Fed’s reach outside of core monetary policy channels, and even personnel, having previously said "I think what we need is regime change at the Fed, and that's not just about the Chairman, it's about a range of people...it's about breaking some heads, because the way they've been doing business is not working."

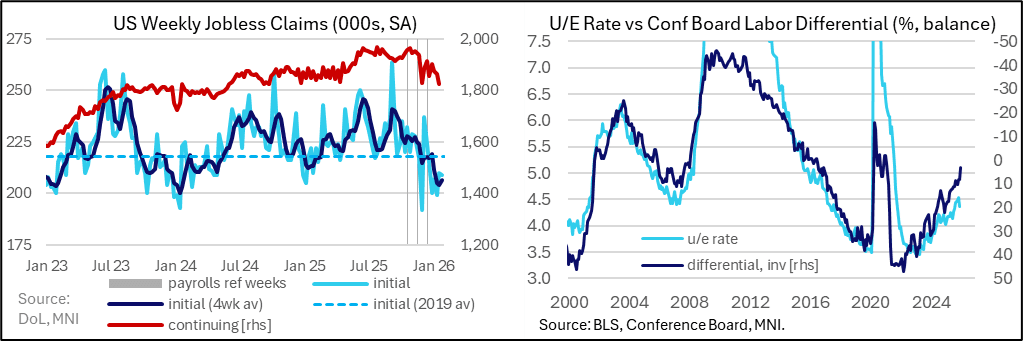

- Warsh or not, one impetus for consensus on a resumption of Fed easing would be a clear deterioration in the labor market, but here the data evidence remained mixed. Jobless claims remain at a healthy level despite initial claims surprising higher for the first time since Dec 11 after a particularly impressive run but with residual seasonality concerns. Continuing claims pushed lower still however but also with some questions over the role of unemployment insurance eligibility roll-off.

- A further acceleration of strong core PPI inflation trends had little impact on Friday against a backdrop of precious metal prices tumbling, whilst details confirmed strong core PCE estimates at ~0.4% M/M for Dec.

- Real GDP growth tracking for Q4 has been trimmed from 5.4% to a still very strong 4.2% after latest volatility in monthly trade reports. Capital goods imports are up strongly in tech-led strength but consumer and industrial imports are down heavily in a hangover from tariff front-running in Q1.

- Manufacturing firms’ sentiment firmed in January but consumer confidence slumped, with the lowest Conference Board metric since 2014 as consumer labor market perceptions softened further.

- The FOMC treaded a largely neutral path with its January decision, maintaining its easing bias but sounding slightly more patient in making its next move than it did last month. Markets took a very mildly hawkish interpretation with implied rates rising under 1bp for meetings to July but even less of a move further out, and the dollar remaining largely unmoved.

- Looking ahead, another government shutdown looms, starting Saturday, but with questions over its potential duration and breadth. In the event the BLS isn’t impacted, the nonfarm payrolls report for January will highlight the week’s economic data on Friday. The report will include benchmark revisions and will continue to see attention on the unemployment rate after its recent stalling around the 4.4% mark.

- We also get Treasury’s quarterly financing and borrowing updates, with attention on any revisions to its guidance on future increases in auction sizes.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

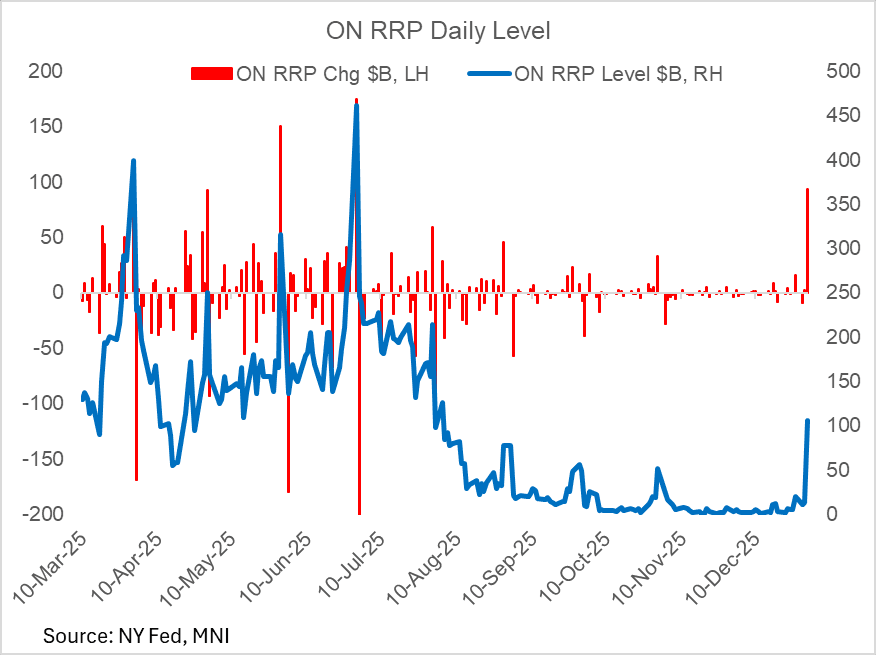

US TSYS/OVERNIGHT REPO: ON RRP Soars At Year-End, Well Below Prior Year's Level

Dec-31 18:22

Month-/quarter-/year-end brings a jump in Fed reverse repo takeup, to $106.0B. The $93B jump from the prior session is the biggest since May's $150B; the level is the highest since August.

- Of course, this is due to reverse sharply in coming sessions, and the takeup level is far below the $473B seen at year-end 2024.

US TSYS: Volume Jumps Into Year End

Dec-31 18:14

A 6+ tick dip in TYH6 accompanies the CME floor close for the New Year's holiday, to a session-low 112-10+ (a level last seen on Dec 24).

- After light volumes throughout the morning, a burst of around 400k contracts trade into the month end to a daily volume of 1.13M.

- Prices are stabilizing (last 112-12+), though as we noted earlier, from a technical perspective 111-29 would confirm a resumption of the bear cycle.

- SIFMA recommends a cash close at 2pm ET; Globex is open until 4pm ET.

US TSYS: Wrapping Up 2025

Dec-31 17:48

- Treasuries reversed early support after the final weekly claims data for 2025 came out lower than expected Wednesday, rather a decent range on moderate volumes ahead of the early close for the New Year's Eve holiday (1300ET; 1600ET Globex), re-open/electronic trade Thursday evening for Friday's order of business.

- TYH6 currently trades 112-17 (-3.5) vs. 112-14 low, curves mixed: 2s10s +.738 at 67.887, 5s30s -.890 at 111.961.

- The technical trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection. Key short-term resistance has been defined at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

- Treasury yields slipped overnight in reaction to additional tariffs on beef by China: the US will have to pay 55% additional tariffs on beef exports to China, above its specified quota (164k tons a year in 2026). 10Y yield tapped a low of 4.1024% before climbing to 4.1513% high following the jobless claims data.

- Initial jobless claims for the Dec 27 week were much lower than expected at 199k, vs the 218k consensus (215k prior rev from 214k). This marked the lowest level of seasonally-adjusted initial claims since the Nov 29 week, though it is for that reason that we suggest caution: both are holiday weeks (the other is Thanksgiving) which typically translates into volatility in claims.

- Meanwhile continuing claims for the Dec 20 week came in at 1,866k (1,902k consensus, 1,913k prior rev from 1,923k), marking a 3-week low but still in the recent ranges. NSA claims dropped 103k to 1,881k, and like initial, we would expect a large pickup the following week.