MNI US Employment Insight: Payrolls Take A Misstep

Mar-06 20:54By: Tim Cooper and 1 more...

Employment+ 2

Download Full Report Here

EXECUTIVE SUMMARY:

- Key figures in both the establishment and household surveys disappointed in the February payrolls report although it must be seen in the context of strong January report. Indeed, even the most dovish FOMC member, Governor Miran, cautioned against reading too much into one month's job report.

- It still acts as a dovish surprise though as it firmly pushes back on any more optimistic views of the labor market going into this report.

- The themes broadly flagged ahead of the report were as expected although the magnitude was surprising. There were two healthcare-related hits, one fully expected (31k strikes) and one less so (potential reversal after a severe flu season in January), whilst adverse weather might well have played a role but was still hard to square away the extent of industries reporting job losses.

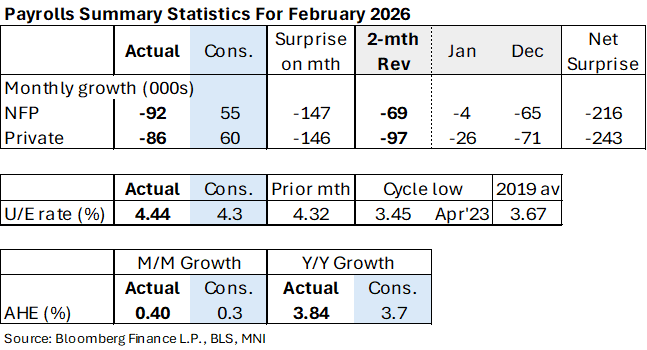

- Nonfarm payrolls fell -92k (cons 55k) after 126k as part of heavy negative revisions of -69k, leaving a three-month average of 6k and six-month average of -1k. Private payrolls fell -86k (cons 60k) after 146k with a three-month average of 18k and six-month average of 34k, whilst private ex health & social assistance sees a three-month average of -29k and six-month of -16k after sizeable declines last year.

- The household survey brought some meaningful surprises and oddities, in terms of both the monthly data and the annual population control revisions. Understanding February dynamics depends largely on figuring in the annual revisions, though overall February's household report looked largely weak.

- For a household survey bottom line, the u/e rate surprised higher in Feb at 4.44% (cons 4.3 with dovish risk tilted to a 4.4) after an upward revised but what would still have surprised lower 4.32% in Jan. The latter was first reported at 4.28% vs then consensus of 4.4%, before unusually being revised with the delayed population control back on January levels.

- Average the two monthly prints and the 4.38% sits between the heavily caveated 4.47% averaged in Q4 (government shutdown disruption) and 4.34% in Q3.

- That broad stability continues to defy a scenario that the most dovish FOMC members had envisaged back in the December SEP (seven members pencilled in an u/e rate at 4.6-4.7% in 4Q25), with some of these prominent members since dialling back cut calls/rhetoric over the past month.

- In a reminder of the risk in putting too much weight on single reports, response rates were at best mixed. The household survey response rate increased from three months of record lows but remains depressed and leaves it prone to higher than usual month-to-month volatility, whilst first responses for payrolls data slid back to very low levels and leave scope for larger revisions.

- Whilst heavily clouded by today's surge in WTI futures and two-way swings in rates since the release, there has been a net dovish shift with June Fed Funds implied rates 4bp lower post-release and Dec 8bp lower. A next Fed cut is seen in September in a close call with July (22bp) and with 45bp of cuts seen for 2026.