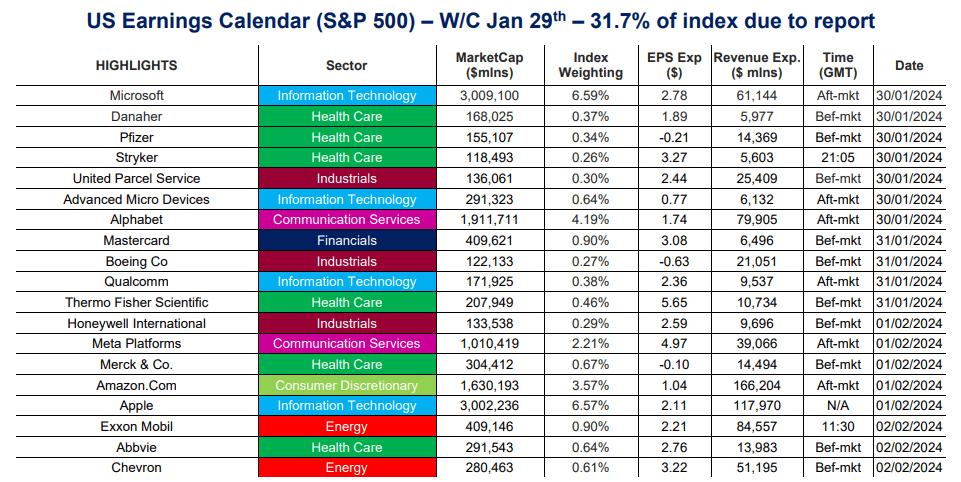

EQUITIES: MNI US EARNINGS SCHEDULE - Busiest Week of the Quarter

- With 20% of the S&P 500 having reported for Q4’23 earnings, firms continue to beat expectations on both EPS and sales metrics, with average EPS 6.3% ahead of forecast, and average revenues 0.4% above.

- Financials have dominated the season so far, with the sector beating on EPS (6.8% ahead of expectations), but revenues broadly inline. Early reports from consumer discretionary names are faring less well, missing on EPS and sales estimates.

- Several trillion-dollar companies report in the coming week, with Alphabet, Microsoft, Meta Platforms, Amazon.com and Apple all on the docket.

Full earnings schedule including EPS & revenue expectations and timings here: https://roar-assets-auto.rbl.ms/files/59689/MNIUSE...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUNDS: 1.90% Holds In 10-Year Yields, Space Off Best Levels

As noted elsewhere, we don’t have much to point to when it comes to news flow re: the move away from best levels in Bunds. We can only offer the hold of round number support in 10-Year yields (with 1.90% essentially holding almost to the bp given lows of 1.899% were seen) as an ‘explainer.’ After that, apparent peripheral widener flow and the Italian headlines flagged elsewhere came to the fore.

STIR: Dovish Move In EUR STIRs Limited As EGBs Tick Away From Best Levels

The drift away from best levels in long end EGBs also helps EUR STIR markets away from best levels.

- Euribor futures last show +1.0 to +5.5bp through the blues.

- ECB-dated OIS is +1bp to -2bp on the day. The strip shows ~167bp of cuts through ’24 as of typing, indicating greater than even odds of the first 25bp cut coming by the end of the March ’24 gathering.

- Spill over from BoE pricing and the previously covered bid in benchmark EGBs allowed the space to trade in a dovish manner early on Wednesday.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Jan-24 | 3.886 | -1.3 |

| Mar-24 | 3.734 | -16.5 |

| Apr-24 | 3.493 | -40.6 |

| Jun-24 | 3.166 | -73.4 |

| Jul-24 | 2.868 | -103.1 |

| Sep-24 | 2.607 | -129.2 |

| Oct-24 | 2.411 | -148.8 |

| Dec-24 | 2.227 | -167.2 |

BTP: Away From Best Levels, Periphery Widens

While BTP futures had already turned away from best levels alongside Bunds, soundbites from the Italian Economy Minister (no need to redraft budget to comply with EU fiscal rules and an apparent lack of willingness when it comes to greenlighting ESM reform) may be filtering in to BTP trade, via channels related to intra-EU tension.

- This also comes with wider peripheral widening vs. Bunds after an impressive ’23 for most related compression trades, so could represent more of a profit taking type exercise.

- BTP futures now show +30 or so on the day around 120.96, ~50 ticks shy of fresh cycle highs printed earlier today.

- The session high (121.43) coincides with the 2.618 projection of the Nov 10-17-24 price swing.

- The 10-Year BTP/Bund spread now sits ~5bp off session tights, just below 160bp, with 10-Year BTP yields back above 3.50%.